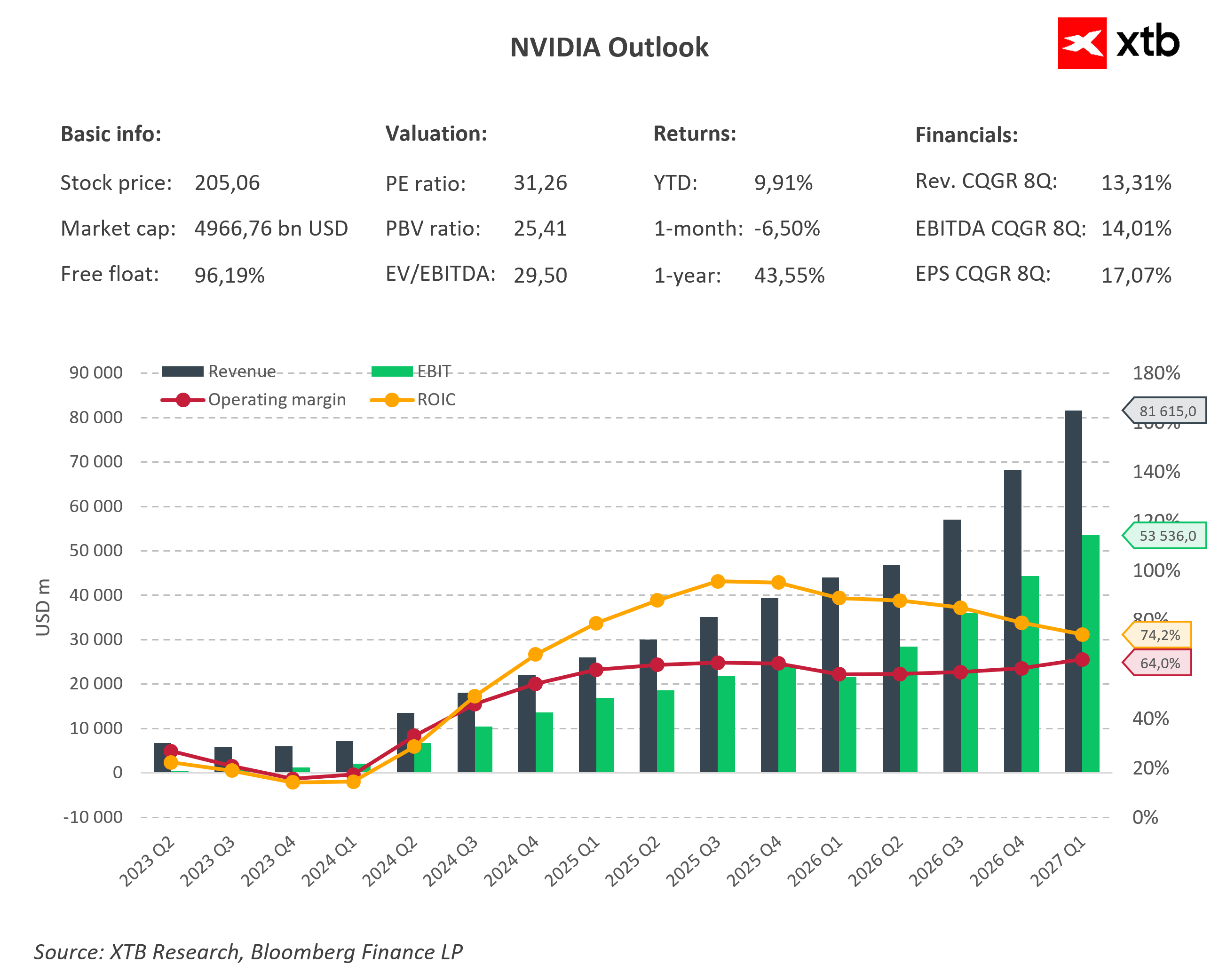

Nvidia’s decision to begin selling its Vera processors in China could prove to be one of the most important developments for investors following the AI sector in 2026. At first glance, this may appear to be little more than the launch of a new server processor. In reality, however, much more is at stake. For the first time since the tightening of U.S. export restrictions, Nvidia is attempting to regain its footing in China not by introducing another downgraded version of its AI accelerators, but by entering an entirely new market segment.

