- European stock markets are rising on Tuesday, driven by renewed optimism in the technology sector.

- Morgan Stanley expects European corporate earnings to grow by more than 16% this year.

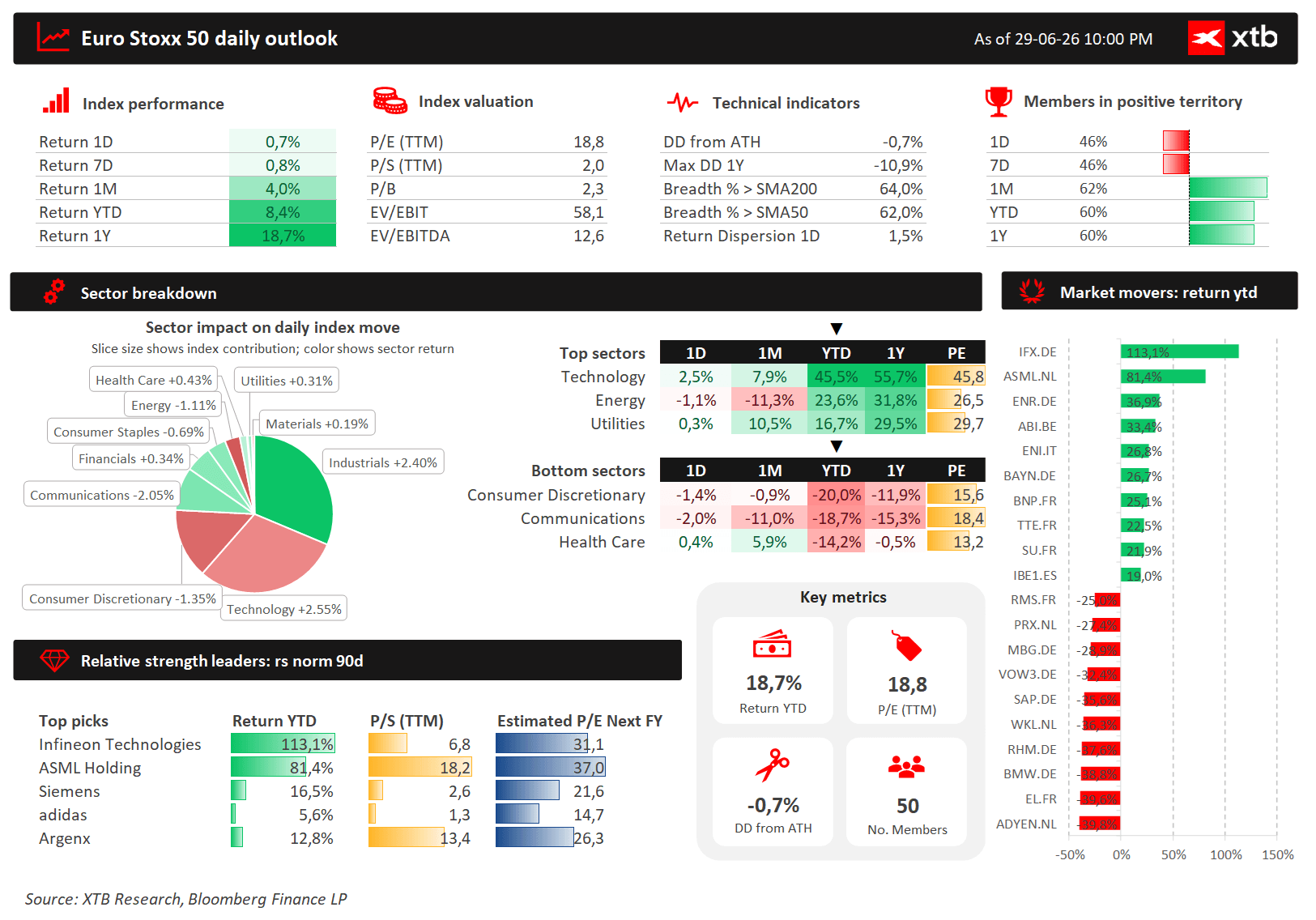

- The Euro Stoxx 50 remains close to its all-time high, trading just around 0.7% below the record level.

- European stock markets are rising on Tuesday, driven by renewed optimism in the technology sector.

- Morgan Stanley expects European corporate earnings to grow by more than 16% this year.

- The Euro Stoxx 50 remains close to its all-time high, trading just around 0.7% below the record level.

