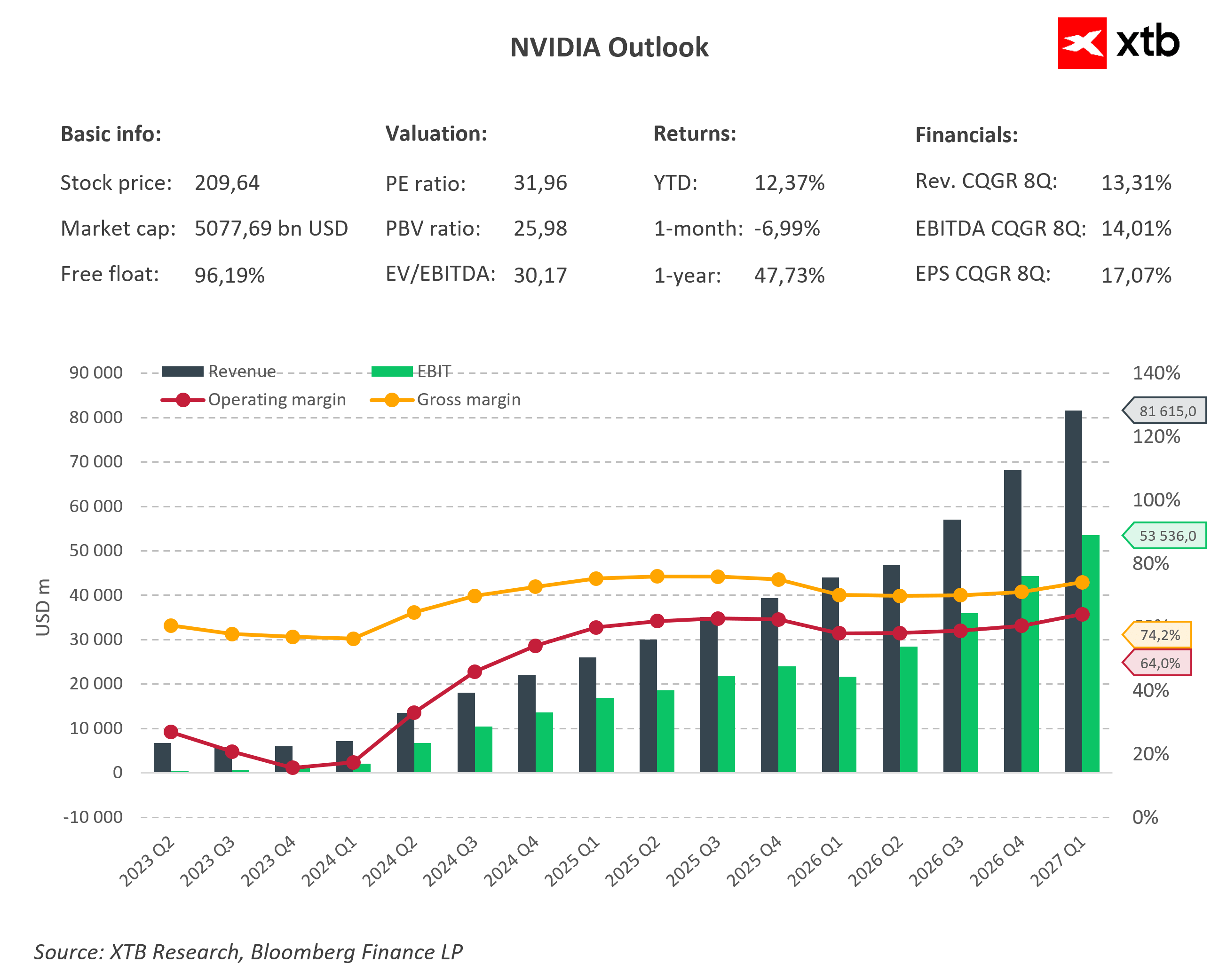

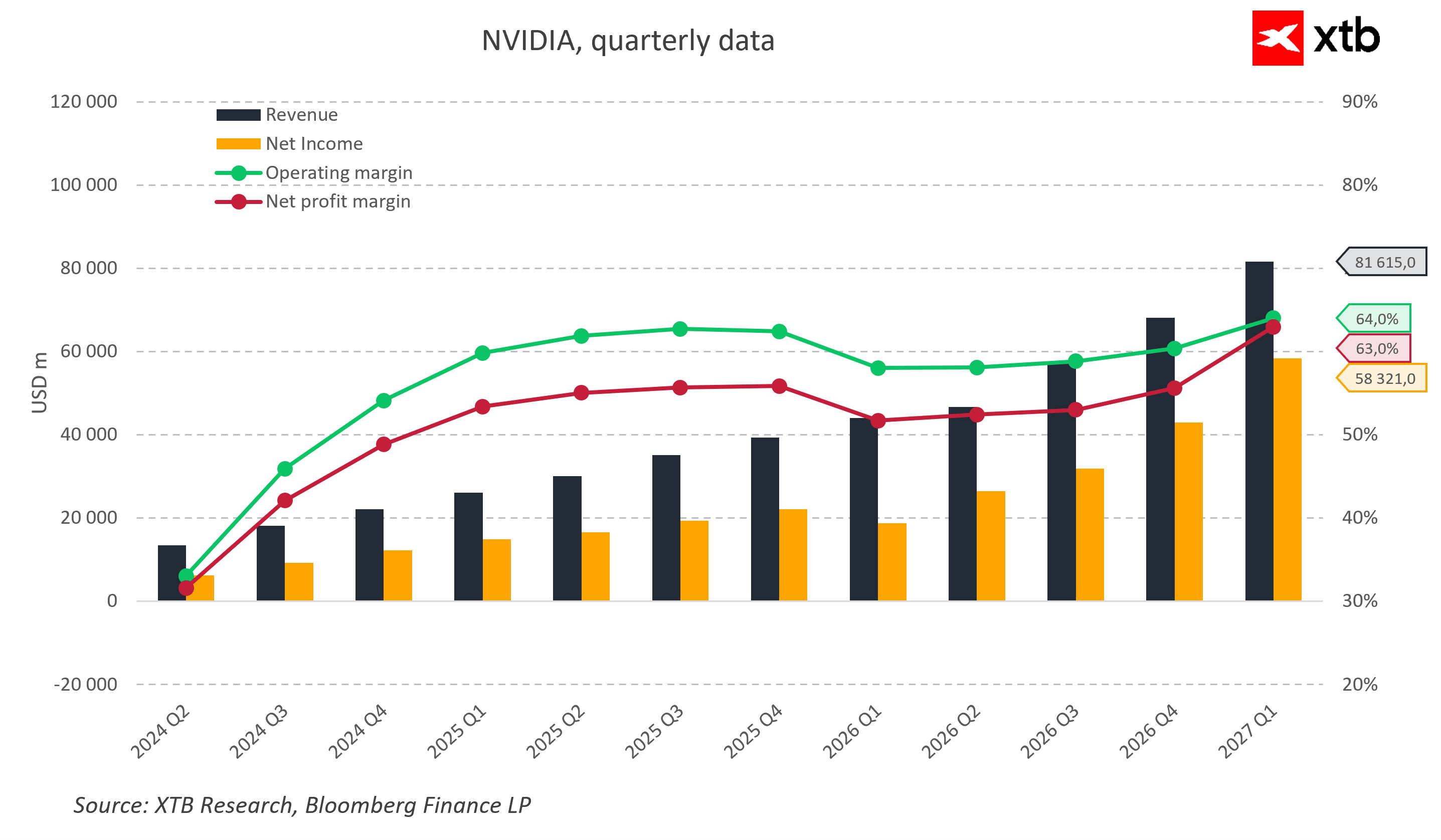

As we noted in our recent piece from the end of last week, NVIDIA has been increasingly building an alternative path to maintaining exposure to the Chinese market after export restrictions effectively cut off access to its most advanced GPU systems. At the time, we highlighted that instead of a conventional “return to China” via its existing products, the company could attempt a side-channel entry, leveraging segments that are subject to fewer regulatory constraints while still playing a critical role in AI infrastructure development.

That scenario is now taking a more concrete shape as NVIDIA deepens its engagement around its Vera CPUs, which the company is actively pitching to selected Chinese clients. According to the latest market reports, NVIDIA has already begun taking orders, with initial deliveries potentially starting as early as August. Importantly, this is not limited to early-stage discussions, as there are also reports of initial pilot deployments, including server configurations used to evaluate performance in data center environments.

The Vera architecture represents a notable shift away from NVIDIA’s most recognizable product lineup. It is a CPU based on the ARM architecture, designed for the next generation of workloads associated with so-called agentic AI, meaning systems capable of executing more complex, multi-step tasks in a partially autonomous manner. In practice, this marks NVIDIA’s entry into a segment traditionally dominated by Intel and AMD, while also operating in a space that is subject to significantly less stringent export restrictions compared to advanced GPU accelerators.

According to available analysis and market information, Vera is expected to deliver a meaningful performance uplift in selected AI-related workloads compared to competing solutions in specific compute scenarios. This is becoming a key selling point in discussions with Chinese data center operators, who remain under pressure to develop domestic technologies while still seeking the most efficient and scalable infrastructure solutions available globally.

