Brent crude (OIL) is down nearly 3% today, trading around $93 per barrel and extending a clearly bearish short-term trend in which supply-side pressure continues to dominate despite ongoing uncertainty surrounding the Strait of Hormuz. At the same time, some research desks, including Piper Sandler, are increasingly positioning themselves in the “prolonged crisis” camp rather than expecting a rapid de-escalation around Hormuz. According to the bank, the market may be interpreting signals of a potential Iran deal too optimistically, while the actual shipping situation in the region remains highly fragile.

Piper Sandler bets on higher oil prices

In its latest note, Piper Sandler argues that the Strait of Hormuz could remain effectively partially closed for several more months. That would imply continued disruption to crude oil and LNG flows from the Middle East to Asia, increasing pressure on the physical oil market.

- The key issue is not necessarily a formal “closure” of Hormuz, but the dramatic decline in commercial tanker traffic. According to Piper Sandler, the chances of shipping volumes recovering even to 50% of pre-crisis levels appear low — not only over the next few weeks, but potentially over the coming months as well.

- Markets have received mixed signals in recent days. On one hand, Donald Trump has suggested that an agreement with Iran is largely negotiated. On the other hand, the Pentagon confirmed additional strikes on Iranian military installations and vessels deploying mines near the Strait. These developments suggest that military tensions are still escalating rather than fading.

- Piper Sandler believes Washington is reluctant to pursue a full-scale confrontation, as a broader Iranian retaliation could destabilize the region and further disrupt global supply chains. At the same time, Tehran appears convinced it still holds significant negotiating leverage, reducing the probability of a quick compromise.

- All of this leads the bank to a fairly aggressive conclusion: oil prices could still reach new yearly highs later this summer.

That view is difficult to dismiss. Until recently, roughly one-fifth of global seaborne oil trade passed through the Strait of Hormuz. If tanker traffic remains constrained for an extended period, the issue shifts from futures market volatility to the physical availability of crude - particularly for Asia.

U.S. strategic reserves are heading east

The United States is now sending a rare cargo of crude oil from its Strategic Petroleum Reserve to Asia, highlighting how deeply the Hormuz crisis is reshaping global energy flows. According to shipping data cited by Reuters, a tanker carrying oil from the U.S. SPR has departed the Gulf of Mexico bound for the Philippines. This marks the first shipment of U.S. strategic crude to Asia since late 2022.

- The move is unusual, but strategically logical. The disruption of normal tanker traffic through Hormuz has severely impacted traditional supply routes from the Middle East to Asia. Before the crisis, Asian economies imported around 80% of their crude from the Middle East, while the Philippines relied heavily on Saudi Arabia, Iraq and the UAE.

- For example, the Greek VLCC Arosa is currently transporting around 616,000 barrels of U.S. sour crude from the SPR alongside another 700,000 barrels of a separate U.S. sour blend. This shows that Washington is not only redirecting crude toward Europe, but is increasingly attempting to offset shortages in Asia as well.

- The problem is that the scale of potential Middle Eastern supply disruption remains enormous. Estimates suggest that between 14 and 15 million barrels per day of production could be affected by ongoing tensions. Even a broad coordinated release from IEA member states may prove insufficient if the Hormuz crisis drags on.

Despite the recent pullback in oil prices, the global crude market is entering a phase of forced reorganization. Asia - the region most dependent on Middle Eastern energy supplies is likely to bear the highest logistical and pricing costs. Meanwhile, the United States is increasingly acting as an emergency supplier not only for Europe, but also for Asian buyers.

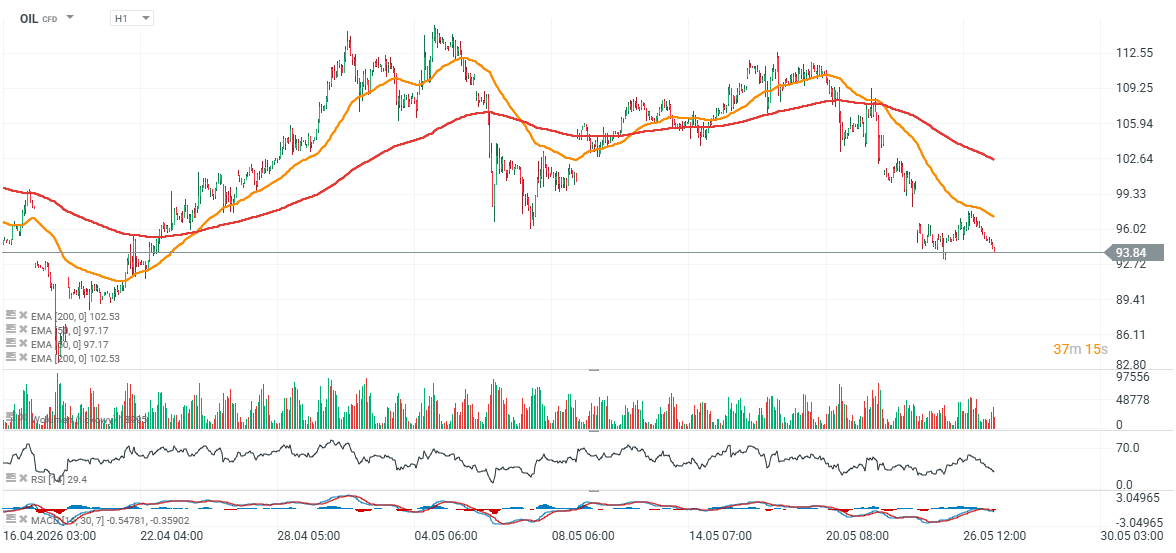

OIL (D1 chart)

WTI crude initially surged toward $120 per barrel before retreating below the $100 level. However, according to Piper Sandler, the market may be pricing in normalization too early. If the crisis persists, renewed supply pressure could once again push oil prices sharply higher, potentially weighing on both global economic growth and the recent rebound in equity markets.

Source: xStation5

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.