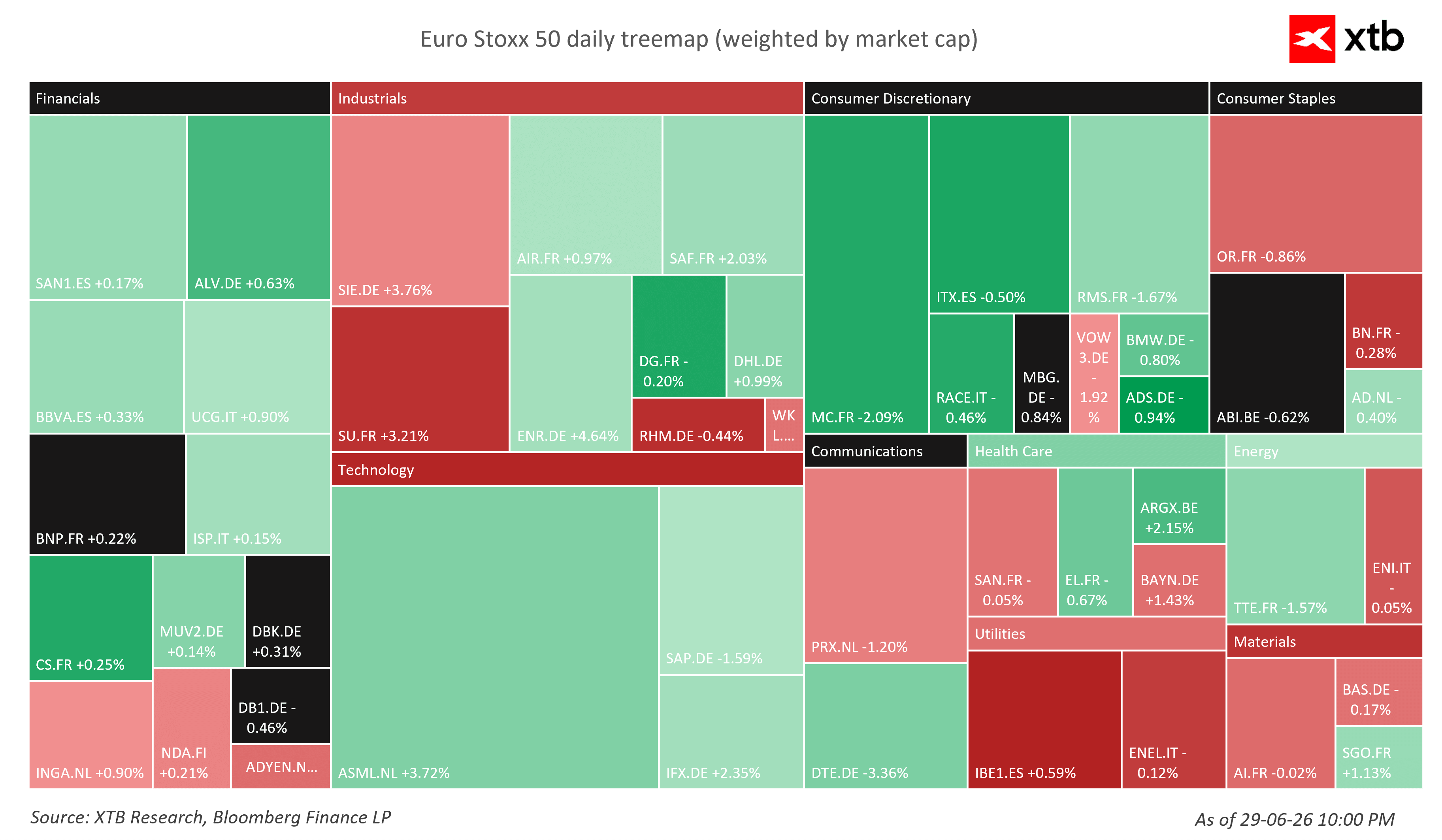

European equities opened Tuesday's session with solid gains, supported by strong sentiment from both Asia and Wall Street. The STOXX 50 advanced around 0.6%, while the broader STOXX 600 climbed nearly 1%. Technology stocks once again led the rally as investors returned to AI-related names following the recent correction and improving expectations for semiconductor demand. Among the session's top performers were Europe's leading chipmakers. Shares of ASML rose more than 3.5%, Infineon gained around 2.5%, and STMicroelectronics advanced nearly 3%, highlighting renewed investor appetite for AI infrastructure and semiconductor companies. Meanwhile, the U.S. dollar strengthened across the market, while Brent crude attempted to recover toward $74 per barrel.

