- Assets in Korean leveraged ETFs surged to a record $40 billion amid AI-driven market euphoria, with nearly half of the exposure coming from offshore products. The KOSPI plunged almost 10% in a single session, highlighting how concentrated positioning can amplify market moves.

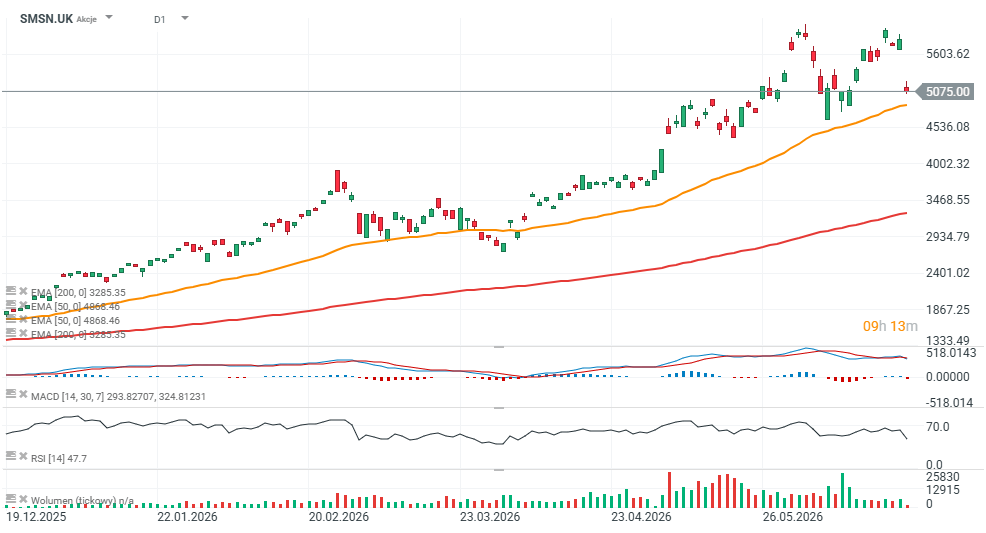

- Samsung's UK-listed ADRs fell more than 10% as investors reassessed momentum in the KOSPI, an index heavily dominated by Korean technology giants that have been among the biggest beneficiaries of the AI investment boom.

- Goldman Sachs estimates that a 5% market move could trigger approximately $4.7 billion of dealer rebalancing flows in Korean leveraged ETFs, equivalent to roughly 13% of average daily turnover on the Korean stock market.

