Oil prices remain under strong pressure after the partial normalization of the situation around the Strait of Hormuz and the resumption of peace talks between the United States and Iran. Brent has already fallen to USD 74 per barrel, while WTI is near USD 71.

At this stage, the market appears to be pricing out any geopolitical or war-related “premium” in oil and inflation. However, the optimism may be premature.

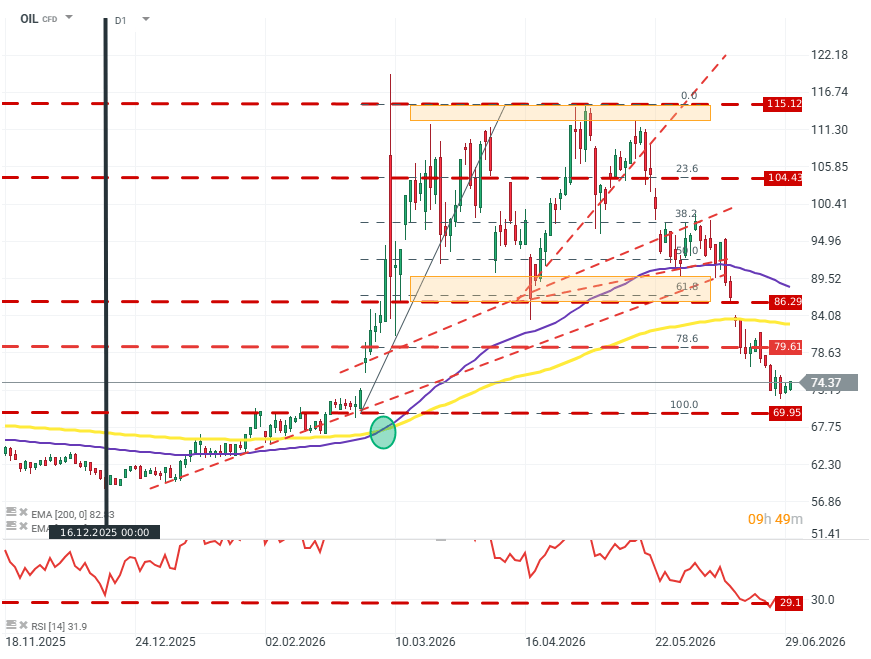

OIL (D1)

On the oil price chart, what stands out is an extremely low RSI level, which does not reflect tensions in the supply chain. Source: xStation5

UNCTAD, an official UN body, warns that even after the Strait of Hormuz is reopened (which has not happened yet), food and fuel costs could remain elevated for a prolonged period.

The problem is no longer solely the oil price itself, but the delayed effect of earlier disruptions in transport, freight costs, insurance, or fertilizer prices. This is particularly important for countries that import energy and food, where higher transport and agricultural production costs translate into consumer prices more quickly. According to UNCTAD, 61 economies remain exposed to further shocks related to imports of oil and grain.

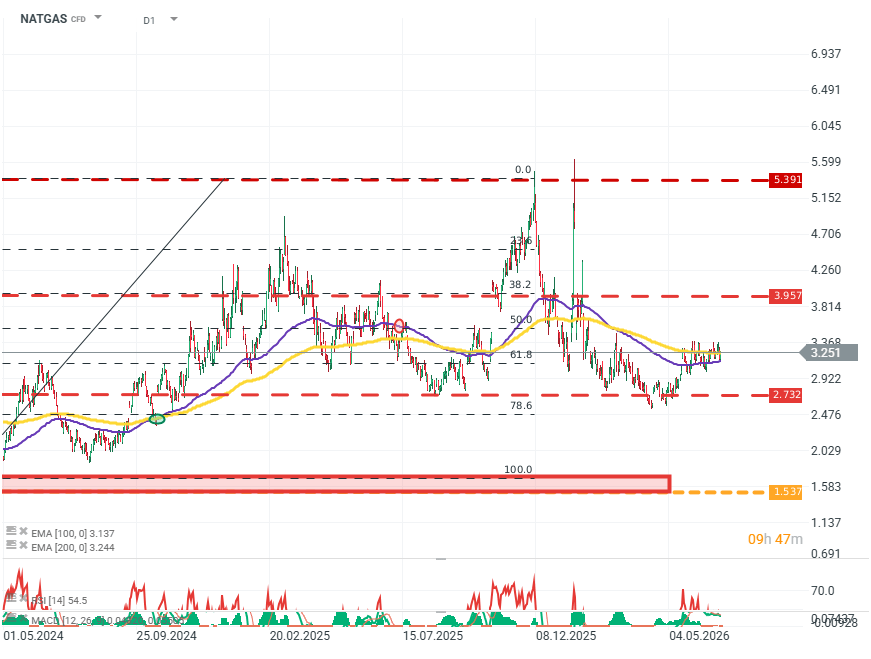

NATGAS (D1)

Source: xStation5

Gas remains the second channel of inflationary pressure. U.S. natural gas prices rose more strongly today than oil, and the persistent risk around LNG flows from the Persian Gulf region may limit the pace of energy-cost normalization in Europe and Asia. More expensive gas means not only higher energy bills but also pressure on fertilizer prices and, later, on food production costs. This makes the inflation impulse potentially more persistent than the drop in oil prices alone would suggest.

