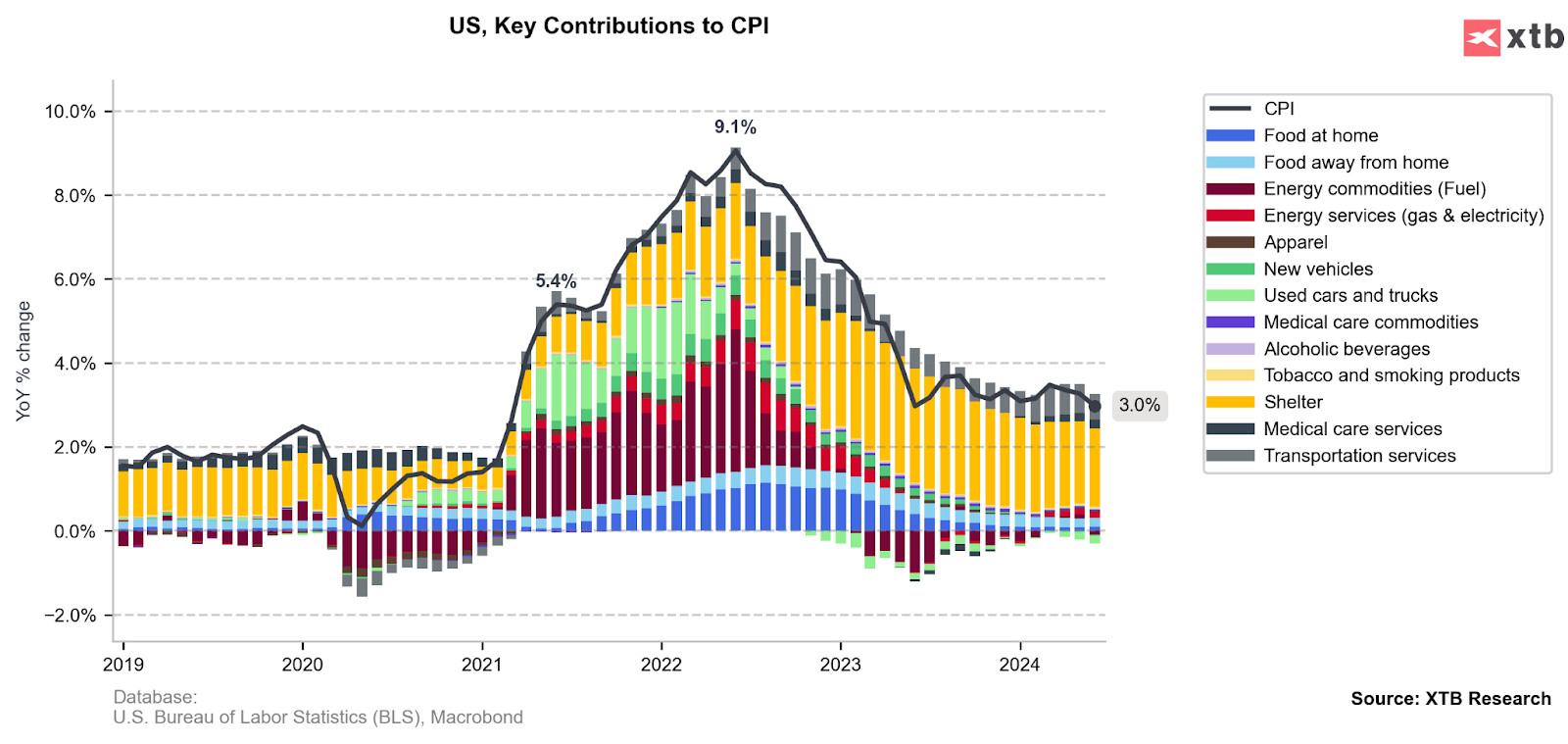

US CPI inflation data for June was released yesterday at 1:30 pm BST. The report positively surprised as inflation came in below expectations. The data showed a decrease in the rate of consumer prices to 3.0% year-on-year (expectations were for 3.1% year-on-year), while core measure (excluding energy and food prices) declined to 3.3% year-on-year (expectations were for 3.4% year-on-year). Following the publication, we observed strong gains in US indices, as well as a sharp drop in the US dollar and bond yields. However, major indices, namely US500 and US100, quickly erased those gains later on and ended the day down 0.88% and 2.20%, respectively. Interestingly, gains in the small-cap US2000 index (Russell 2000) have been maintained, which might be influenced by the hope for some relief among smaller businesses with the upcoming interest rate cuts. However, is a rate cut at the September FOMC meeting a done deal? Take a look at our analysis based on the latest data.