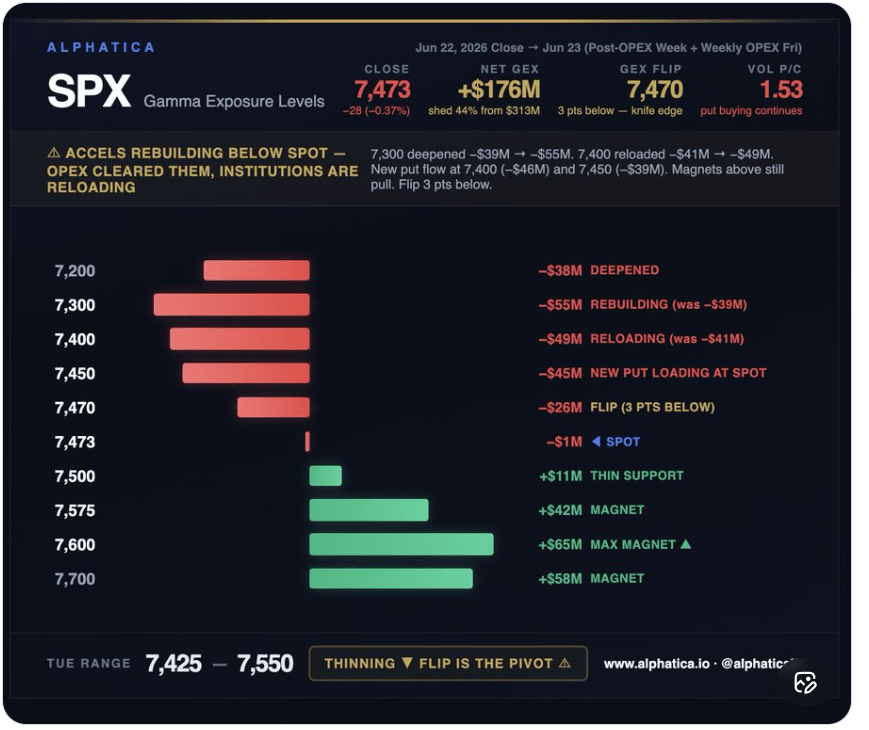

- Net Gamma Exposure (GEX) on the S&P 500 declined 44% in a single session, while the 7470 level—just two points below the June 22 close—remains a critical threshold separating a stabilizing positive-gamma environment from a potentially more volatile market regime.

- Assets in Korean leveraged ETFs surged to a record $40 billion amid AI-driven market euphoria, with nearly half of the exposure coming from offshore products. The KOSPI plunged almost 10% in a single session, highlighting how concentrated positioning can amplify market moves.

- Samsung's UK-listed ADRs fell more than 10% as investors reassessed momentum in the KOSPI, an index heavily dominated by Korean technology giants that have been among the biggest beneficiaries of the AI investment boom.

- Goldman Sachs estimates that a 5% market move could trigger approximately $4.7 billion of dealer rebalancing flows in Korean leveraged ETFs, equivalent to roughly 13% of average daily turnover on the Korean stock market.

- Net Gamma Exposure (GEX) on the S&P 500 declined 44% in a single session, while the 7470 level—just two points below the June 22 close—remains a critical threshold separating a stabilizing positive-gamma environment from a potentially more volatile market regime.

Investors trying to assess Wall Street's momentum have largely focused on U.S. options markets, dealer gamma flows, and the impact of quarterly options expiration (OPEX) on the S&P 500. Goldman Sachs, however, points to a potentially new source of risk: the rapidly expanding leveraged ETF market in South Korea. According to the bank, assets held in Korean leveraged ETFs have reached a record $40 billion. Importantly, nearly half of that exposure comes from funds listed outside Korea, increasing the scale of potential cross-border rebalancing flows.

Weakness is already visible today in shares of Korean heavyweight Samsung (SMSN.UK), and Korea increasingly appears to be acting as a useful barometer of concentration risk across global markets. Without giants such as Samsung Electronics, SK Hynix, and LG Electronics, the Korean equity index would be trading nearly flat this year. Instead, it has rallied almost 90% year-to-date after investors began viewing Korean technology companies as critical beneficiaries of the global AI expansion.

The next major catalyst arrives tomorrow, when Micron Technology—one of the key beneficiaries of the memory-chip bull market—reports earnings after the U.S. close. On Friday, investors will also receive the latest U.S. PCE inflation report.

Source: xStation5

Dealer Gamma Is Becoming a Focus Again

Analysis of the S&P 500 options structure based on Alphatica data shows that protective positioning has been rebuilt remarkably quickly following quarterly options expiration.

Net Gamma Exposure (GEX) fell by 44% in a single session, declining from $313 million to $176 million. This suggests the market currently has a much weaker stabilizing gamma cushion than it did only a few days ago.

At the same time, institutions have been aggressively adding put exposure close to current index levels:

-

The 7400 strike accumulated approximately $46 million of new put gamma.

-

The 7450 strike accumulated approximately $39 million of new put gamma.

-

The put/call volume ratio rose to 1.53.

This suggests that large investors are not hedging against a distant crisis scenario but against downside risks that could emerge at any time.

Why Is 7470 Such an Important Level?

According to Alphatica's analysis, the S&P 500 gamma flip currently sits near 7470, almost exactly at the latest market close.

