Tesla continues to ignite strong opinions – some view it as a leader in the technology and AI revolution, while others see it as an "ordinary" car manufacturer with an overvalued assessment. Today's Q2 2025 report has the potential to determine which category the company truly belongs to. Following record deliveries in Q4 2024 and a painful disappointment in Q1 2025, investors are closely monitoring whether Tesla can regain growth momentum or if it is ceding ground to Chinese rivals, potentially losing its place in the elite "Magnificent Seven" group of leading US technology companies.

Q2 2025 Performance Expectations

-

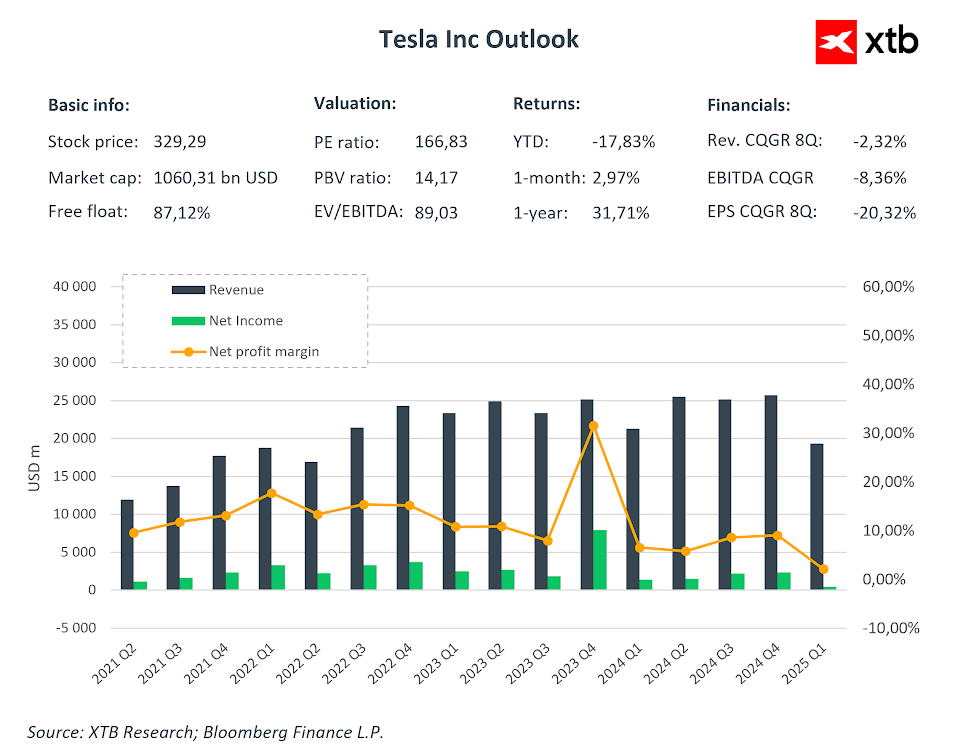

Revenue and Profitability: Market expectations forecast revenue around $22.6 billion, representing an approximate 11% year-on-year (y/y) decline but a slight rebound from the previous quarter. The consolidated gross margin is anticipated to be around 16.5%, with operating profits at $1.2 billion – levels similar to the lows of Q1 2025.

-

Earnings Per Share (EPS): Bloomberg consensus points to an adjusted EPS of $0.42, approximately 18% below the figure from a year ago.

-

Free Cash Flow (FCF) and CAPEX: The market expects FCF of around $760 million, alongside capital expenditure exceeding $2.4 billion for the quarter.

-

Deliveries and Production: Following the previously announced 13% y/y drop in deliveries (384,000 units), analysts will be watching to see if the company maintains its target of 1.65 million vehicles for 2025.

The record sales in Q4 2024 were followed by a sense of disillusionment after the Q1 2025 results. While an improvement in results is now expected compared to the previous quarter, it might not be enough to fully convince investors. Source: Bloomberg Finance LP, XTB

EPS expectations for Q2 have been consistently reduced for some time. Given such changes, often, upward price movements are not justified by fundamentals but merely by hope for future changes. Source: Bloomberg Finance LP, XTB

What Questions Are Weighing on Investors?

Investors are primarily focused on questions regarding future projects, which continue to position Tesla as a technology company rather than solely an automotive one. Frequently repeated inquiries concern the pace of robotaxi expansion beyond Austin, the timeline for the "cheaper" car model, the release date of the fully autonomous FSD version, the commercialization of the humanoid robot Optimus, and specific regulatory hurdles for driverless operation. Pressure is mounting on company founder Elon Musk, upon his return from working with the current government administration, to present tangible milestones the company will achieve in the near future, rather than simply making further promises while the company's results deteriorate. Although the valuation of a technology company often relies on prospects, the company is increasingly disappointing investors in terms of product delivery.

