Thursday’s session is bringing further gains in oil prices on the back of concerns not only about the prospects for peace between the US and Iran, but also about the durability of the ceasefire. The latest wave of reports raises more reasons for concern than it provides answers.

Iran reportedly categorically rejected demands to hand over fissile materials and is maintaining its position calling for recognition of its control over the strait (as well as the right to collect fees).

IEA head Fatih Birol warned that in July or August the market could enter a “red zone” if the situation in the Middle East does not improve. The problem is the collision of a seasonal peak in fuel demand with constrained exports from the region and falling inventories.

OPEC+ is trying to ease tensions. The group is set to raise its July production target by about 188 thousand barrels per day. Under normal circumstances this would be a stabilizing signal; however, given the current situation, it is a symbolic gesture rather than real downward pressure on prices.

The situation is not helped by reports from Russia, where - aside from further questions about the regime’s intentions in light of setbacks at the front - another wave of attacks on infrastructure can be observed. This time, Ukrainian drones hit facilities along the Volga, including the refinery in Syzran.

Expectations of rising oil prices are no longer confined to the general public. UBS raised its September Brent price forecast to $105 and WTI to $97. The bank notes that short-term risks are skewed to the upside. In an extreme scenario, Brent could, according to UBS, exceed $150 per barrel.

Importantly, US oil companies are not currently signaling an aggressive increase in production, even despite rising supply tightness and an elevated geopolitical premium in oil prices. Companies’ priorities are cash flow, dividends, share buybacks, and maintaining profitability - not maximizing output volumes. If logistical or geopolitical disruptions command a premium in crude prices, the coming quarters could bring a meaningful increase in profitability for the oil sector.

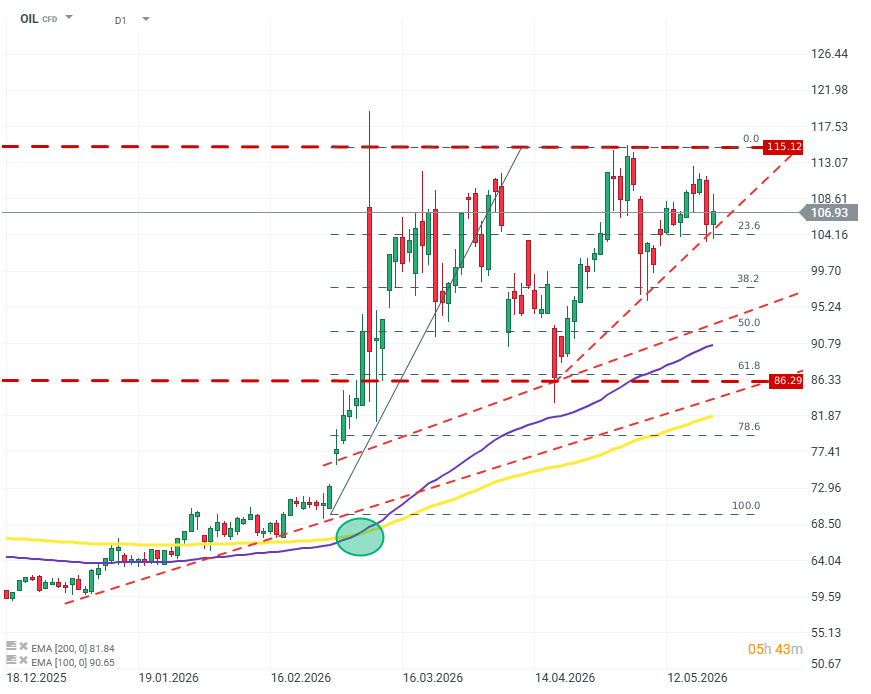

OIL

On the oil price chart, one can observe a shift toward increasingly steep uptrends despite local pullbacks. Source: xStation5.

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Oil rises over 3% 🛢️

Defense sector ahead of earnings: Summary

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.