-

Gold continues to climb above $4,200 per ounce, driven by expectations of a shift in Federal Reserve policy.

-

Silver has surged past $52 per ounce, extending its strong upward momentum.

-

The U.S. labor market is showing increasing signs of weakness.

-

Fed officials are signaling the possibility of interest rate cuts in the near future

-

Gold continues to climb above $4,200 per ounce, driven by expectations of a shift in Federal Reserve policy.

-

Silver has surged past $52 per ounce, extending its strong upward momentum.

-

The U.S. labor market is showing increasing signs of weakness.

-

Fed officials are signaling the possibility of interest rate cuts in the near future

Precious metals, including gold, are rising sharply today, extending the ongoing rally. Gold is climbing above $4,200, rebounding relatively quickly after a brief correction that tested the $4,100 level. Currently, the key support levels are $4,100 and $4,160 per ounce, as defined by price action. In October, the Fed is expected to cut rates by another 25 basis points. Metal availability in the London market remains tight, while spot demand is very strong.

Investors are increasingly viewing precious metals as a hedge against currency devaluation and the consequences of growing budget deficits — a phenomenon referred to as the “debasement trade.”

- In the case of silver as well, the market has been gripped by a liquidity squeeze in London, which has driven up benchmark prices that now exceed New York futures. The gap between the two markets is about $1 per ounce, while the annualized cost of borrowing silver (on a monthly basis) stood at approximately 17% on Tuesday — both historically elevated levels.

- Traders are also awaiting the results of the U.S. administration’s so-called Section 232 investigation into critical minerals, which includes silver, platinum, and palladium. This inquiry has raised concerns that these metals could be subjected to new tariffs, even though they were officially exempted in April.

The four major precious metals have posted impressive gains this year — ranging from 60% to 82% — becoming the leaders of the commodity market rally. The key drivers behind gold’s price surge include central bank purchases, rising investor exposure to ETFs, and interest rate cuts by the Federal Reserve.

Spot demand for so-called “safe haven” assets has been further fuelled by:

-

escalating trade tensions between the U.S. and China,

-

concerns over the Federal Reserve’s independence,

-

and the risk of another U.S. government shutdown.

A major driving force behind the rally remains aggressive gold buying by central banks, which are acquiring large volumes of the metal amid a weakening U.S. dollar and falling bond yields. Concerns about rising debt, lower interest rates from the Fed and ECB, and geopolitical risks are prompting investors to treat gold as a reliable store of value. The Fed is set to decide on interest rates on October 29 and is likely to cut them by 25 basis points — as also hinted by recent comments from Federal Reserve official Susan Collins.

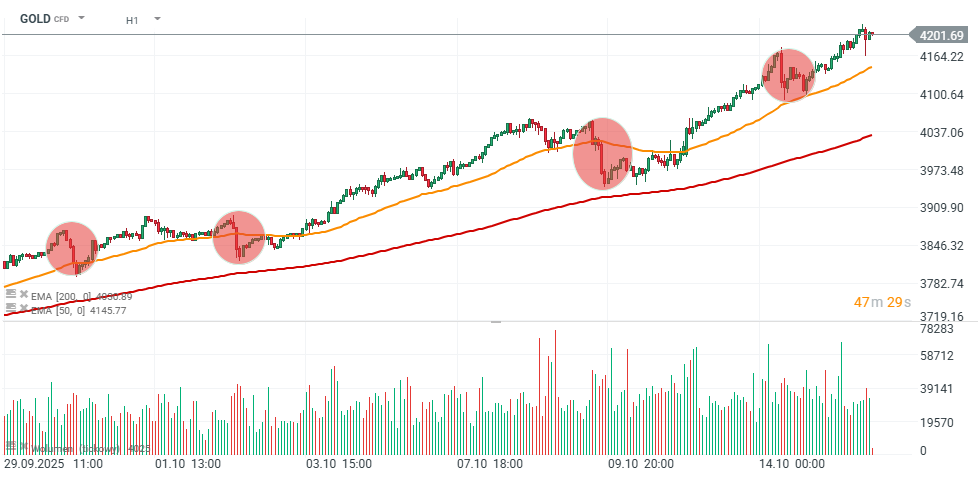

GOLD (H1 Timeframe)

Gold has experienced a few minor corrections, but the uptrend that began in early October remains dominant.

