Markets and macroeconomics

-

European indices are rising on Tuesday – the German DAX is up by around 1.3%, the French CAC 40 by 0.9%, the FTSE 100 by around 0.7%, and the pan-European Stoxx 600 is up by nearly 0.8–0.9%. The main catalyst for the gains is President Donald Trump’s decision to call off the planned strike on Iran following requests from allies in the Persian Gulf – Saudi Arabia, Qatar and the UAE – who urged that diplomacy be given more time.

-

Trump announced that there is a “very good chance” of a nuclear deal with Iran, which has clearly eased geopolitical tensions in the Middle East. Crude oil fell by around 2%, although Brent remains above $100 a barrel – contracts for July delivery are trading at around $109.8. The dollar has returned to an upward trajectory following Monday’s rebound – the Bloomberg Dollar Spot Index is up 0.3%, and the USDIDX is hovering around 99.13–99.14, reflecting fragile market sentiment.

-

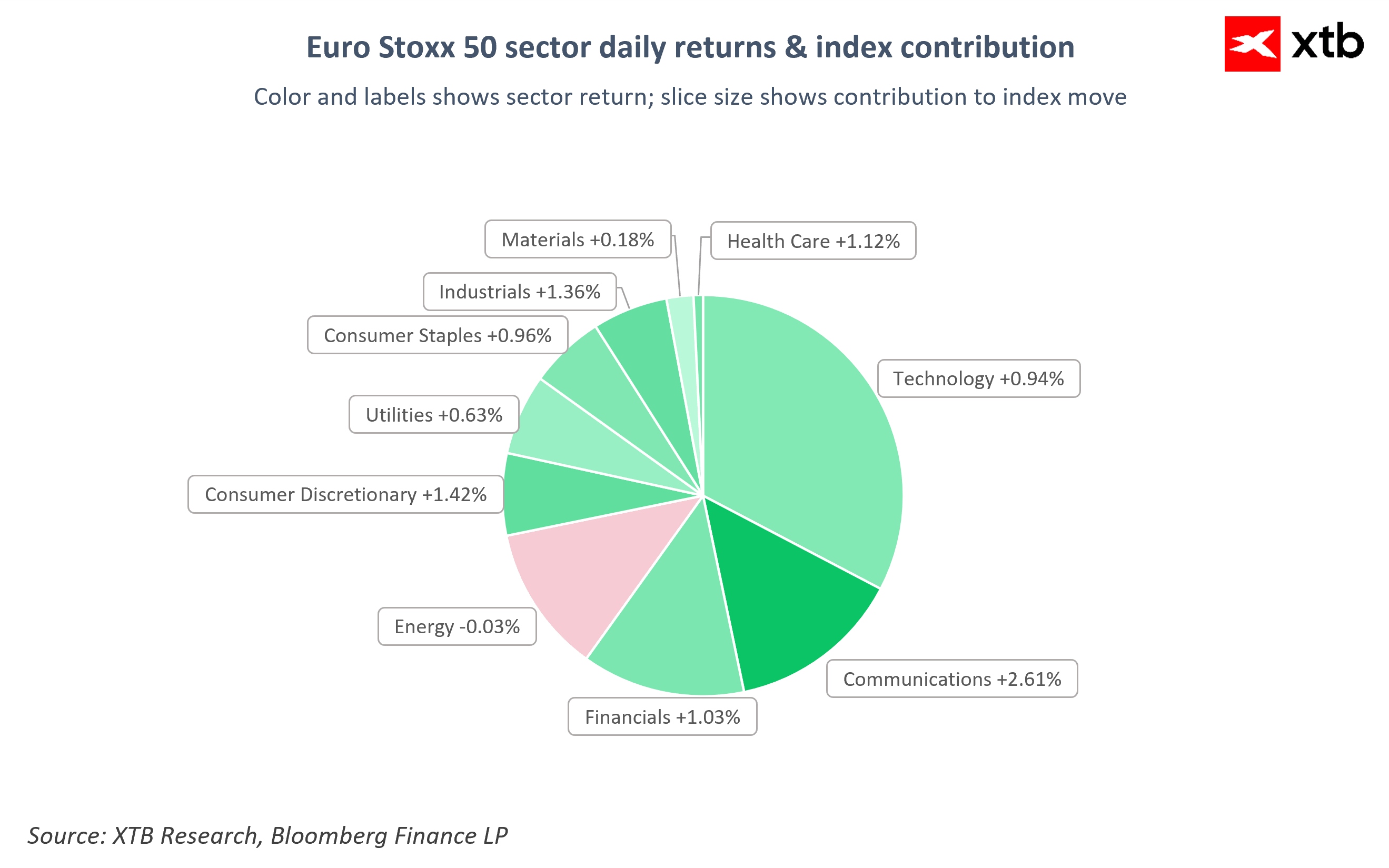

Among the Euro Stoxx 50 sectors, the leaders are: Transport (+2.61%), Consumer Discretionary (+1.42%), Industrials (+1.36%) and Health Care (+1.12%). The Energy sector is the only one in negative territory (-0.03%), dragged down by weakness in TotalEnergies and Eni, whilst Materials are recording only a symbolic rise (+0.18%).

Index and sector chart – What drives the market?

The Communications sector (+2.61%), along with Consumer Discretionary (+1.42%) and Industrials (+1.36%), are driving the gains in the Euro Stoxx 50 today, whilst Energy is the only sector to post a slight loss (-0.03%). Source: XTB