At the same time, part of the early deployment strategy is expected to take place outside China, allowing NVIDIA to reduce regulatory risk and gradually integrate the platform into its broader customer ecosystem. Only in later stages could a more direct rollout into the Chinese market follow, depending on the evolution of US–China trade relations and the interpretation of existing export controls.

From a market perspective, this development can be seen as a natural continuation of the earlier trend in which NVIDIA is not so much regaining access to China through its traditional GPU business, but rather redefining how it participates in the market altogether. Instead of confronting the most restrictive regulatory barriers directly, the company is shifting its focus toward CPUs and server infrastructure, building a more flexible and indirect expansion channel.

However, this strategy is not without challenges. The key headwind remains the growing strength of domestic Chinese competitors and the accelerating development of local hardware alternatives, which could limit adoption over the longer term. As a result, the initial phase of Vera deployments is likely to remain selective and experimental, and whether this initiative ultimately opens a new growth chapter will depend on its ability to maintain a technological edge in an increasingly complex and geopolitically sensitive environment.

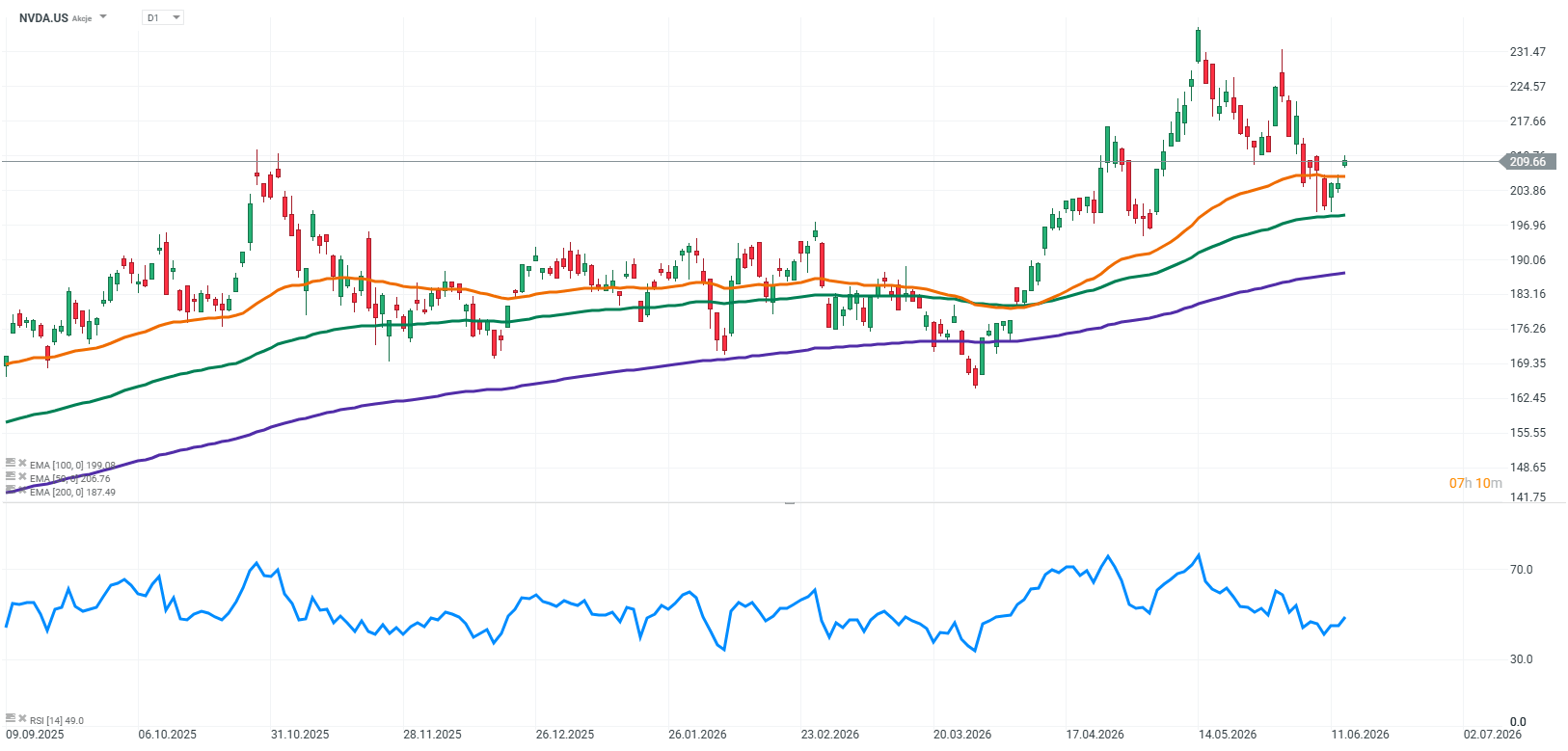

Źródło: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.