The oil market is changing direction rapidly. Until recently, investors were worried about supply disruptions through the Strait of Hormuz and a potential supply shock. Today, that narrative is slowly reversing. Morgan Stanley has cut its oil price forecasts for the second time in around two weeks, arguing that flows through Hormuz are returning to normal faster than expected, while the market also faces strong U.S. production and weak demand from China. What does the bank see?

-

Morgan Stanley lowered its Brent crude forecast to an average of 75 USD per barrel for both Q3 and Q4 2026. This means previous forecasts were reduced by 15 USD and 5 USD per barrel, respectively.

-

The bank also cut its forecasts for all four quarters of 2027 and now expects Dated Brent to trade at around 70 USD per barrel by the end of 2027.

-

According to Morgan Stanley analysts, the main reason behind the revision is the faster-than-expected recovery in oil transport through the Strait of Hormuz following progress in talks between the U.S. and Iran.

-

At the same time, more oil is coming from the U.S., while demand from China remains disappointingly weak. This combination of rising supply and weaker consumption increases the risk of a global oil surplus.

-

Brent crude futures have fallen by around 30% this quarter, showing how quickly the market has moved from pricing geopolitical risk to worrying about excess supply.

-

The Strait of Hormuz remains one of the most important transport routes for the global oil market. Any improvement in the region reduces the geopolitical premium that had previously supported prices.

-

Morgan Stanley is not the only investment bank changing its view. Goldman Sachs has also lowered its oil market forecasts, suggesting that major financial institutions are becoming more cautious on the price outlook.

-

For investors, this marks a clear shift in narrative. The market is no longer focused only on conflict risk in the Middle East and is paying more attention to fundamentals — the balance between global supply and demand.

-

If production remains high and demand, especially from China, fails to accelerate, pressure on oil prices could continue in the coming quarters.

Morgan Stanley believes the biggest risk for the market is no longer a shortage of oil, but the possibility of a surplus. Such a scenario could keep Brent prices under pressure even if geopolitical tensions in the Middle East remain elevated.

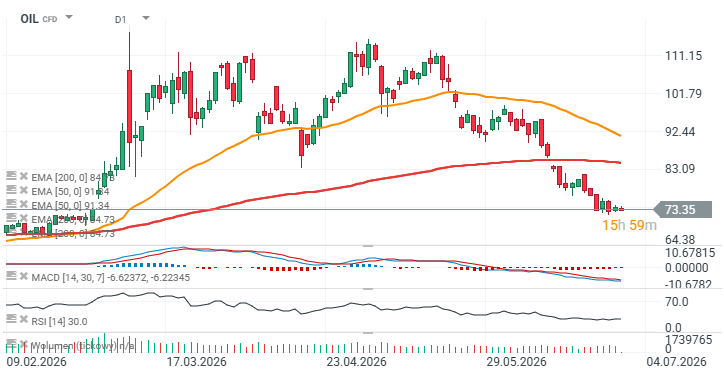

Brent crude futures chart (OIL), D1 interval

Oil has suffered a major decline and is now stabilizing in the 72–74 USD range — levels not seen since late February 2026. The RSI is close to the upper boundary of oversold territory, at around 30. The next important support level is the round 70 USD per barrel area, additionally supported by previous price reactions from February.

Source: xStation

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.