The start of Thursday’s session on Wall Street is bringing a slight upward correction, likely a relief rebound after the deep declines of the last few sessions.

The early-session leader is the Russell index, whose futures are up nearly 1%. Beyond the rebound effect, it’s possible the market is seeing pressure on the Fed coming from the labor market as well as low core PPI - so that it does not tighten policy.

- One of the key news items that may define the direction of today’s and tomorrow’s sessions are Donald Trump’s comments regarding Iran. After several weeks of de-escalatory rhetoric, the president is clearly pointing to a high likelihood of a return to bombing Iran.

- Reports from the WSJ indicate that OpenAI may enter a phase of aggressive price war with Anthropic ahead of its IPO.

Macroeconomic data

- In the U.S., key macroeconomic data were published regarding inflation and producer prices.

- Labor market data surprised the market with a moderate deterioration: jobless claims rose from 225k to 229k, versus expectations of a decline to 220k.

- PPI inflation came in mixed. Headline PPI rose above expectations to 6.5%, while core PPI fell below expectations to 4.9%. This suggests that broader economic conditions may be weaker than the market is pricing in, and that the rise in prices has a larger-than-expected energy component.

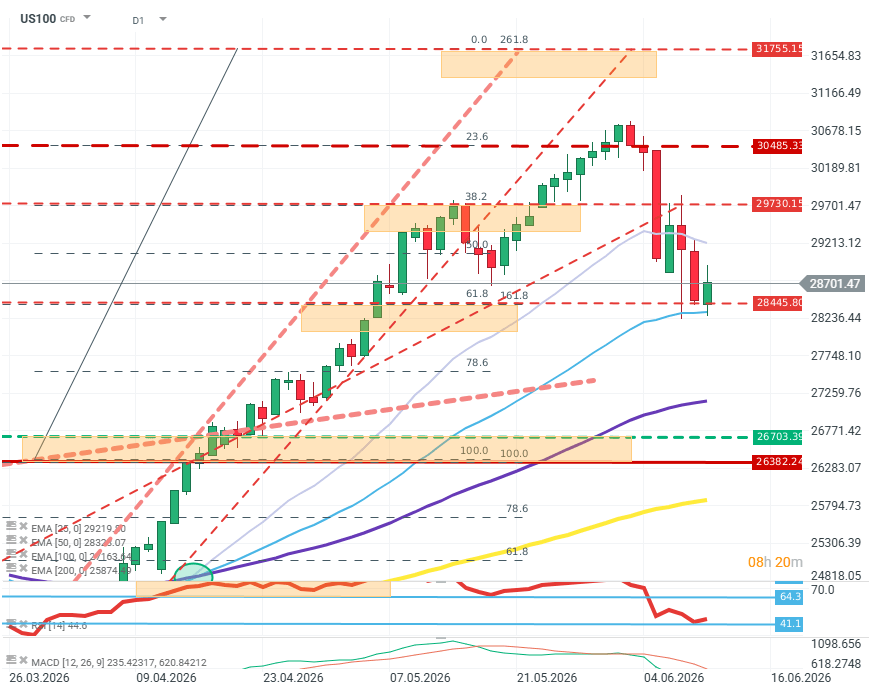

US100 (D1)

Buyers managed to defend the resistance zone at 28,440, where the 61.8% and 161.8% Fibonacci levels intersect. The 50-day EMA is also located at this level. The EMA momentum structure remains strongly bullish, and RSI has already fallen to around 40, which creates favorable conditions for an upward corrective move. The first target for demand is resistance at the 38.2% Fibonacci level. If gains break down and price falls below the last resistance, the next support for buyers is the 78.6% Fibonacci level, i.e., around 27,500 USD. Source: xStation5

Company news

- Oracle (ORCL.US): The company released results for Q2 FY2026; the share price is down about 8% in after-hours trading. Revenue rose 21% y/y to $19.2 billion, and EPS came in at $2.11. Particularly positive for investors was cloud segment revenue growth of as much as 90%, and receivables increased by 363% y/y. However, strong results were not enough to divert attention from another huge jump in CAPEX. Capital expenditures are now $55.7 billion for the fiscal year.

- Navan (NAVN.US): The company operates an AI platform supporting travel planning and expense settlement. Q2 results showed non-GAAP EPS rising to $0.08, eight times market expectations, while revenue grew to $220 million, up 40% y/y. Most important, however, may be the 50% y/y increase in bookings, which - together with raising the revenue forecast to over $900 million for the fiscal year—has the stock up about 50% in after-hours trading.

- Sandisk (SNDK.US): Oracle’s huge CAPEX weighed on the company’s valuation, but reaffirmed commitments from hyperscalers are supporting valuations of semiconductor and memory manufacturers. Sector gains are in the 4–6% range.

- Firefly Aerospace (FLY.US): Expectations surrounding a SpaceX IPO are supporting valuations of space-sector companies. The stock is up more than 4%.

- Adobe (ADBE.US): The company is set to report results after the session ends. The market expects EPS above $5.8 and revenue around $6.5 billion. Beyond the numbers, the key will also be messaging and guidance, especially in the context of AI.

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.