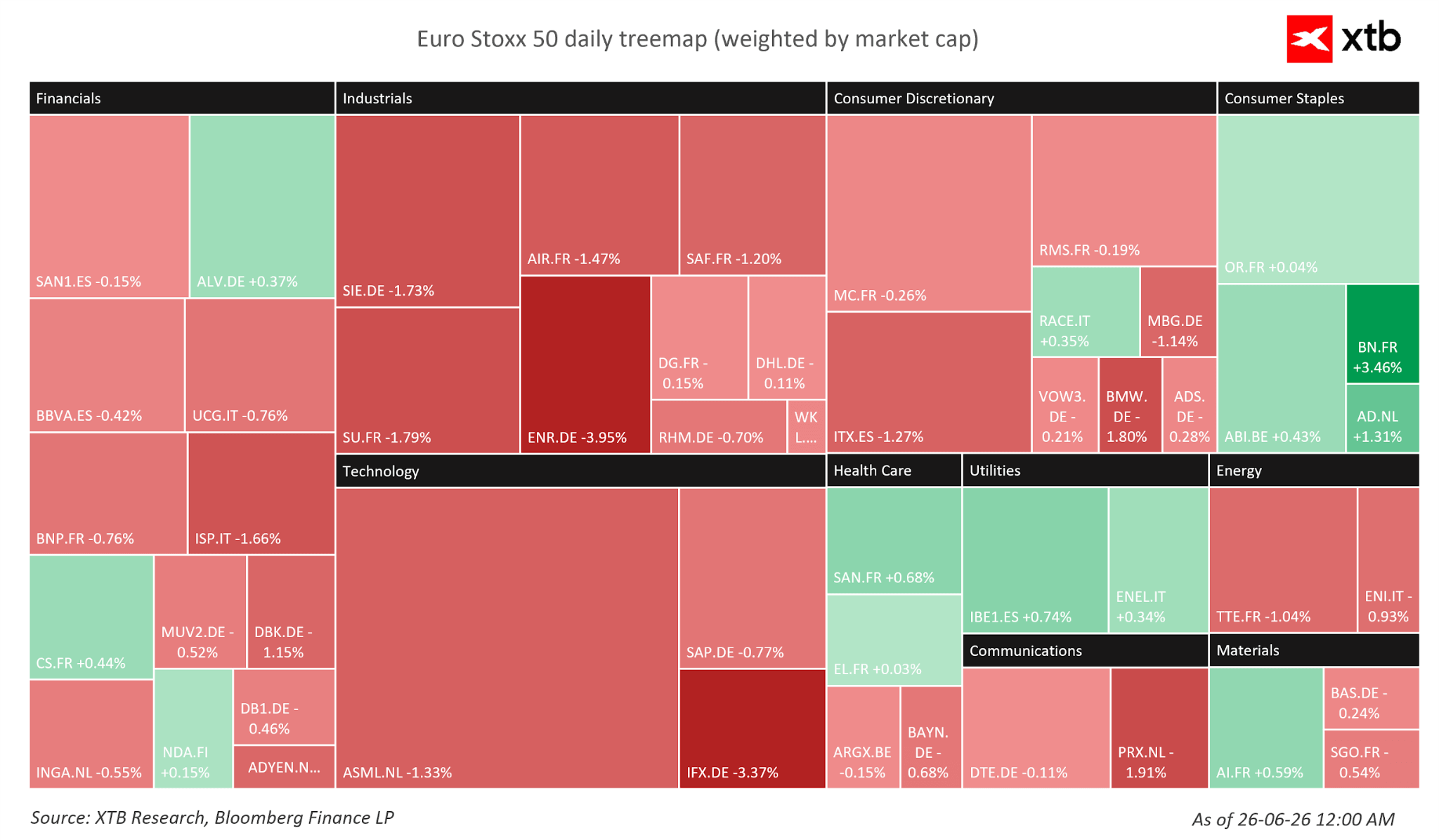

Chip and advanced technology manufacturers are recording declines on trading floors in Frankfurt, Paris, and Amsterdam. European sector leaders such as ASML and Infineon are following in the footsteps of American giants. Negative sentiment is also enveloping companies in the automotive and heavy industry sectors.