Partial market calm is supported by diplomatic signals. U.S. representatives were reportedly set to meet in Doha with Qatari mediators, and Pakistan had earlier pointed to the possibility of resuming talks between the United States and Iran. At the same time, Qatar emphasized that this was not a high-level meeting between Washington and Tehran.

Wild card: Russia

Many analysts pointed to far-reaching benefits for the Russian Federation from the surge in oil prices, but the campaign of “kinetic sanctions” and increasingly intensive air attacks on Russian territory raise doubts not so much about the scale of Russia’s benefits from the crisis, but about the presence of Russian products on the market.

Kremlin representatives have confirmed that they are currently seeking potential fuel suppliers who could alleviate the ongoing and worsening domestic fuel crisis. The Kremlin refused, however, to indicate which entities might undertake such deliveries. Importantly for the oil market, the shift of Russia from an exporter to an importer of fuel (not crude oil) will put additional pressure on already insufficient refining infrastructure, which means that even if oil prices fall, fuel prices may remain elevated.

What about the dollar?

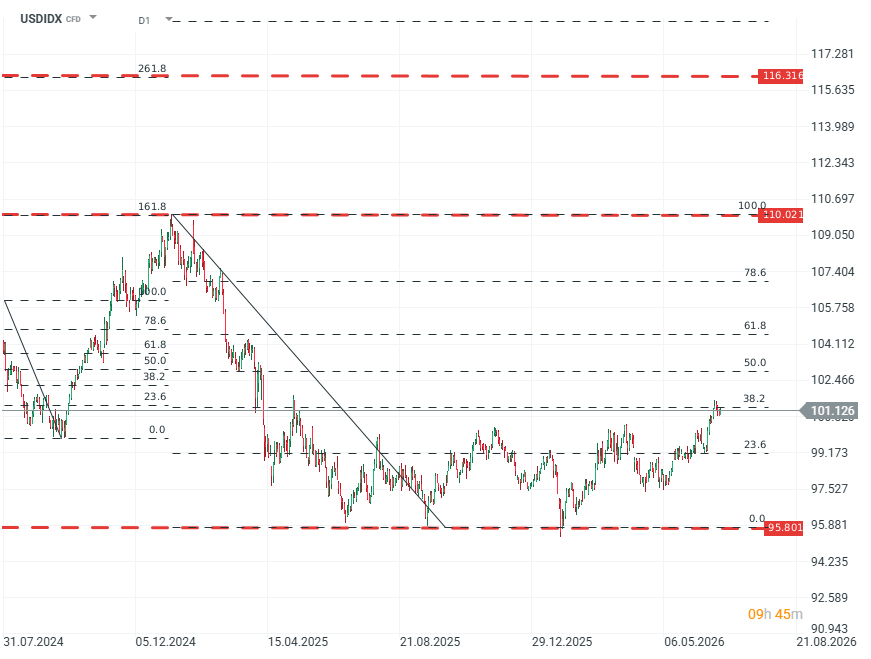

USDIDX (D1)

The Dollar Index remains near its lows from recent years. If the Fed turns out to be more hawkish in its rhetoric (or decisions) than expected, there is significant room for an upward correction. Source: xStation5

The dollar index is holding above 101 points, which, with commodities priced in USD, can increase cost pressure in economies that import energy and food. Even if the nominal oil price falls, a stronger dollar partly limits the positive effect for importers outside the United States. This is especially important for emerging markets such as Poland.

In the short term, the energy market is pricing in a de-escalation scenario, but the risk balance remains asymmetric. Looking at indices and commodity futures prices, investors see the end of the war not as a prospect but as a fait accompli.

The current relationship between the United States and Iran resembles a ceasefire, not peace. A ceasefire that one side breaks at least once a week. In addition, the agreement includes a number of provisions that may be very difficult to implement due to required approvals, for example from the U.S. Congress. The agreement itself is constrained by many conditions that neither side wants to meet, and both sides have until August to reach a real compromise, or to confirm the lack of one.

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.