Echoes of Disappointment After Q1 2025

The first quarter saw a 9% y/y decline in revenue, and the operating margin dropped to just 2.1%. Deliveries shrunk by almost 14%, a stark contrast to the record-breaking end of 2024, and made investors realize that the impact of price cuts has its limits. Furthermore, Tesla provided no specific forecasts for 2025 at that time, increasing market uncertainty.

Robotaxi and Autonomy – Promise or Real Growth Driver?

A pilot fleet of robotaxis has been operating in Austin since June, but each ride still requires a safety operator. Musk announced that the service would expand to California and Arizona within "a month or two," with hundreds of thousands of autonomous vehicles expected on roads by the end of 2026. Meanwhile, Waymo is already providing fully autonomous rides in Los Angeles, Phoenix, San Francisco, and several other cities, indicating that Tesla is no longer the sole pioneer in this technology. This differing approach from competitors may suggest that Tesla may not necessarily become the leader in this market in the coming years, casting doubt on its very high valuations.

Competitive Pressure and Regulatory Risks

In China, Tesla's share of the NEV segment has fallen to just under 5%, while BYD controls almost a third of the market. In the US, General Motors sold one EV for every three Teslas in Q2, capturing 15% of the EV market, whereas just four years ago, Tesla held 80%. Additionally, federal tax credits for EV purchases – a past demand driver worth approximately $7,500 per vehicle – are set to expire in September. Simultaneously, the program penalizing internal combustion engine vehicle manufacturers is ending, which will reduce Tesla's revenue from trading emissions credits.

Can Elon Musk's Return Restore the Company's Luster?

Musk is once again more deeply involved in the company's day-to-day operations, but his increasing political activity and numerous side projects (xAI, SpaceX, X platform) are diverting attention. It is becoming increasingly clear that Tesla's stock price reacts strongly not to fundamentals but to the CEO's latest promises regarding robotaxis or humanoid robots. According to DataTrek, as much as 95% of the company's market value today stems from faith in future innovations, not from current cash flows.

Valuation Versus Operational Reality

Tesla is currently trading at an EV/EBITDA multiple of approximately 80-90x, about ten times higher than the industry average. The price-to-earnings ratio has recently translated into an astronomical 160-180x, while Toyota or BYD trade at values dozens of times lower, while offering higher volume momentum or more stable margins. With such stretched metrics, even a cosmetic deterioration in results could trigger a sharp valuation compression.

Will Tesla Remain in the "Magnificent Seven" Club?

Since the beginning of 2025, it is the only company from this elite group that has contributed negatively to the index's total return, and its market capitalization has fallen below 8% of the "Mag7" total value. If today's results disappoint again, and Musk fails to present a credible plan for commercializing AI projects, Tesla may yield its place to a company with more predictable fundamentals. On the other hand, the Mag7 group might simply become a Mag6 group, considering the lack of support for Musk from the current administration.

What Does the Market Think of the Company?

Recently, key analysts have repeatedly reduced price targets for the company. For example, Goldman Sachs indicated that the target price is now $285, down from the previous $390.

The 12-month target for the company, based on all recommendations, is slightly below $300 per share. However, based on comparative valuation, looking at other car manufacturers, the target price for the company could be set as much as three times lower than the current price. Source: Bloomberg Finance LP

Summary

In a few hours, we will see whether Tesla can prove it remains a leader in the technological revolution, or if it is indeed becoming an "ordinary" electric car manufacturer with an expensive valuation. Without a breakthrough in profitability and the scaling of robotaxis, Q2 may only deepen the divergence between the company's narrative and its financial reality. Of course, it is important to remember that Elon Musk remains one of the greatest visionaries of the 21st century, so the company cannot be definitively written off. Nevertheless, the fundamentals and realities are looking increasingly grim, and therefore, only a strong stance from the CEO or a clear upside surprise in the data will be able to alter the company's fortunes.

The share price is near an important resistance level associated with a downtrend line. It is worth noting that after a rebound in April, the uptrend ended in late May. We are currently observing new lower highs, although there are no new lower lows either. We are dealing with two triangle formations – a small one and a large one. Theoretically, a breakout from the small formation downwards could pull the company to test the lower boundary of the large formation, around $200 per share. On the other hand, an upward breakout could lead to the start of a new uptrend, but this would require a strong declaration from Musk regarding the future. Currently, the key resistance is around $360. Source: xStation5

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.