Euro Stoxx 50 remains close to record highs

The Euro Stoxx 50 continues to trade near its all-time highs, sitting only around 0.7% below its record, while delivering a gain of nearly 8.5% year-to-date.

Technology remains the strongest-performing sector both on the day and since the beginning of the year, whereas consumer-related stocks and communication services continue to lag behind. Roughly 64% of the index's constituents are trading above their 200-day moving averages, suggesting that the long-term uptrend remains intact.

Among the strongest relative performers are Infineon, ASML and Siemens, while BMW, SAP, Mercedes-Benz and Adyen rank among this year's weakest large-cap stocks. With the index trading at approximately 18.8x forward earnings, valuations remain reasonable compared with major U.S. benchmarks, reinforcing the case for gradually increasing investor interest in European equities.

Source: XTB Research

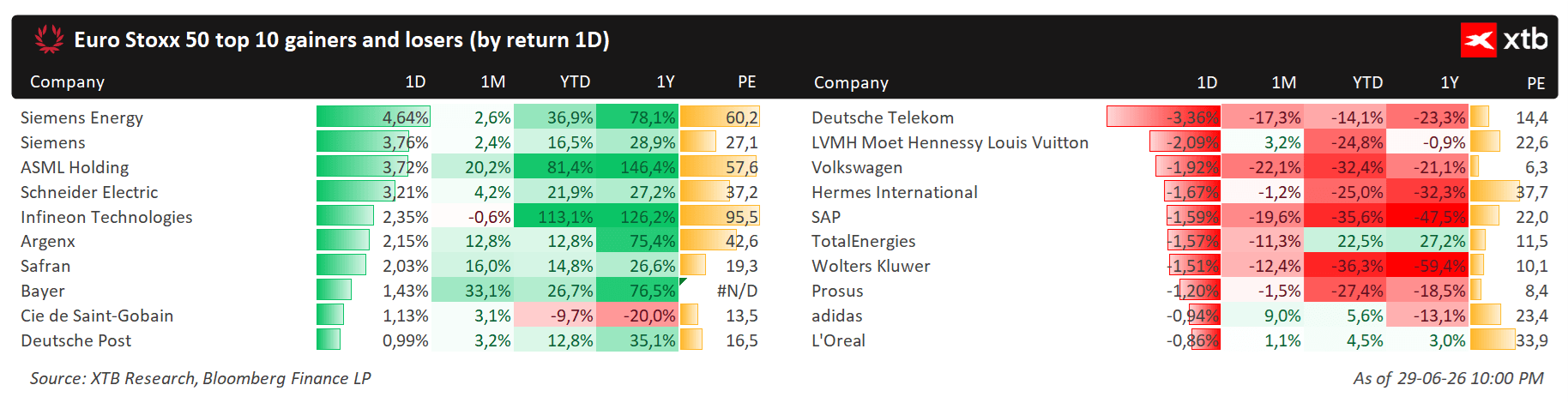

Industrials and AI leaders dominate Tuesday's session

Tuesday's gains were driven primarily by industrial, technology and energy-transition companies. Siemens Energy (+4.6%), Siemens (+3.8%), and ASML (+3.7%) led the advance, underlining continued capital inflows into AI-related infrastructure and electrification themes.

Schneider Electric, Infineon and Safran also posted strong gains as investors rotated back into European industrial leaders. On the downside, telecommunications, luxury goods and automotive stocks underperformed, with Deutsche Telekom, LVMH and Volkswagen among the weakest names.

Despite today's declines, several lagging stocks continue to post positive returns over the past year, while this year's leaders maintain exceptionally strong long-term momentum.