Over the past several quarters, China has become a growing source of uncertainty for Nvidia. Restrictions on exports of advanced AI chips have gradually limited the company’s access to one of the world’s most important technology markets. As a result, many investors have begun to question whether Nvidia can maintain its extraordinary growth trajectory without full access to Chinese customers. Vera may represent the company’s first meaningful answer to that challenge.

The new processor was designed for next-generation artificial intelligence systems, particularly so-called AI agents, autonomous systems capable of performing complex tasks with minimal human supervision. According to recent media reports, Nvidia has already begun discussions with Chinese customers and informed them that orders can now be placed, with initial deliveries potentially starting as early as August. For the market, however, the key question is not when the first shipments will arrive, but who will be buying the first Vera-powered systems.

If these processors find their way into the hands of China’s largest cloud providers, AI developers, and data center operators building infrastructure for the next wave of AI-driven services, it would send a powerful signal that Nvidia remains the industry standard even in markets where it can no longer offer its most advanced GPUs. From an investor’s perspective, maintaining relationships with major customers is often more valuable than a short-term increase in sales.

In the near term, the news is primarily important for sentiment surrounding Nvidia’s stock. Investors are being reminded that the company continues to actively pursue new growth opportunities and is not willing to passively accept the loss of a significant portion of the Chinese market. Expectations for the first wave of orders remain relatively modest, but even limited deployments could carry symbolic importance. They demonstrate that Nvidia has identified a product capable of preserving its presence in China despite current export restrictions.

The long-term implications are even more compelling. Vera is not simply another addition to Nvidia’s product portfolio. It is part of a much broader strategy aimed at transforming the company from a dominant GPU manufacturer into a provider of complete AI infrastructure. Just a few years ago, Nvidia’s success depended largely on sales of graphics processors and AI accelerators. Today, the company is building an ecosystem that includes CPUs, GPUs, networking technologies, HBM memory, the CUDA software platform, and fully integrated server systems ready for deployment by enterprise customers.

This may ultimately be the most important aspect of the story for investors. The more of a customer’s infrastructure that relies on Nvidia technology, the harder it becomes for competitors to displace the company. In practice, this creates opportunities to increase revenue per customer while strengthening long-term competitive advantages. If the strategy succeeds, investors may begin valuing Nvidia not merely as the leader in GPUs, but as the dominant supplier of computational infrastructure for the AI era.

Competition with Intel and AMD is another important element of this story. Until now, the primary battleground has been the AI accelerator market, where Nvidia enjoys a significant lead. Vera, however, marks an entry into territory traditionally controlled by server CPU manufacturers. If the new architecture gains traction among customers, competition among the industry’s largest semiconductor companies will expand into another multi-billion-dollar market.

That said, success is far from guaranteed. The most obvious risk remains geopolitics. While CPUs are currently not subject to the same strict export controls as advanced AI accelerators, the regulatory landscape can change quickly. If U.S. authorities determine that Nvidia’s new processors contribute to the development of advanced AI systems in China, additional restrictions on this segment cannot be ruled out.

A second major risk is China’s growing technological self-sufficiency. Beijing has spent years investing heavily in its domestic semiconductor industry, and local manufacturers continue to narrow the gap with their Western counterparts. Companies such as Huawei are developing their own solutions for data centers and artificial intelligence, meaning that some Chinese customers may view Nvidia’s products as temporary solutions until domestic alternatives become sufficiently competitive.

Investors should also keep in mind the risks associated with demand for AI infrastructure itself. The market is currently experiencing an unprecedented investment cycle, with major technology companies committing tens of billions of dollars to expanding data center capacity. However, there is no guarantee that this pace of spending will continue indefinitely. If the monetization of artificial intelligence progresses more slowly than expected, some customers may reduce capital expenditures, which would inevitably affect demand for Nvidia’s future products as well.

The broader significance of Vera extends well beyond the launch of another processor. Once again, Nvidia is demonstrating its ability to adapt to a rapidly evolving regulatory and geopolitical environment. Rather than focusing solely on restrictions affecting GPU exports, the company is searching for new avenues of growth and new ways to maintain relationships with its most important customers.

For that reason, the importance of Vera reaches far beyond the potential revenue generated by initial orders. For investors, it represents a test of whether Nvidia can leverage its dominant position in AI to build another multi-billion-dollar business while maintaining a foothold in a market that only recently appeared nearly inaccessible. If the strategy succeeds, it could mark the beginning of a new chapter in the company’s growth story and provide further evidence that Nvidia is becoming far more than just an AI chipmaker.

Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.