Headline and Core Inflation

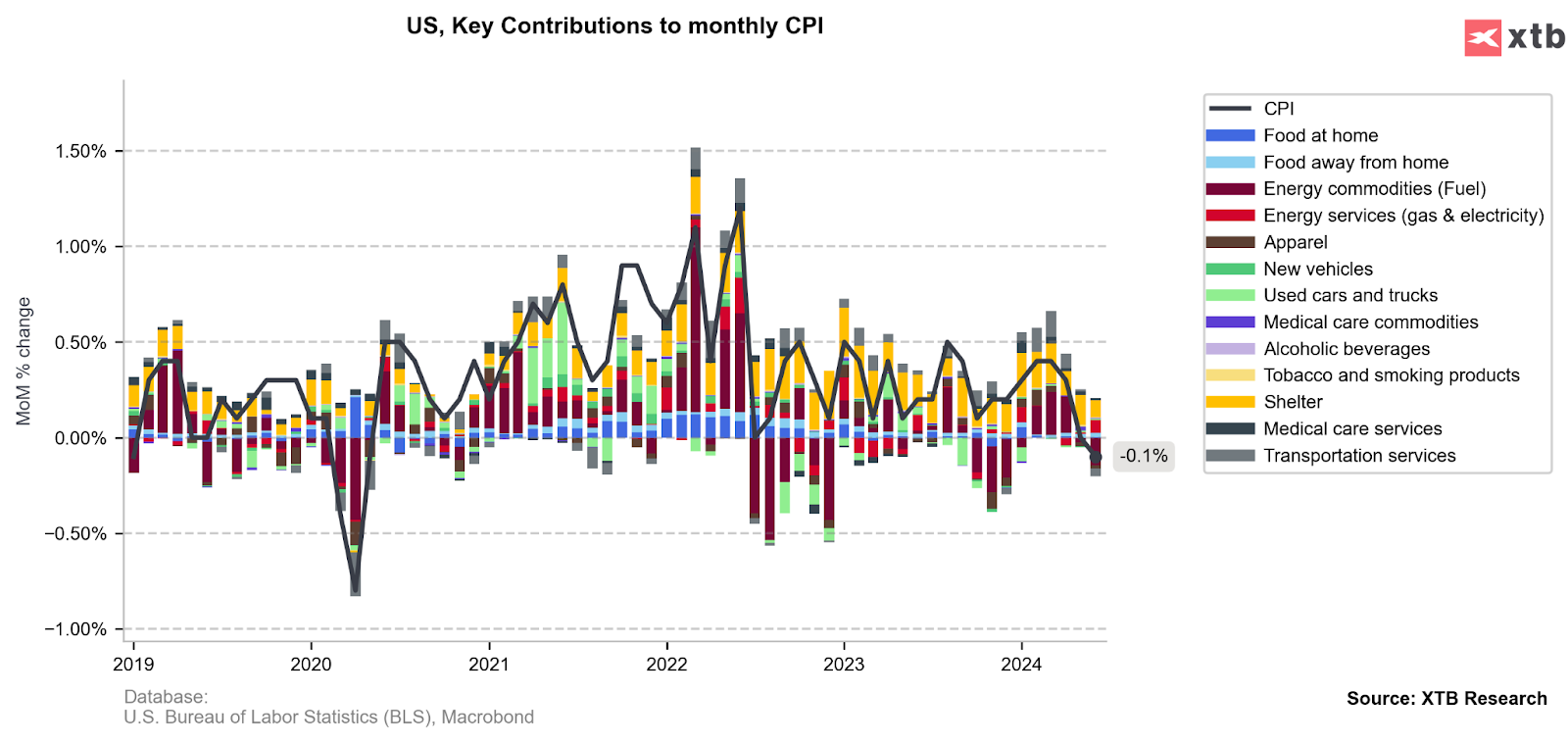

Annual inflation measures indeed came in lower than expected, but the rate of price increases in the stubborn service sector remains high. The lower-than-expected reading was largely possible due to deflationary or neutral readings from other sectors of the economy. Contributing to disinflation were categories such as new and used cars, low food prices, and energy prices. Meanwhile, rental prices still have the largest share in inflation, which is slowly but steadily moving towards stabilization.