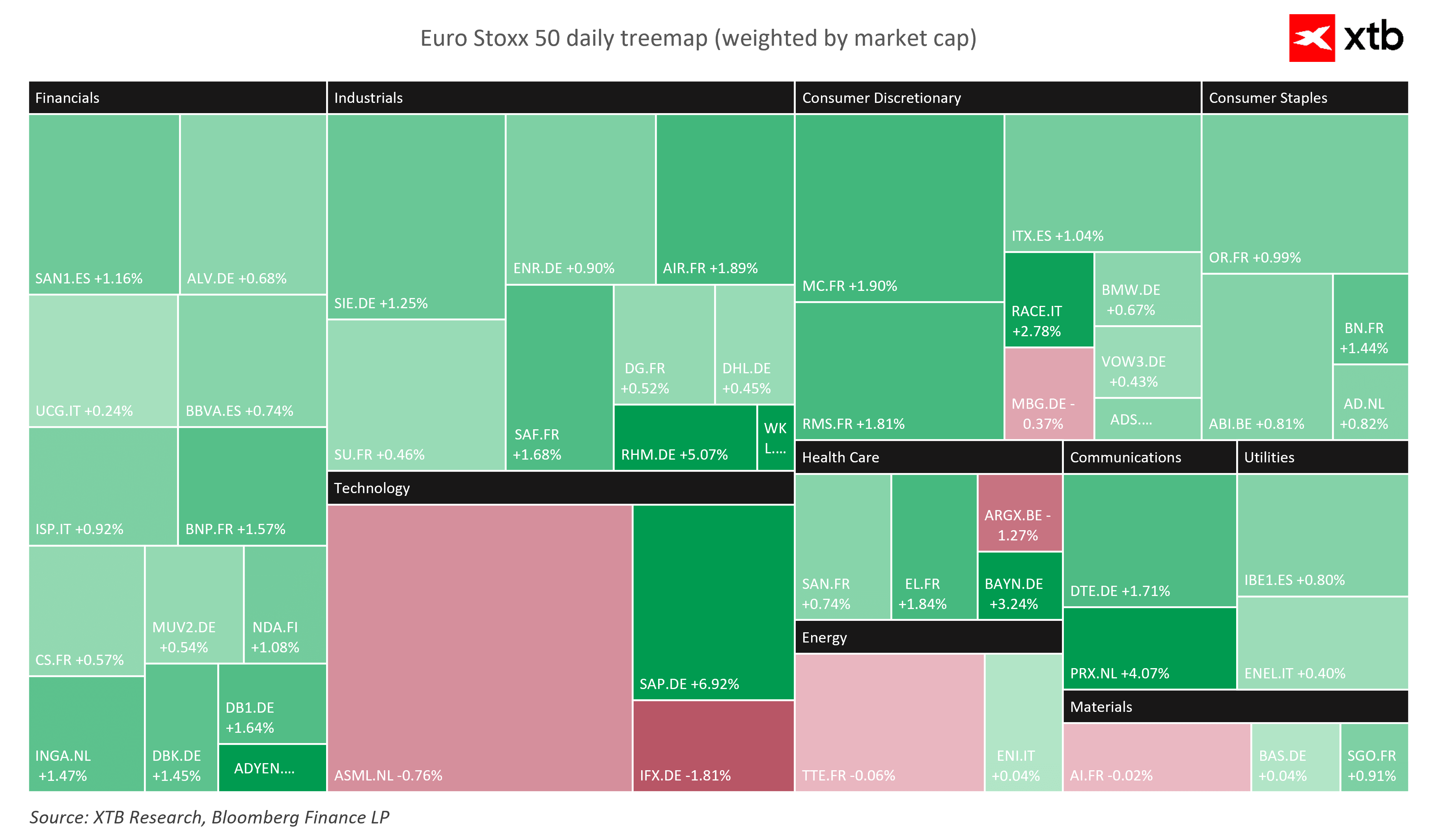

The technology sector (SAP +6.92%, Rheinmetall +5.07%) and consumer and industrial goods are leading the gains on the Euro Stoxx 50, whilst Infineon (-1.81%) and ASML (-0.76%) remain among the few stocks in the red. Source: XTB

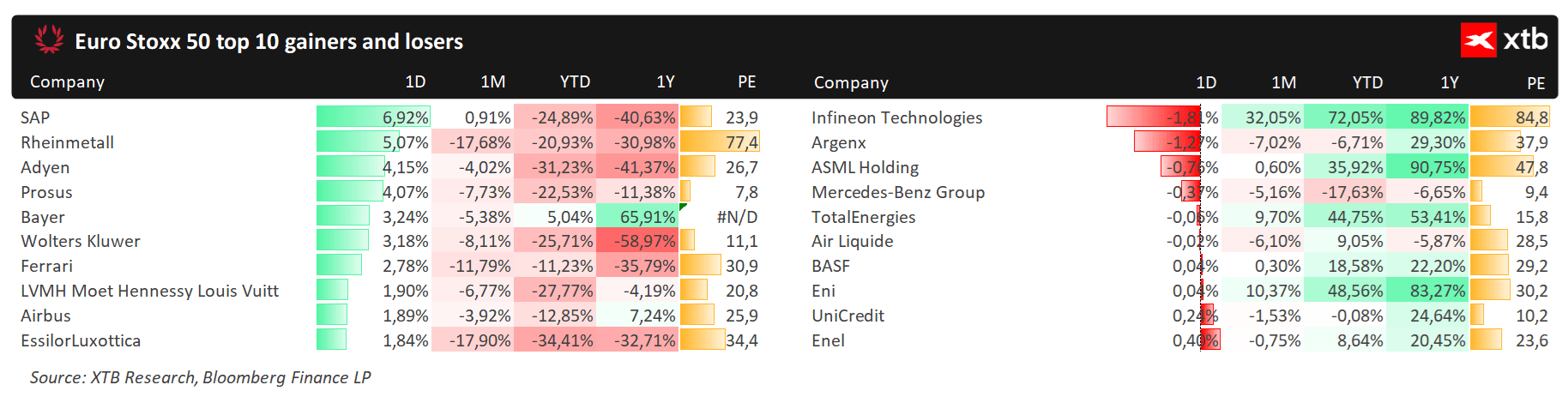

Today’s winners and losers on the European market; companies included in the EuroStoxx 50 and EU50 indices. Source: XTB

Companies

-

SAP is the day’s biggest gainer on the Euro Stoxx 50, jumping by nearly +6.9% – the company is clearly benefiting from the wave of optimism surrounding the technology sector and the return of risk appetite; year-to-date, the company is still down by nearly 25%.

-

Rheinmetall is up by over 5%, and the defence sector (+2.5%) is one of the top performers in Europe – Sweden’s Saab rose by around 4–5% following confirmation that Sweden will purchase naval frigates from France for over $4 billion, with Saab set to develop radar and weapon systems.

-

Evolution Gaming has jumped by over 11% following the announcement of a €2 billion (approx. $2.4 billion) share buyback programme, one of the largest such operations in the company’s history.

-

Vallourec is down nearly 7.8% after ArcelorMittal sold its 10% stake in the French steel tube manufacturer at a discount, generating proceeds of around €667 million.

-

Uniper is up by around 1.9–9.3% following the German government’s announcement of its intention to privatise the energy group – the government holds 99.12% of the company’s shares and plans to sell them or float the company on the stock market, which could be one of the biggest European deals of the year.

-

Infineon Technologies (-1.81%) and ASML (-0.76%) are weighing on the technology sector, even though SAP is rebounding strongly – investors are taking a selective approach to chipmakers amid uncertainty surrounding global trade and Nvidia’s upcoming results.

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.