Today at 13:15 BST, we will see the private report on employment change in the United States. The ADP report has recently given a slightly greater predictive power in relation to NFP, although in August it significantly underestimated the final employment growth. What does the market expect from today's report, and how will this impact interest rate expectations and ultimately translate into financial markets?

Market expectations:

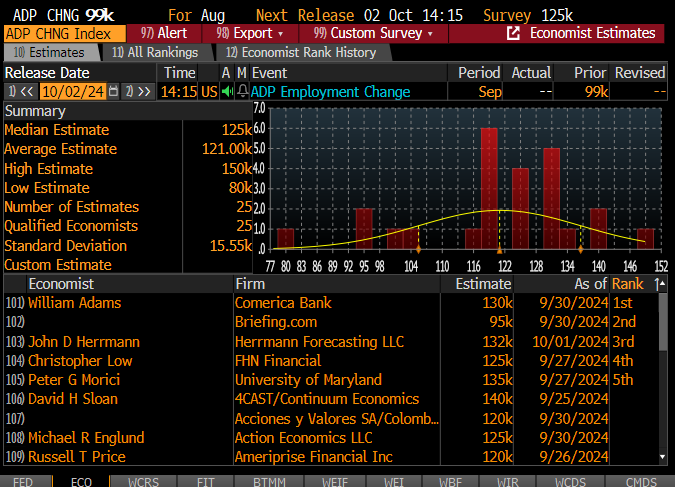

- Bloomberg consensus indicates a reading of 125,000 (median) and 121,000 from the average perspective

- Previously, the reading was 99,000, with the final NFP reading at 142,000

- Bloomberg consensus currently contains only 25 very scattered forecasts: from 80,000 to 150,000

- The best forecasters indicate readings close to 130,000

- Seasonality indicates potential improvement compared to previous readings. Bloomberg Economics points to similar conclusions, which is to be related to the adjustment model regarding the number of births and deaths

- Yesterday's JOLTS report showed a much better state of the labor market, although the trend regarding the number of new jobs still remains downward

- The average number of jobless claims fell to 224,000 in recent weeks, indicating a decidedly better situation than in July and August

- The employment sub-index from the ISM index for industry fell significantly to 43.9 points from 46 points, with an expectation of 47 points

The Bloomberg consensus does not seem to be a good guideline for today's reading. At the same time, it's hard to say whether ADP will be a guideline for the NFP report on Friday. Before NFP, we will still see claims tomorrow and the ISM employment sub-index from the service sector. Source: Bloomberg Finance LP, XTB

The JOLTS report showed a clear improvement, although the trend remains unchanged. Will the ADP report also show a better side?

The Fed is focused on the labor market

The US dollar started strengthening from the beginning of this week, which also affected the weakness of gold on Monday. This happened after Powell's statement, which indicated that the Fed doesn't need to rush with cuts and investors shouldn't expect another big cut. On the other hand, Bostic from the Atlanta Fed indicated that an NFP reading below 100,000 could lead to further action from the Federal Reserve. Currently, the expectation for a double cut of 50 bp in November has fallen to 37%, although it was recently 50%.

How will the market react?

Gold is slightly retreating before the publication of today's data. We see that the earlier correction was contained in the size of previous corrections since the beginning of August. ADP below 100,000 may trigger another increase in expectations for a larger cut and lead to an increase in gold prices around yesterday's peaks at $2,670 per ounce. On the other hand, if ADP turns out to be closer to 130,000, then an attempt to test 2,630 cannot be ruled out. ADP above 150,000 could lead to a break in the last stronger upward trend that began in September. It's worth remembering that gold is currently more volatile due to the tense situation in the Middle East.

Source: xStation5

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

Platinum gains 6% as precious metals rebound, US Dollar weakens

🚨 Brent crude falls below $80!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.