Can Low Inflation Persist?

The potential for further deceleration in price growth in some sectors may be limited, especially in those that have so far contributed disinflationary to the main reading.

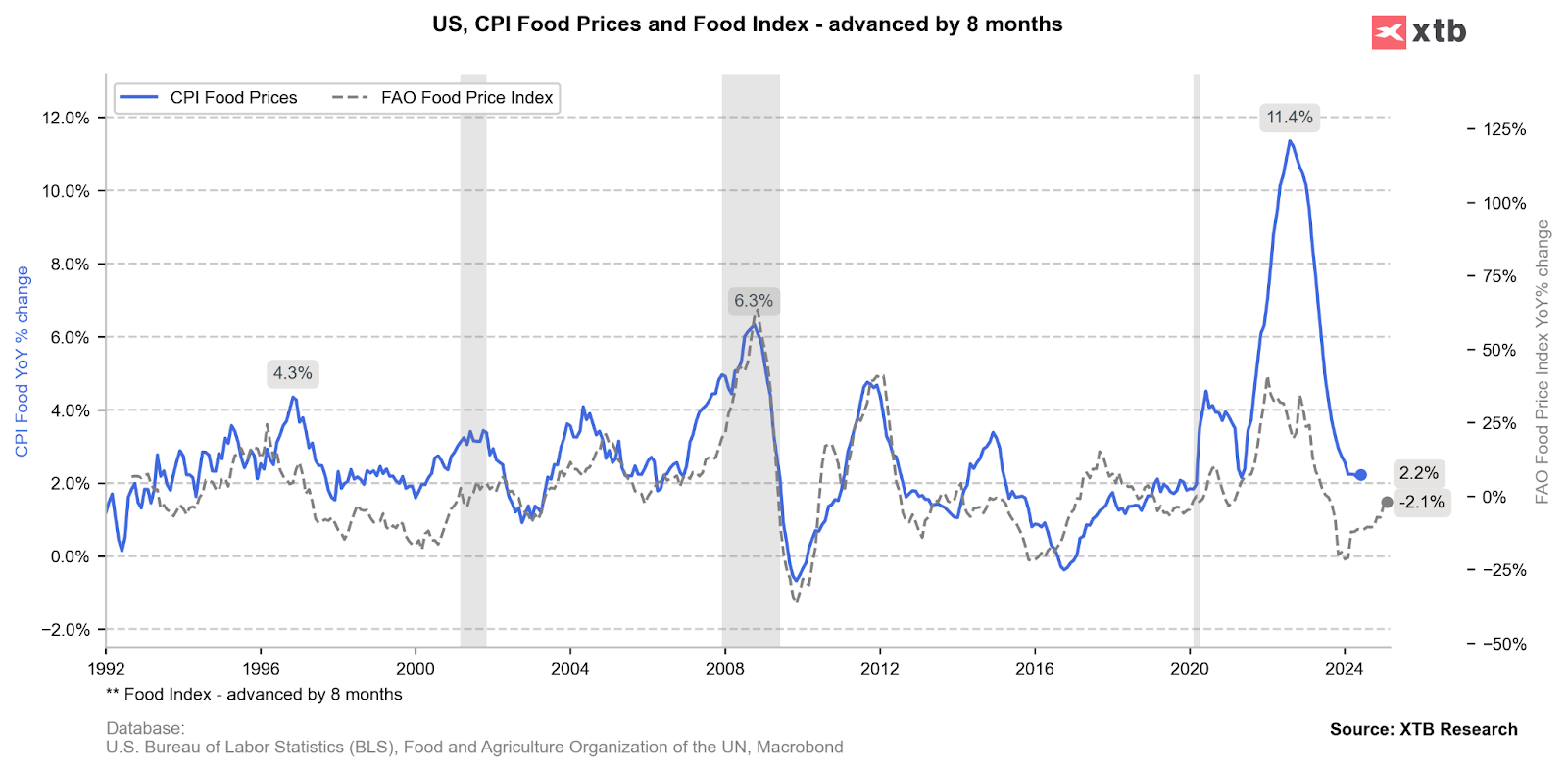

Food inflation remains low, and their positive impact in the coming months may be limited for this reason.