Above this level, positive dealer gamma tends to stabilize price action and support moves toward higher resistance zones:

-

7575

-

7600

-

7700

-

7800

A move below 7470 could trigger the opposite effect. In that scenario, dealers may be forced to sell futures as the market declines, potentially increasing volatility and accelerating downside momentum unless buyers step in quickly. The strongest downside acceleration zones currently sit around 7450 and 7400.

Source: Alphatica.io

Korea Could Amplify Market Moves

Goldman Sachs notes that the record popularity of leveraged ETFs in Korea could further increase market volatility.

According to the bank's estimates, a 5% move in the market could force dealers supporting Korean leveraged ETFs to rebalance approximately $4.7 billion worth of exposure.

That figure represents roughly 13% of average daily turnover on the Korean stock market.

The numbers become even more striking at the individual stock level.

Goldman Sachs estimates that the largest potential rebalancing flows would affect Korea's leading technology companies:

-

SK Hynix: approximately $2.0 billion

-

Samsung Electronics: approximately $1.45 billion

These flows correspond to roughly 25% and 21% of each company's average trading volume, respectively.

This means that even if corporate fundamentals remain unchanged, the mechanical nature of leveraged ETF rebalancing can temporarily generate significant price movements.

Is Another Volmageddon Coming?

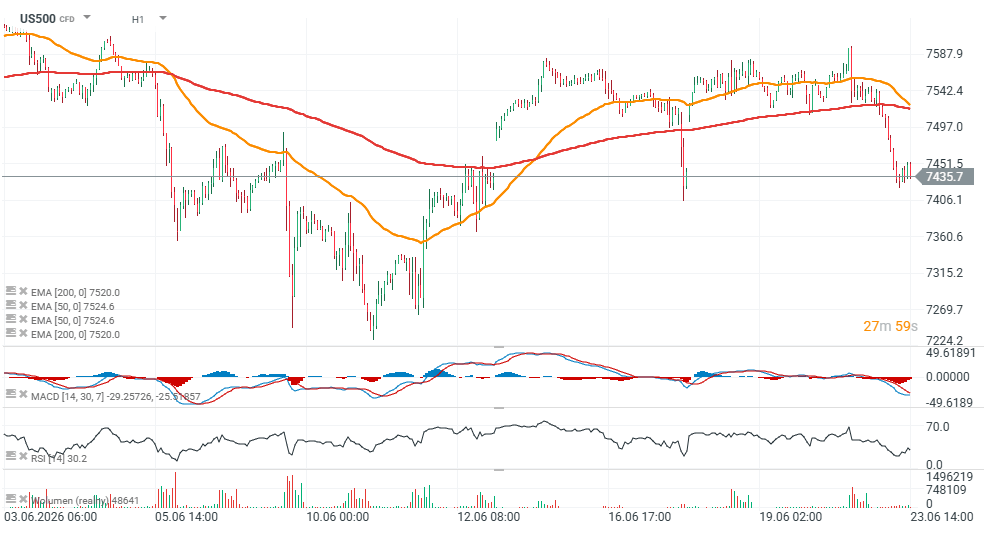

For now, there are no signs of extreme fear in the market. The S&P 500 has pulled back roughly 170 points from its recent high, a relatively modest correction given the strength of the preceding rally.

However, the combination of rapidly rebuilding negative gamma exposure in U.S. options markets and record leveraged ETF exposure in Asia creates an environment that may be more sensitive to sharp market moves. Lower summer liquidity could further amplify volatility.

Even relatively ordinary catalysts—such as softer inflation data, a more hawkish Federal Reserve, or disappointing earnings from major technology companies—could trigger automatic hedging and rebalancing flows on both sides of the Pacific.

The coming days may therefore serve as a test not only of the 7470 level on the S&P 500, but also of the broader market's ability to absorb the growing influence of mechanical trading strategies and leveraged investment products.

S&P 500 futures are trading lower ahead of the U.S. cash open, although volumes remain relatively light. As a result, what happens during the first 20-30 minutes of trading in New York may prove particularly important for determining whether today's weakness develops into a larger move or remains a short-term pullback.

Source: xStation5

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Hormuz Deal Moves Closer

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.