New York Fed chief John C. Williams and Lisa D.Cook of the Federal Reserve Board commented today on the US monetary policy situation:

Fed Williams

- Fed policy is not very restrictive at the moment although overall I see that financial conditions have tightened;

- The Federal Reserve may need to maintain a restrictive monetary policy even for several years;

- If financial conditions loosen too much, as expected by the Fed's outlook, the Fed will have to raise interest rates;

- There are many indications that the U.S. economy is becoming more resilient but we may slow down rate hikes now as we are closer to the peak. If the situation changes, however, we may move faster than 25 bps;

- 25 bps rate hikes seem to be the best option for now. Currently, however, a target rate of 5%-5.25% is a reasonable target;

- Maybe service prices will remain high, and if that happens, we will need higher rates. Demand for services as well as labor is still very high, demand in the economy is stronger than usual;

- There is a lot of uncertainty around the outlook for inflation, it may prove to be more persistent for some reasons;

- So far, commodity prices are falling but there is a long way to go before a further decline. However, inflation driven by the rental market is weakening, and the housing sector is clearly slowing down;

- The labor market is extremely tight, and it is unclear whether and by how much unemployment will rise. With a strong economy, job growth may continue to rise.

Fed Cook

- The data paint a clear picture of a strong labor market with persistently high inflation. The cycle of increases is not over yet;

- Inflation is still too high despite the decline, the Fed will maintain a restrictive monetary policy for a long time;

- It is possible that the upward path of the unemployment rate will be lower than the latest Fed forecasts. I believe that inflation can be contained without a large increase in unemployment;

- The combination of a strong labor market and falling wages and prices has raised hopes of a soft landing. I expect inflation to continue to decline this year and next, although progress may be uneven

- Lower rate hikes are more appropriate now, as the Fed assesses the cumulative impact of past hikes;

- The Fed has seen improvement but needs to pay attention to a lot of data. In 2023, U.S. GDP growth seems most likely today though I expect it to be below average.

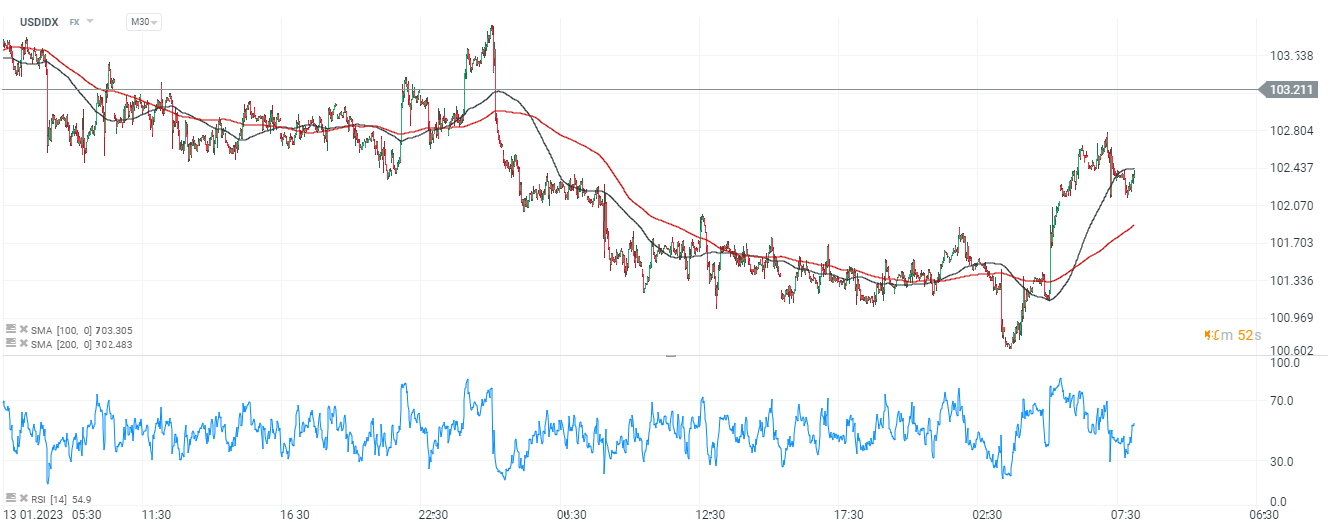

The USDDIDX Dollar Index reacted with an initial rise to Williams' comments, but supply came to a head near the SMA100 average (black color) and is attempting to pull back the 'greenback'. Source: xStation5

The USDDIDX Dollar Index reacted with an initial rise to Williams' comments, but supply came to a head near the SMA100 average (black color) and is attempting to pull back the 'greenback'. Source: xStation5

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

US ADP employment below estimates! EURUSD extends gains 📈

Economic calendar: US macro data and big tech earnings🔎

Market wrap (05.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.