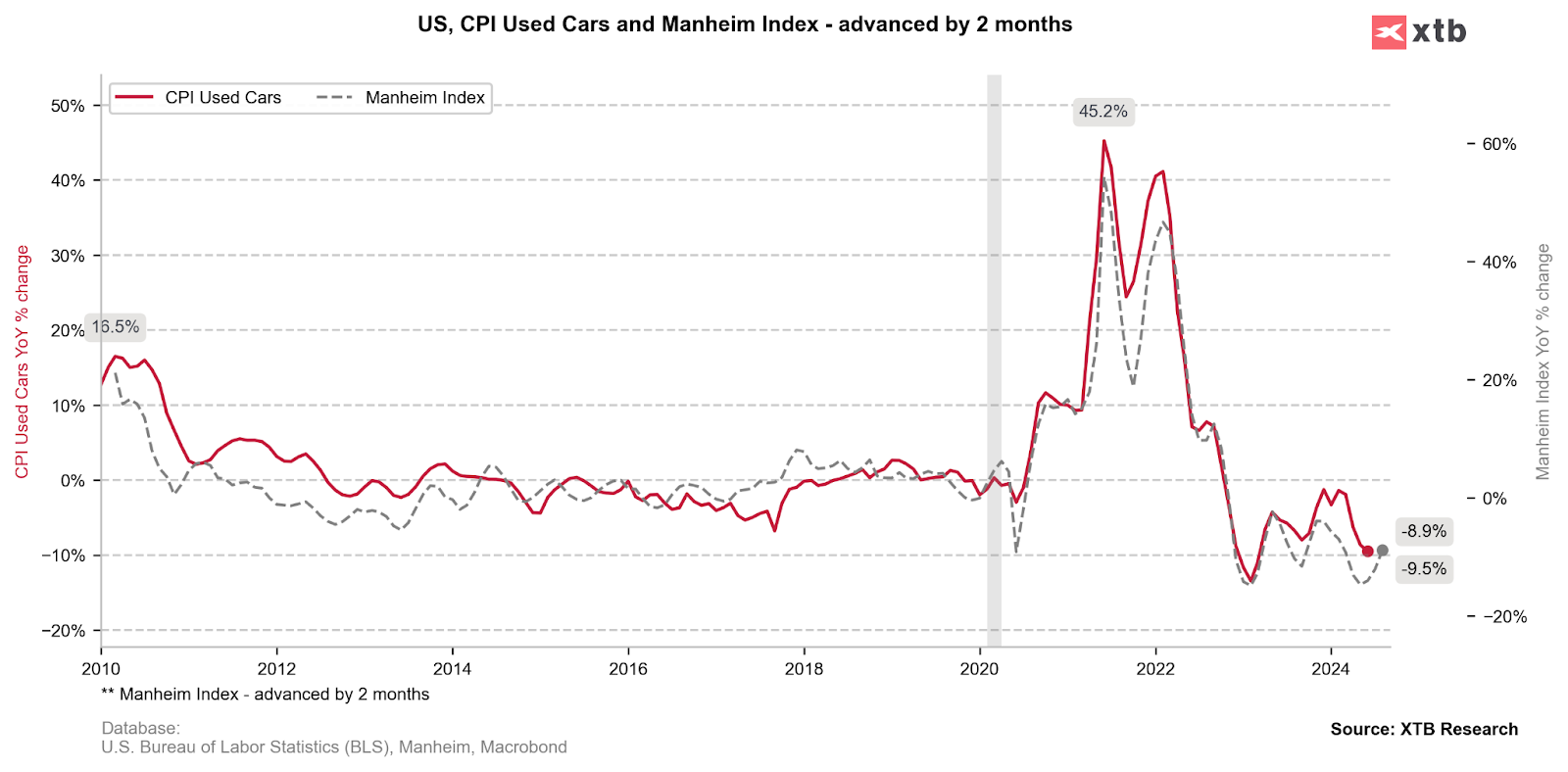

Similarly, the situation looks in the sector of used and new cars. Declines in recent months mean little chance of a further downward trend with such a low base.