Figure 1: Sector Heatmap in Euro Stoxx 50 (26.06.2026)

Source: XTB Research, 26.05.2026

Source: XTB Research, 26.05.2026

With the cooling of the USA-Iran conflict, speculative enthusiasm surrounding companies in the broadly defined AI ecosystem is fading. Increasingly, it takes more to meet the very high expectations of investors, and billion-dollar outlays on infrastructure and data centres are being verified with greater scrutiny.

Furthermore, the second quarter, which was exceptionally successful for the tech sector, is coming to an end. Due to rebalancing, especially in institutional and balanced funds, the final days of June may be demanding for the companies that have performed best in recent months. Fund managers are often compelled to restore the appropriate portfolio structure (e.g., 60% equities, 40% bonds), which partly explains the recently recorded price increases for government bonds of the world's largest economies.

Companies

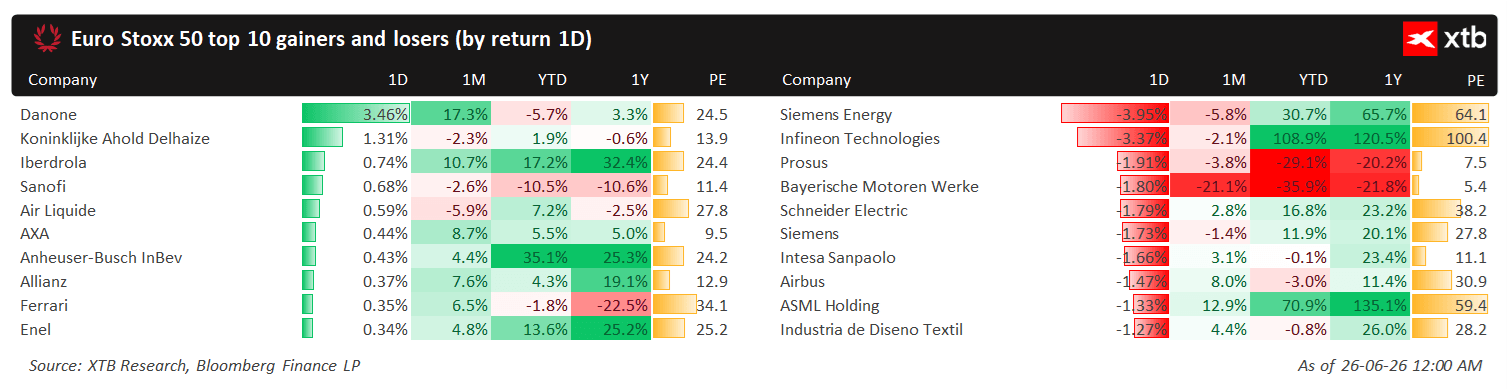

While as recently as yesterday, following the publication of results far better than expected by Micron, we wrote about the significant strengthening of Infineon Technologies and ASML, today both companies are among the biggest losers, recording declines of 3.4% and 1.3%, respectively.

Figure 2: Winners and losers in Euro Stoxx 50 (26.06.2026)

Source: XTB Research, 26.06.2026

Source: XTB Research, 26.06.2026

German giants are also losing ground – Siemens (-4%) and BMW (-1.8%), the latter of which has weakened by over 20% on a monthly scale. The sharp decline in the share price of the Bavarian automotive manufacturer is largely due to a slump in sales in China (down as much as 18% year-on-year). Chinese consumers are mass-migrating to domestic, local electric vehicle brands such as BYD, Xiaomi, and Li Auto.

