🌍 Geopolitics

- The U.S.-Iran talks in Islamabad ended in failure over the weekend—the two sides were unable to reach an agreement on Iran’s nuclear program. The ceasefire is still formally in effect, but hopes for another round of dialogue are slim, especially following Washington’s latest escalatory moves.

-

President Trump confirmed this morning on Truth Social that the blockade of Iranian ports will take effect at 10:00 a.m. ET (2:00 p.m. GMT). The U.S. will intercept all ships entering or leaving Iranian ports that are carrying Iranian goods, including oil and gas.

-

CENTCOM clarified that the blockade does not mean the Strait of Hormuz will be closed to transit traffic; however, Iran has warned that any approach by U.S. ships to the Strait will be considered a violation of the ceasefire. Israel has raised its alert level.

-

Reports have indicated that Trump and his advisers are considering resuming limited strikes against Iran if the blockade proves ineffective. Analysts view the blockade primarily as a means of exerting pressure, but the market is pricing in the risk of further escalation.

🗳️ Politics—Hungary

-

In Sunday’s parliamentary elections in Hungary, the opposition party Tisza Péter Magyar won approximately 53% of the vote amid a historically high turnout. With 98.93% of the votes counted, Tisza holds 138 seats, Fidesz 55, and Mi Hazánk 6 out of the 199 seats in parliament.

-

Magyar has secured a constitutional majority (the threshold is 133 seats), bringing an end to Viktor Orbán’s 16-year rule. Europe has sent its congratulations, and the markets are interpreting the result as a sign of Hungary’s rapprochement with the EU—up to €90 billion in aid for Ukraine, previously blocked by Budapest, could now be released.

-

The EUR/USD pair reacted only slightly to this news—it is under pressure from a stronger dollar and rising energy prices in Europe. In the long term, however, the election result is positive for the euro and EU assets.

📉 Asian Markets

-

The Asian session was marked by risk-off sentiment: the Nikkei 225 fell 1.0%, weighed down by rising energy prices and a 29-year high in yields on Japanese 10-year bonds, which rose amid inflation concerns. The Hang Seng fell 1.5%, and the Shanghai Composite dropped 0.3%.

-

The ASX 200 fell 0.5%—technology and mining stocks dragged the index down, although the energy sector posted gains.

-

Euro Stoxx 50 futures are down 1.8% after closing up 0.5% on Friday. U.S. futures are also down: US500 -0.70%, US100 -0.81%.