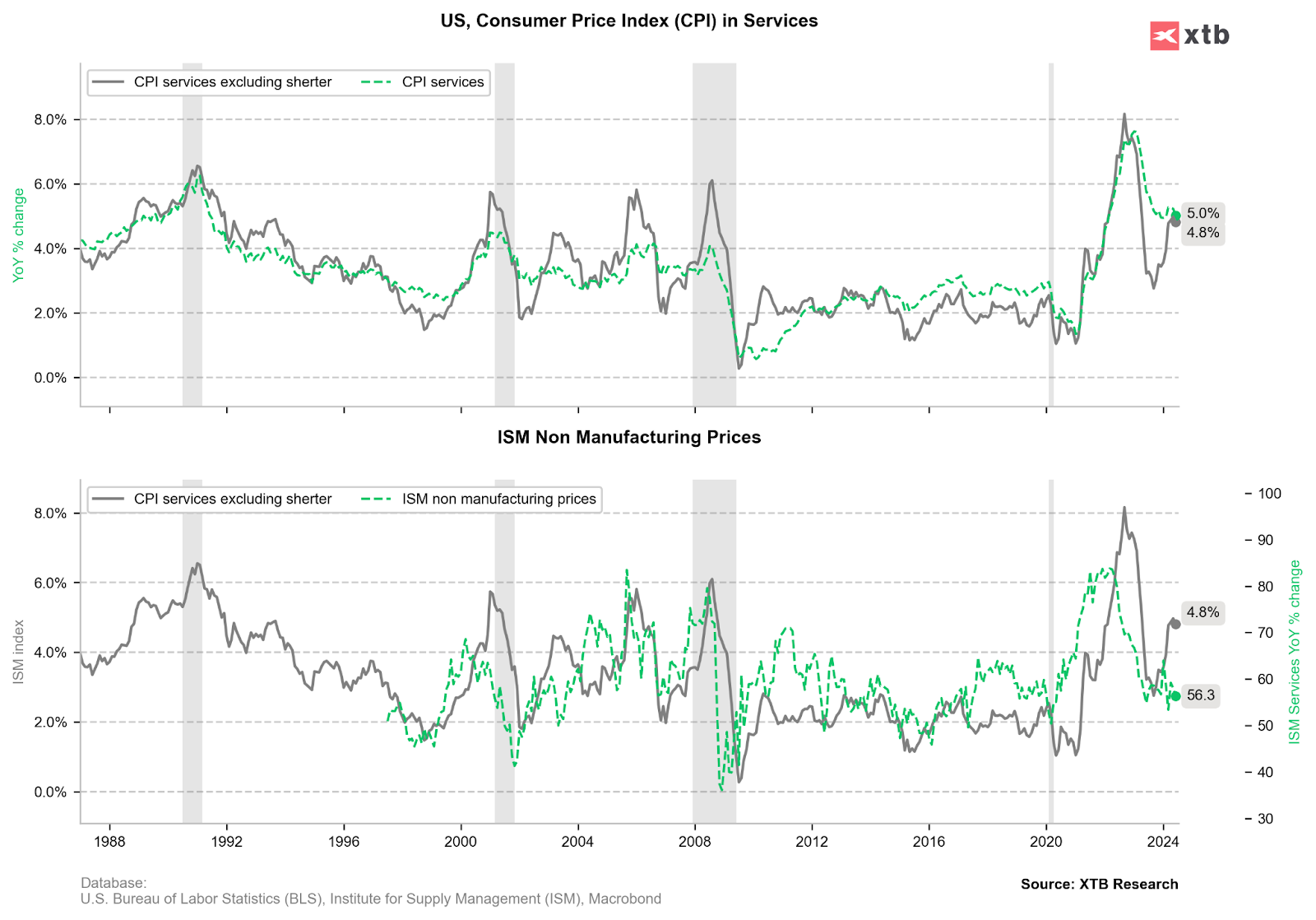

Therefore, all hope remains in the service sector inflation, which so far remains high. Here, the fact is that monthly figures look better than annual ones. However, the close correlation between rental prices and property prices (Case Shiller Price Index) indicates that the downward trend may last a few more months before a potential rebound early next year.

