- RBNZ unexpectedly cuts the OCR by 50 basis points to 2.50%

- Significant demand gap after a larger-than-expected GDP decline in Q2 2025

- Monetary Policy Committee remains open to further cuts if needed

- RBNZ unexpectedly cuts the OCR by 50 basis points to 2.50%

- Significant demand gap after a larger-than-expected GDP decline in Q2 2025

- Monetary Policy Committee remains open to further cuts if needed

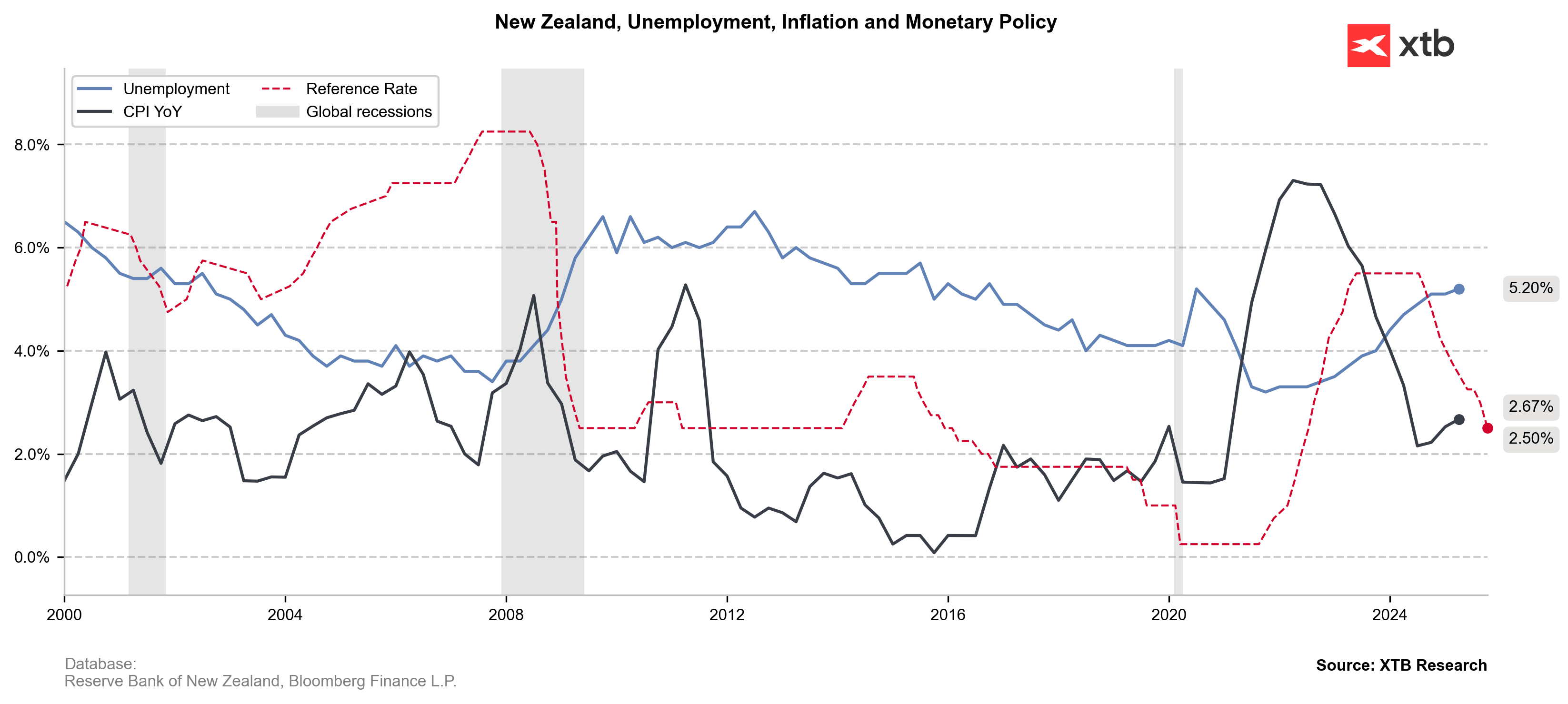

The Reserve Bank of New Zealand (RBNZ) delivered a larger-than-expected 50 bp rate cut, bringing the Official Cash Rate (OCR) down to 2.50% in response to weaker economic growth and a widening demand gap. The Committee noted that domestic inflationary pressures are easing. Core inflation excluding administered prices is consistent with the target, even though headline CPI remains near the upper end of the 1–3% band. Moreover, CPI inflation likely stood around 3.0% in Q3 2025, driven by higher food and regulated service prices. With clear excess capacity in the economy and a stronger policy transmission (lower wholesale, mortgage, and corporate lending rates), the Bank expects inflation to move toward 2% in the first half of 2026.

Unemployment remains worryingly high and, according to the RBNZ Board, poses a greater risk than CPI inflation staying near the upper bound of the Bank’s tolerance range.

RBNZ stance

Ultimately, a majority of members concluded that a 50 bp cut was justified to counter a prolonged demand gap and support economic activity. The Bank left the door open for further monetary easing if conditions warrant.

Macroeconomic situation according to the RBNZ

Macro indicators remain mixed but lean to the weaker side. GDP in Q2 2025 contracted -0.9% QoQ versus expectations for a -0.3% decline (partly due to seasonal factors). Supply constraints — including energy shortages, weather impacts on agriculture, and industrial bottlenecks — have curbed production. Domestically, housing prices are stable, while residential and business investment remain weak, although lower interest rates are beginning to support household spending and should gradually reduce debt-servicing costs.

Market reaction

Markets immediately priced in a more dovish outlook. The New Zealand dollar is the weakest G10 currency today, falling between 0.6% and 1.0%. NZDUSD dropped to a 6-month low, down 1.00% to 0.5740 USD. Swaps now fully price another 25 bp cut in November (to 2.25%) and assign a significant probability to a 2.00% terminal rate.

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.