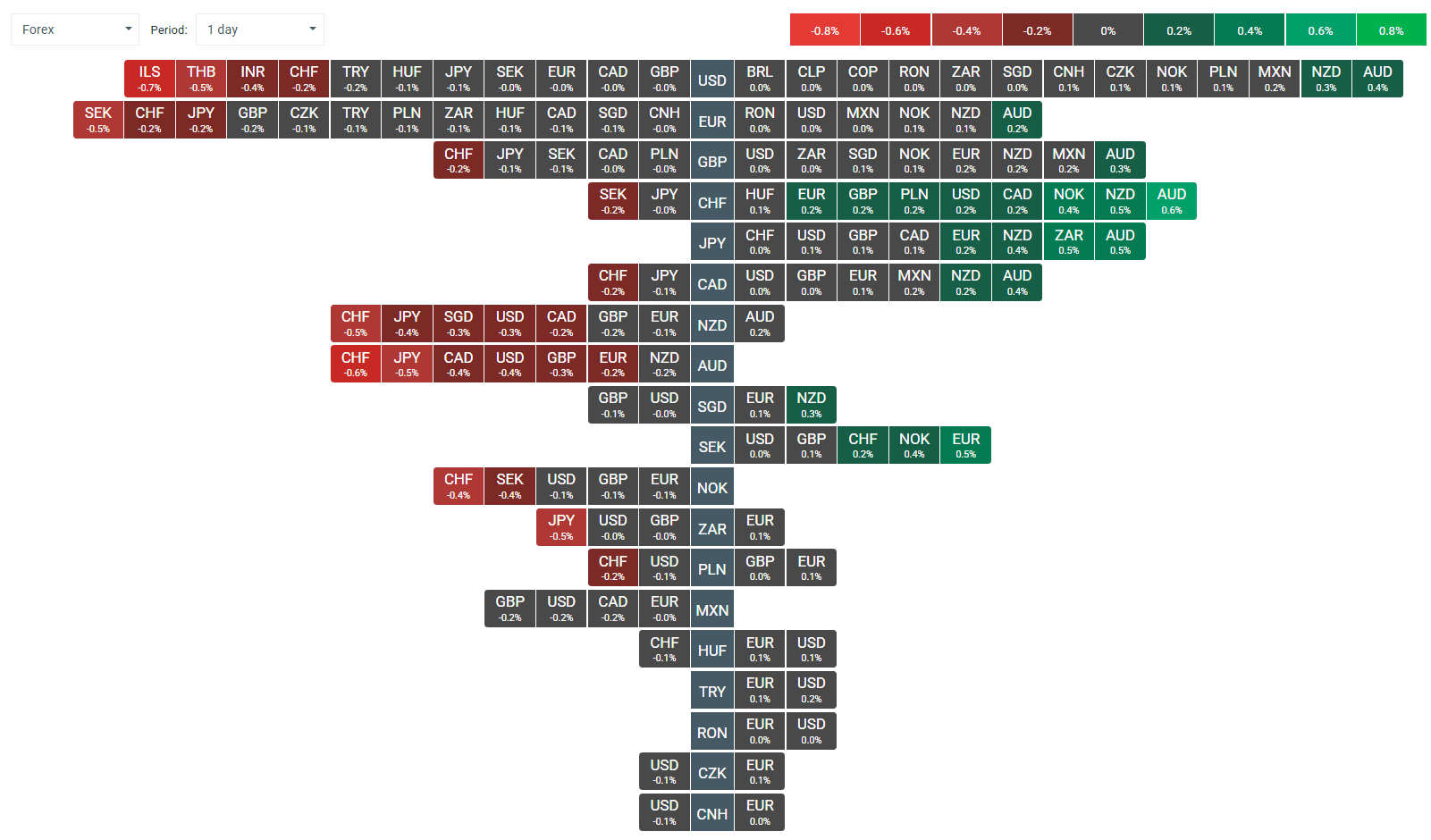

💱 Currencies

-

The dollar is strengthening on the back of demand for safe-haven assets and higher oil prices: DXY +0.3%, USD/JPY +0.3% (around 159.7). The yen remains weak despite hawkish signals from the BoJ, as higher energy prices pose a structural problem for the Japanese economy.

-

EUR/USD is down 0.3%, falling below the 1.1700 level. GBP/USD is down 0.4%, struggling to hold above 1.3400.

-

Currencies from the Southern Hemisphere under risk-off pressure: AUD/USD -0.3% (support at 0.7000), NZD/USD -0.2% (support at 0.5800). Zloty: USD/PLN -0.13% (3.6394), EUR/PLN +0.12% (4.2531) — relatively stable.