Monthly Data Fuels Optimism

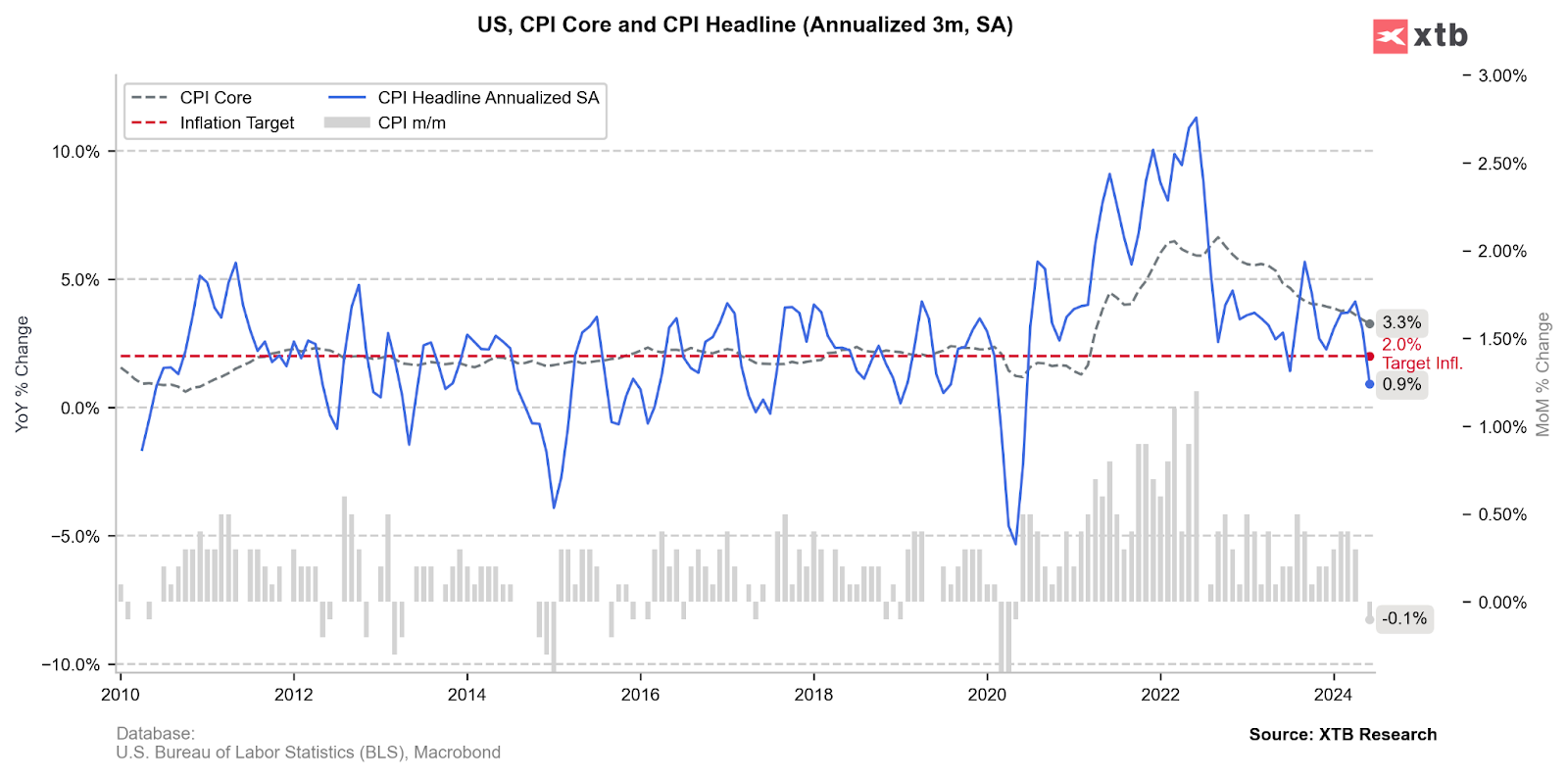

It is the monthly data that is a strong argument for the Fed to make the first interest rate cut at the September meeting. The 0.1% month-on-month decline in inflation in June after flat growth in May (0.0% month-on-month) is currently fuelling market speculation.

This is because annualized inflation for the last three months has fallen to 0.9%, the lowest reading in 4 years and well below the Fed's target.

Will the Fed Start Cutting Rates in September?

Ultimately, everything still depends on the inflation data for July and August. The most important thing for the Fed is to maintain a sustainable disinflationary trend. The data from the last two months have been very good in this context, and if they hold, we will most likely see the first cut of 25 basis points in September. The next 3-4 months are a good time to ease monetary policy. Currently, the markets fully price in the first rate cut at the September meeting, whereas before the report, the chances were 78%. Investors now price a total of 2.43 cuts for the whole of 2024, compared to 2.02 before the report. This means that for now, cuts in September and December this year look likely, with a possibility of another cut in-between (November).

NFP much below expectations! 🚨EURUSD spikes 📈

Dollar and Nasdaq facing a key test

Chart of the Day: What will drive the US stock market? (07.08.2026)

Economic Calendar: Will NFP Move the Market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.