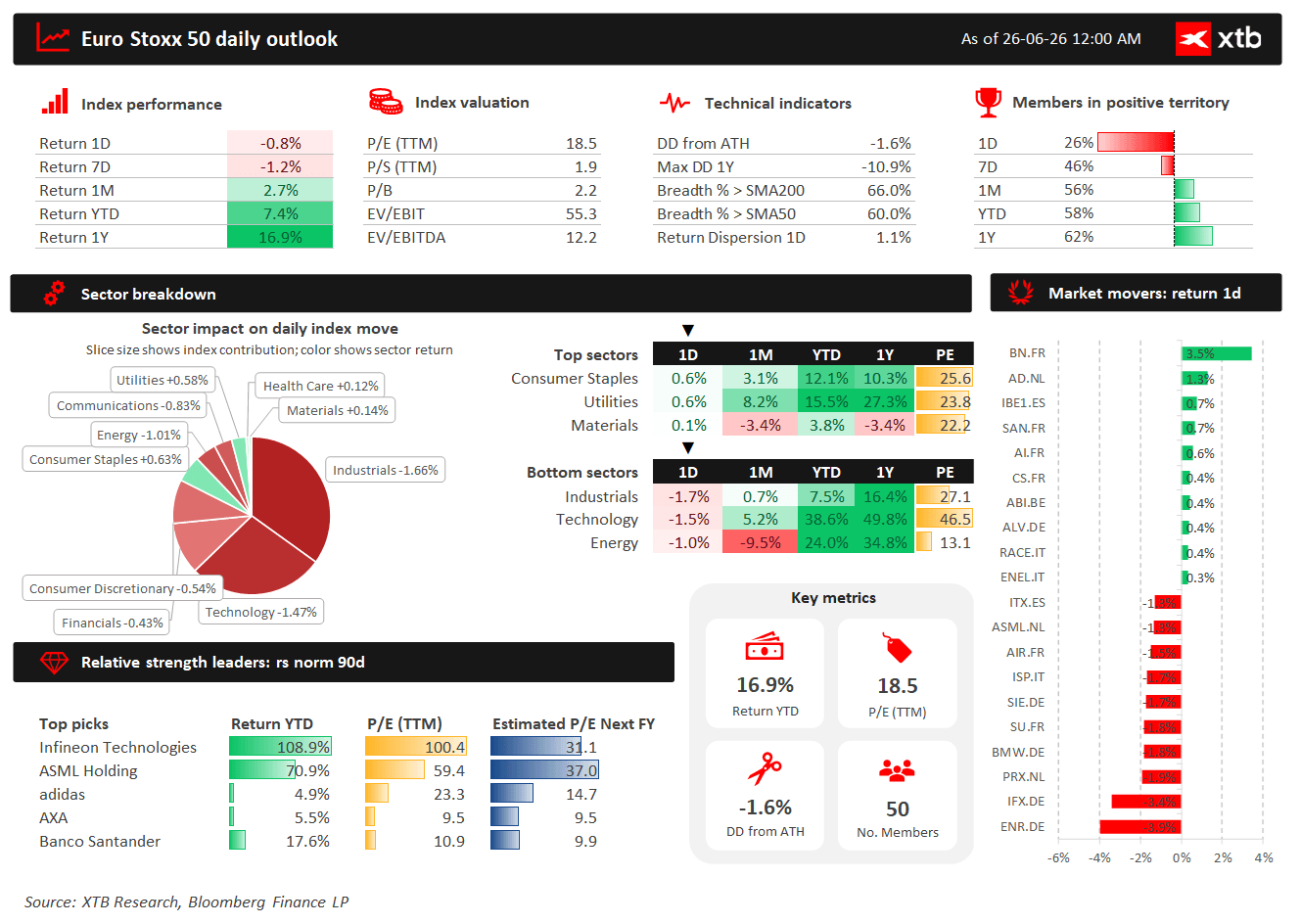

Indices

It is not only the pan-European Euro Stoxx 50 that is falling (-0.8%). The German DAX (-1.2%), French CAC40 (-0.8%), Italian FTSE MIB (-1.3%), and Polish WIG20 (-1.6%) are also flashing red.