Source: xStation5

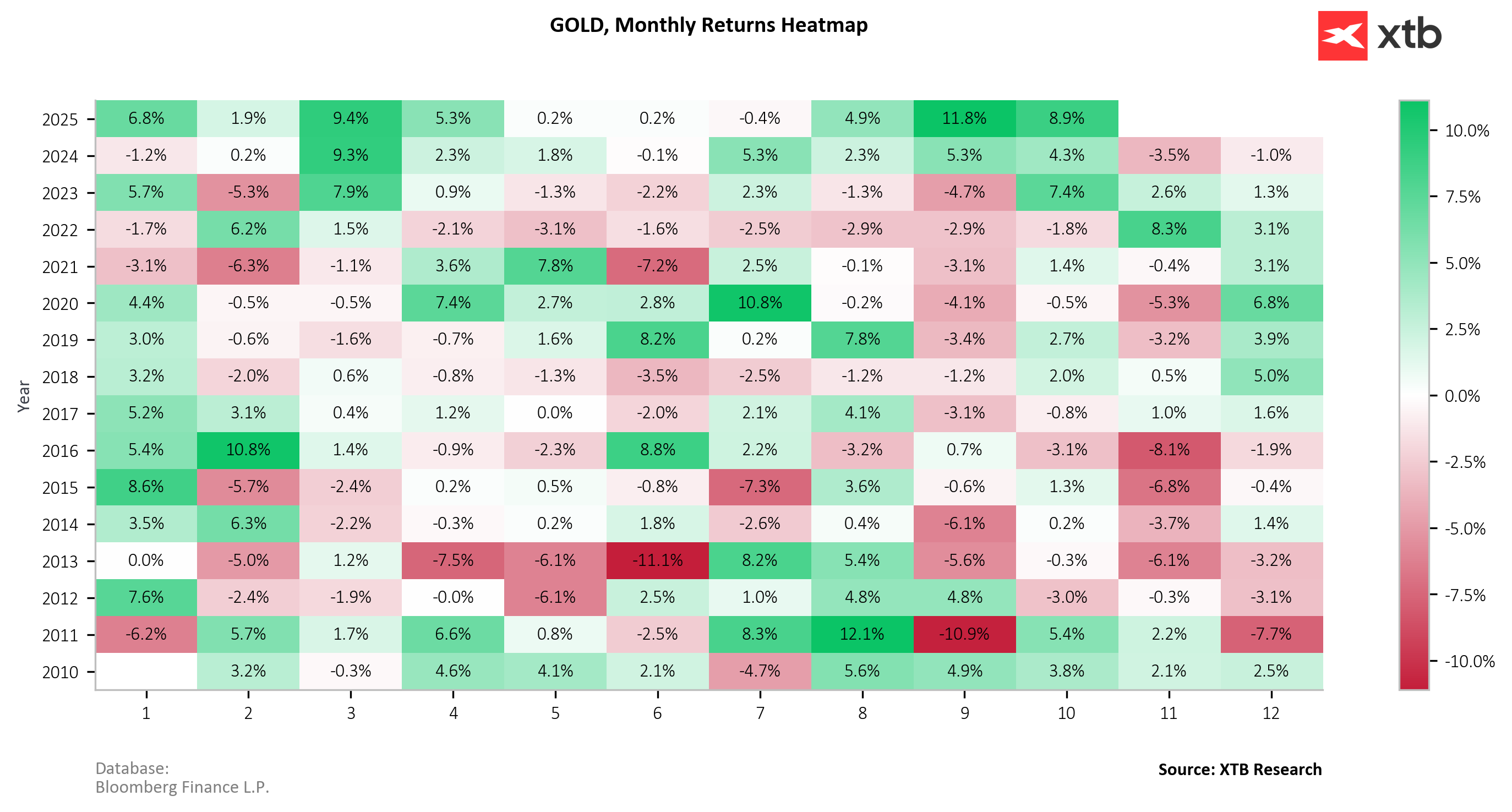

Gold's Performance Over Time

Historically, October hasn’t been particularly favorable for gold prices. However, in 2022, the metal’s price rose by over 8%. So far, since October 1, gold has gained around 9%, climbing from $3,850 to its current level per ounce.

Source: XTB Research, Bloomberg Finance

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.