Source: XTB Research

Source: XTB Research

Source: XTB Research

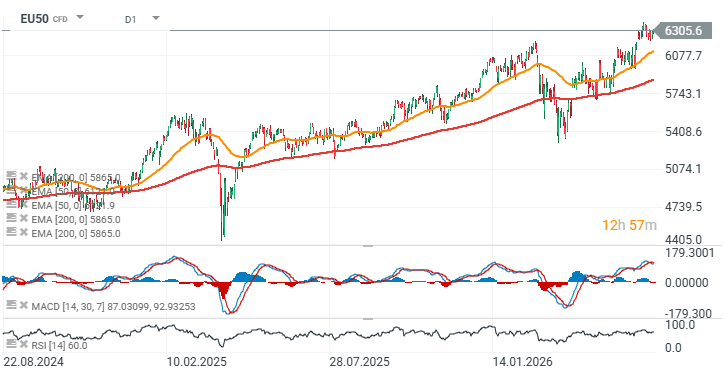

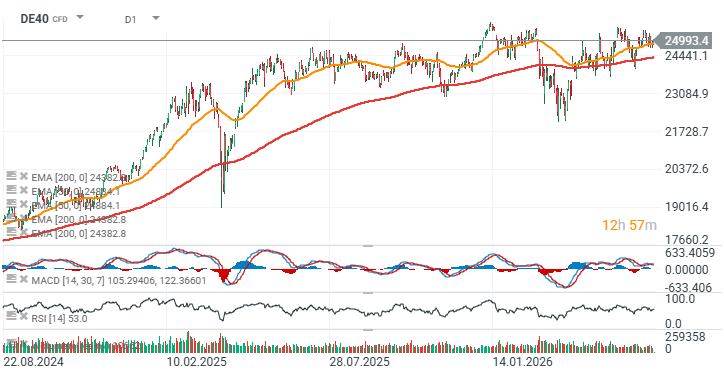

EU50 and DE40 charts

Source: xStation5

Source: xStation5

Morgan Stanley: Europe could outperform through broader diversification

Morgan Stanley believes European equities have room to extend their rally in the second half of the year. According to the bank's strategists, investors are not abandoning artificial intelligence, but are increasingly looking to diversify away from the heavy concentration of capital in U.S. mega-cap technology stocks. Europe is emerging as one of the main beneficiaries of this rotation.

European equity indices have delivered year-to-date returns broadly in line with the S&P 500 after recovering from earlier geopolitical-driven weakness. Morgan Stanley argues that this is more than a temporary rebound and may represent the beginning of a broader reallocation of global capital.

The decline in oil prices following the U.S.-Iran agreement has improved the outlook for European companies by reducing energy costs and supporting corporate margins. However, the bank believes the main catalyst behind renewed inflows is not geopolitics but increasing volatility across the U.S. AI sector. Investors are seeking to maintain AI exposure while broadening regional diversification.

Around 90% of this year's gains in European equity indices have been generated by AI-related sectors, including semiconductors, technology hardware, capital goods, and copper and mining companies.

Morgan Stanley also notes that European listed companies are far less dependent on domestic economic conditions than commonly assumed. Around 55% of their revenues are generated outside Europe, reducing their sensitivity to weaker GDP growth or disappointing PMI data.

Consensus forecasts call for more than 16% earnings growth for European companies this year, a figure the bank believes is still underestimated by investors. European banks remain particularly attractive thanks to higher interest rates, improving profitability, ongoing share buyback programs and solid dividend distributions.

According to the bank, sectors benefiting from higher inflation—including banks, real assets and AI-related businesses—now account for roughly 60% of total European corporate earnings, making the region well positioned for the current macroeconomic backdrop.

Morgan Stanley also highlights that the long-standing valuation discount of European equities versus the U.S. market has started to narrow after many years, potentially creating further room for international capital inflows.

For the second half of the year, the bank's preferred sectors include semiconductors, copper and mining companies, banks, capital goods manufacturers, and utilities, with the latter expected to benefit from both the energy transition and continued investment in AI infrastructure.

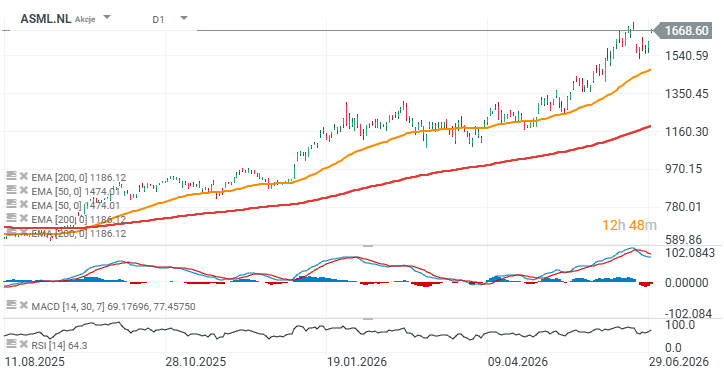

ASML (ASML.NL) chart – D1 interval

Source: xStation5

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

Berkshire earnings: What do the reports say about the market’s direction?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.