Morgan Stanley started 2026 with a very solid and clearly high-quality quarter, which meaningfully exceeded market expectations both in terms of revenue and earnings. Importantly, this is not a result driven by a single dominant factor or a short-term market effect, but rather the outcome of broad-based strength across key business segments. At the same time, there is visible improvement in more cyclical areas such as trading and investment banking, alongside continued stability in Wealth Management, which remains the foundation of the firm’s overall revenue structure.

As a result, this is a quarter that not only delivers a positive surprise, but also reinforces the picture of a well-balanced business model capable of generating strong results across different market environments. At the same time, the report is not without nuance, as some segments remain more uneven, which limits full euphoria despite the very strong overall performance.

Key financial results

-

Net revenues: 20.58 billion USD (above expectations of 19.71 billion USD)

-

Earnings per share (EPS): 3.43 USD

-

Institutional Securities: 10.7 billion USD

-

Wealth Management: 8.52 billion USD (above expectations)

-

Equities trading: 5.15 billion USD (above expectations)

-

FICC trading: 3.36 billion USD (above expectations)

-

Investment banking: 2.12 billion USD (above expectations)

-

Net interest income: 2.7 billion USD (above expectations)

-

Deposits: 428 billion USD

-

CET1 ratio: 15.1%

-

ROE: 21%

-

ROTE: 27.1%

-

Operating expenses: 13.47 billion USD

Market reaction

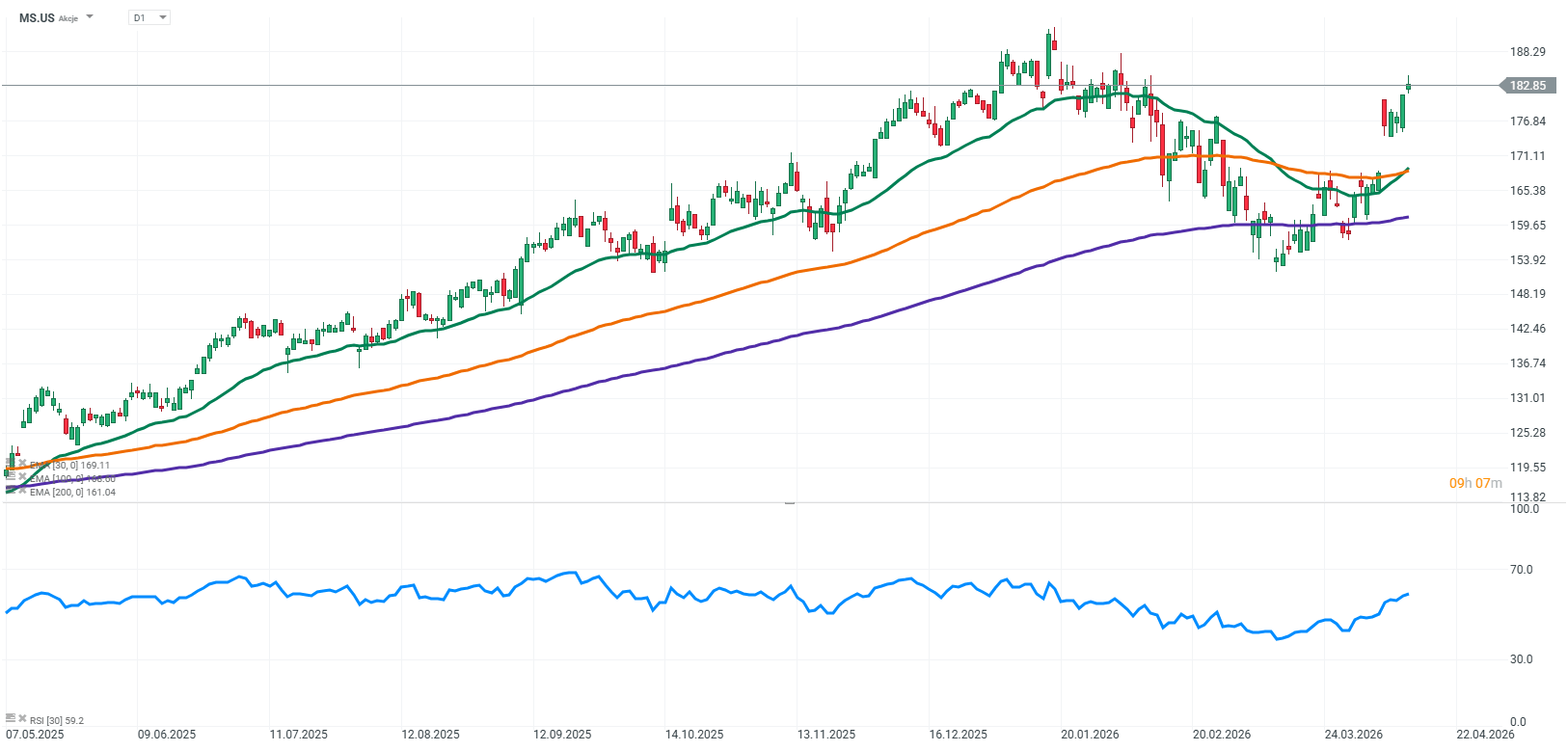

Following the release, shares are trading higher in pre-market, indicating a positive market reaction. Investors are primarily focusing on the strong trading performance and the stability of Wealth Management, which together create a high-quality earnings profile.

Trading as the main growth driver, with a positive surprise in FICC

The markets segment was the strongest part of the report. Equity trading revenues reached 5.15 billion USD, reflecting strong client activity and supportive market conditions.

Even more importantly, FICC revenue came in at 3.36 billion USD, clearly above expectations. Against a backdrop of mixed results from peers in this segment, this represents one of the key positive surprises of the quarter. It highlights that Morgan Stanley is not only benefiting from market volatility, but is also effectively monetizing it across both equities and fixed income products.

Institutional Securities and investment banking regain momentum

Institutional Securities generated record revenues of 10.7 billion USD, confirming strong client engagement and continued expansion in activity levels.

Within investment banking, advisory activity showed a clear recovery, indicating a rebound in M&A activity. At the same time, underwriting remains more uneven, as equity and debt issuance revenues came in slightly below the most optimistic forecasts, suggesting that primary markets have not yet fully normalized.