FX market volatility. Source: xStation

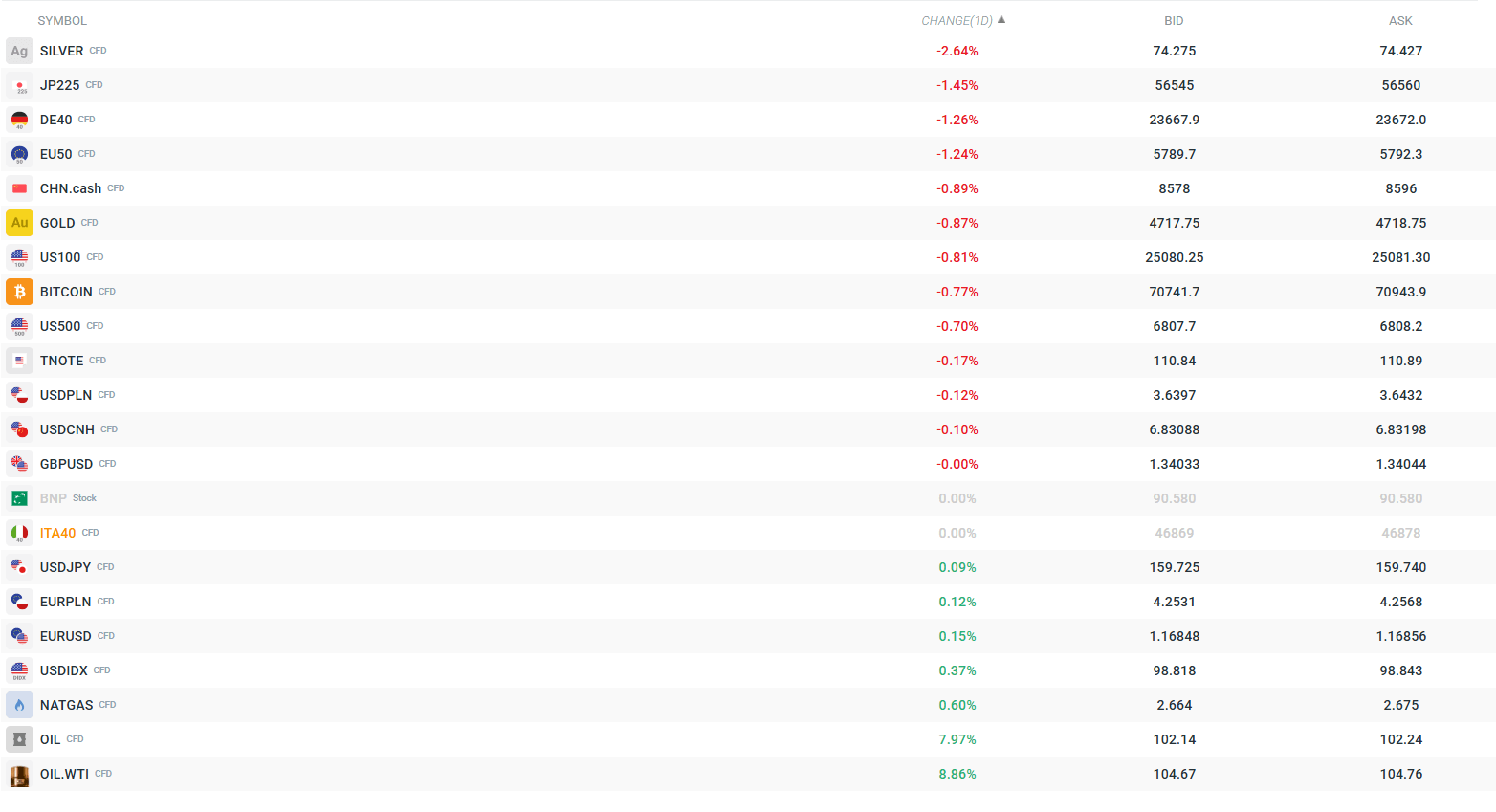

🛢️ Commodities

-

Crude oil is the clear leader today: WTI +8.95% (~$104.76/bbl), Brent +6.8% (above $102). This marks a return above the psychological $100 threshold following the breakdown of talks and the announcement of a blockade.

-

Analysts point to an additional risk factor: the expiration of the May WTI contract on April 21. The lack of a diplomatic breakthrough could trigger a sharp speculative rally—some predict a possible move toward $120 by the end of the week.

-

Gold is down between -0.5% and -0.81% (around $4,720/oz) due to a strong dollar and a rally in oil prices—but remains well above its low of $4,700. Silver is down 2.52%. Copper is down 1.3%, under pressure from weaker growth sentiment and the risk of a slowdown.

📊 Stocks and sectors

-

The prevailing scenario is a flight from cyclical sectors: banks, airlines, industrial companies, and retailers will come under pressure due to higher energy costs. Energy companies and the defense sector are the natural beneficiaries.

-

The DE40 is down 1.16%, the EU50 1.15%, the JP225 1.37%, and the CHN.cash 0.84% — a clearly negative picture globally.

₿ Cryptocurrencies

-

Bitcoin -0.69% (approx. $70,800) — is behaving like a risky asset, not like "digital gold," which is a weakness in the current environment.

Volatility in major markets. Source: xStation

🎯 What can we expect today?

-

The European session is likely to open sharply lower, with the key moment being 2:00 p.m. GMT — the official start of the blockade of Iranian ports. If a maritime incident occurs or Iran responds militarily, oil prices could spike higher, and stocks could extend their losses.

-

On the macroeconomic calendar, it’s worth keeping an eye on any diplomatic announcements (with Pakistan and China acting as mediators) and any statements from the ECB following the political upheaval in Hungary. Any signs of de-escalation from the U.S. or Iran would be the biggest positive surprise of the session. On the data front, the calendar is empty today.

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

Not so hawkish words, dovish dodges. EURUSD at 1.1450 during Kevin Warsh's Q&A

Fed Press Conference: Warsh Praises CapEx and Improves Market Sentiment

BREAKING: Fed Keeps Rates Unchanged Amid Regional Dissents and Warsh's Pause

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.