The EURUSD has ticked down slightly over the last few minutes, likely reacting to Waller's somewhat hawkish remarks. It is also worth noting the weaker-than-expected University of Michigan consumer sentiment reading, which dropped to 44.8 against expectations of 48.2. Meanwhile, inflation expectations are climbing, with the 1-year outlook rising to 4.8% and the 5-year hitting 3.9%.

Key Takeaways from Christopher Waller's Speech

-

End of the Rate Cut Narrative: "It's crazy, given recent data, to be talking about rate cuts in the near future." The current plan is to hold rates steady.

-

A Neutral-to-Hawkish Shift: Waller believes the Fed should remove the "easing bias" from its statements. He admitted that recent inflation and labor market data have completely changed his outlook.

-

Rate Hikes as a Last Resort: While he isn't calling for an immediate hike, he "would not hesitate" to back one if inflation expectations (particularly over a 2-to-4-year horizon) begin to unanchor.

-

The Labor Market Takes a Back Seat: The labor market is stable and unemployment is low. It is no longer the primary driver of the policy path—inflation is now calling the shots.

-

Key Risk Factors: Price pressures are broadening again, and inflation is becoming sticky. The situation is further complicated by high energy costs (tied to the duration of the conflict in Iran) and an unyielding AI investment boom.

-

Balance Sheet Reduction (QT): Waller floated the possibility of trimming the Fed's balance sheet by an additional $300 billion to $500 billion.

-

The New Reality of Reserves: He made it clear that there is no returning to the small balance sheet of 2008. The Fed intends to operate under an "ample reserves" system and will not allow a scarce-reserve environment to develop.

Waller’s Metamorphosis

Waller has undergone a sharp shift in a very short period. Lest we forget, back in January 2026, he voted for a 25-basis-point rate cut. Today, he calls such ideas "crazy." While his tone is hawkish, it is evident he does not want to choke the economy with rate hikes right now—unless forced to by a sudden unanchoring of inflation expectations (which have already crept up to an uncomfortable 4.8% in the 1-year UoM outlook).

Instead, Waller would prefer the heavy lifting to be done by rising market bond yields (which naturally cool the economy) and further quantitative tightening (QT). However, it's worth noting that rising yields are a headache for the US government, which faces ever-growing borrowing needs.

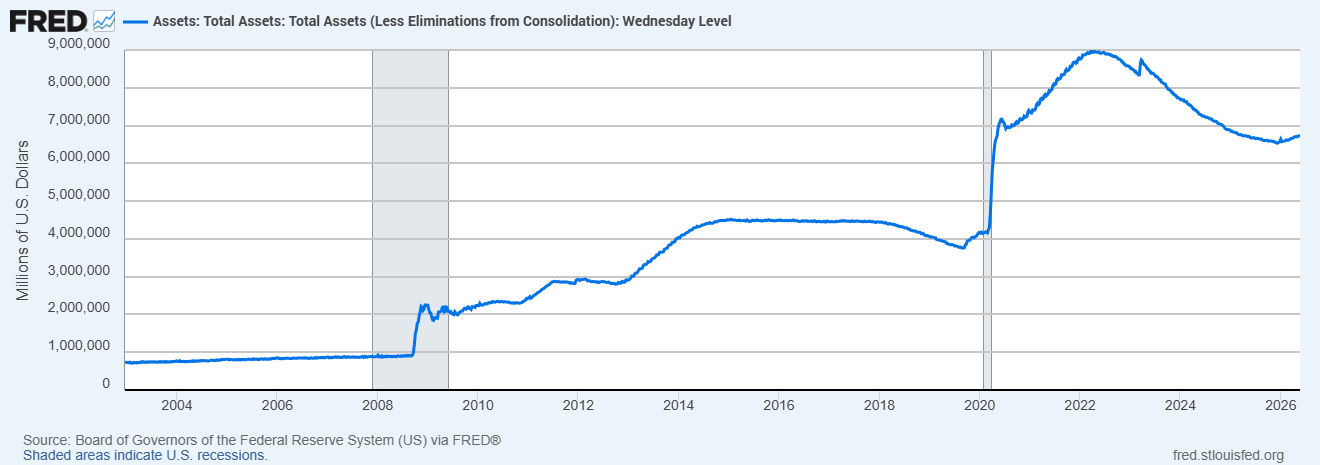

A Drop in the Ocean: The Math Behind the Fed's Balance Sheet

Trimming another $300 billion to $500 billion sounds impressive in headlines, but in the grand macroeconomic scheme, it’s mere cosmetics.

Following the pandemic-era money-printing frenzy, the Fed’s balance sheet ballooned to around $9 trillion. Even after the quantitative tightening seen so far, removing another $500 billion won't even bring the balance sheet below the psychological $6 trillion mark. This highlights the tight corner the central bank has painted itself into.

Surrendering to the "Mega-Balance Sheet"

-

Pre-2008: The Fed's balance sheet was under $1 trillion (roughly $800–$900 billion).

-

Phase I of the Crisis (QE1): A massive spike above $2 trillion.

-

2012 (QE3): Around $3 trillion.

-

2014: Peaking at approximately $4.5 trillion.

-

2018–2019: An attempt at quantitative tightening (QT) that ended in panic and emergency intervention in the repo market in September 2019, as reserves became too scarce.

-

Post-2020: Ballooning to $9 trillion.

Historically, Waller belonged to the camp of academic conservatives who warned against a bloated balance sheet, arguing that it distorts financial markets and hooks governments on cheap debt.

His comments today "There is no way we can go back to the small balance sheet of 2008" and his emphasis on an “ample reserves system” amount to an official surrender to this new economic reality. Waller knows all too well that the modern banking system is so saturated with liquidity that any attempt to drain it deeper (below the informationally critical $6 trillion mark) would risk paralyzing the interbank market, echoing the 2019 repo crisis.

The Warsh Connection

At the same time, Waller’s remarks today may reflect how Kevin Warsh views monetary policy. Warsh is scheduled to be sworn in today as Federal Reserve Chair by Donald Trump. Warsh famously opposed an oversized balance sheet even during the global financial crisis. Furthermore, both Waller and Warsh appear to belong to the inner circle of central bankers trusted by Trump, signaling a potential alignment in how the Fed will handle the balance sheet moving forward.

Oil rises over 3% 🛢️

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.