Wealth Management as a core pillar of quality and stability

Wealth Management once again confirmed its central role in the firm’s business model. The segment generated 8.52 billion USD in revenues with a very strong pre-tax margin of around 30%.

The most impressive element remains asset inflows, which reached 118 billion USD in a single quarter. More than 53 billion USD came from fee-based flows, further strengthening the recurring revenue base and improving overall earnings stability.

In practice, Morgan Stanley is increasingly operating a model where high-margin advisory and wealth management businesses balance more volatile trading-driven segments.

Costs under control and improving efficiency

Operating expenses totaled 13.47 billion USD and were broadly in line with expectations. However, higher revenues allowed for improved efficiency. The cost-to-income ratio declined to approximately 65%, indicating increasing operating leverage.

Cost discipline remains intact, while the scale of the business is starting to generate more visible benefits.

Balance sheet and risk, stable position

The capital position remains very strong. A CET1 ratio of 15.1% provides comfort for both regulators and investors. Deposits increased to nearly 428 billion USD, further strengthening funding stability.

Credit provisions amounted to 98 million USD. While slightly above expectations, they remain low in absolute terms and do not signal any meaningful deterioration in asset quality.

Weaker elements present but secondary

Despite the strong overall picture, the report included several weaker elements. These included lower momentum in parts of underwriting, outflows in equity-related assets, and a slightly weaker Investment Management segment.

However, these factors do not change the overall picture, as they remain secondary relative to the strong performance in core business lines.

Key takeaways

The first quarter of 2026 for Morgan Stanley should be clearly assessed as very strong and high quality. The bank delivered better-than-expected results, supported by strong trading performance, a positive surprise in FICC, and stable, highly profitable Wealth Management.

This was a strong quarter, but not an euphoric one. Full euphoria was held back by a few weaker elements, which nevertheless do not change the overall picture. Overall, it remains a very solid result that confirms the high quality of the business and the bank’s ability to generate strong performance in a supportive market environment.

Source: xStation5

US OPEN: Deeper sell-off and a SaaS rebound

Mercedes earninigs: Is optimism justified?

ASML sell-out: Dreams and rumors will not break the monopoly

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.