Figure 3: Dashboard for Euro Stoxx 50 (26.06.2026)

Source: XTB Research, 26.06.2026

Source: XTB Research, 26.06.2026

Futures contracts also suggest that the US stock market should open in the red.

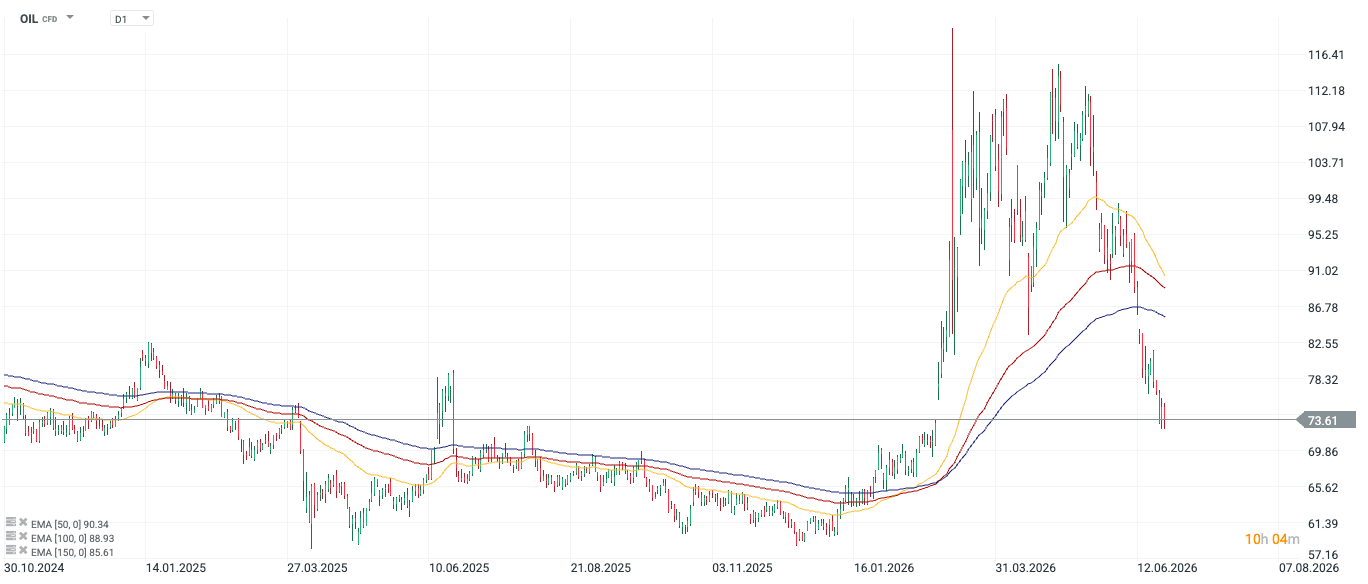

Energy Commodities

According to the words of the US Secretary of Energy, Chris Wright, an average of approximately 72 vessels have passed through the Strait of Hormuz over the past few days, transporting nearly 20 million barrels of crude oil per day. Kpler, a company specialising in analytics regarding the global commodities and maritime transport market, also reports that 70 vessels passed through the strait on 24 June. This is still about half as much as before the outbreak of the war, yet the trend is clearly upward, which may explain further price declines.

- We currently pay just over $73 for a barrel of Brent crude oil.

- The cost of a WTI barrel is approximately $70.

Figure 4: OIL [D1] (30.10 - 26.06)

Source: xStation, 26.05.2026

Source: xStation, 26.05.2026

—

Michał Jóźwiak, Financial Markets Analyst, XTB

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Hormuz Deal Moves Closer

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.