- Specter of USA-Iran agreement and opening of the Strait of Hormuz: Anticipation of Friday's pact signing pushes oil prices down (Brent 78–79 USD, WTI near 75 USD), discounting the immediate unblocking of Iranian exports and the release of over 100 tankers detained in the gulf.

- IEA and Goldman Sachs herald oversupply: The IEA drastically lowered its forecast for this year's demand (a drop of 1.1 million bpd) and warns of a massive flooding of the market in the coming years, which prompted Goldman Sachs to lower its Brent price forecast to 85 USD for this year and 75 USD for the next.

- Bearish market and technical signals: The Middle Eastern market's transition to a contango structure officially confirms a physical oversupply of the raw material, and the testing by Brent prices of the key 200-session moving average technically seals the sellers' advantage.

- Specter of USA-Iran agreement and opening of the Strait of Hormuz: Anticipation of Friday's pact signing pushes oil prices down (Brent 78–79 USD, WTI near 75 USD), discounting the immediate unblocking of Iranian exports and the release of over 100 tankers detained in the gulf.

- IEA and Goldman Sachs herald oversupply: The IEA drastically lowered its forecast for this year's demand (a drop of 1.1 million bpd) and warns of a massive flooding of the market in the coming years, which prompted Goldman Sachs to lower its Brent price forecast to 85 USD for this year and 75 USD for the next.

- Bearish market and technical signals: The Middle Eastern market's transition to a contango structure officially confirms a physical oversupply of the raw material, and the testing by Brent prices of the key 200-session moving average technically seals the sellers' advantage.

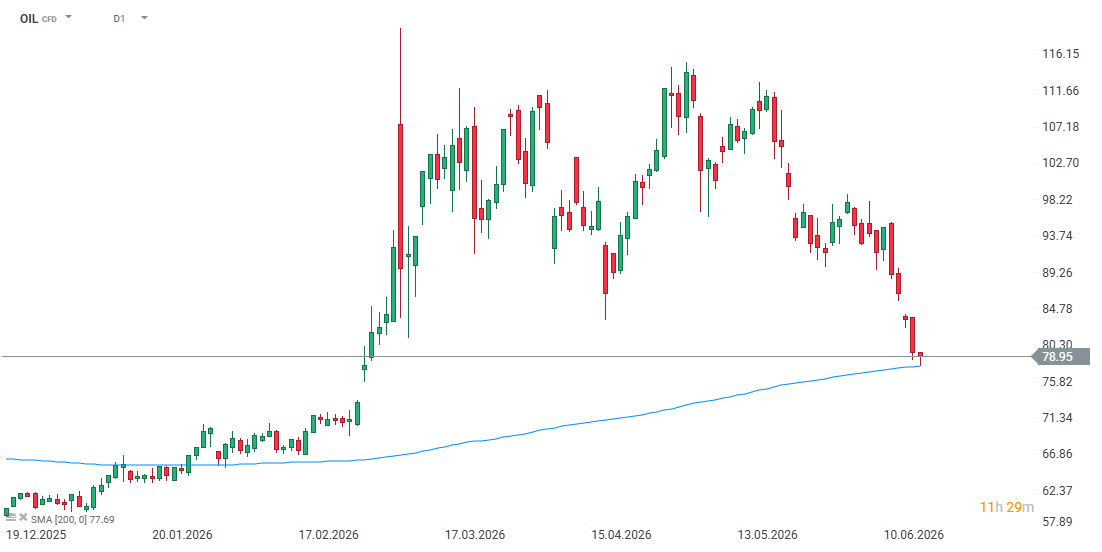

Oil prices continued further declines in the morning, but at this moment they are consolidating and rising to around $79 per barrel of Brent oil. Although the market is set for further declines in the face of potential peace between Iran and the US, it is worth emphasizing that many issues still remain unresolved and unsaid.

It is worth noting that the details of the 14-point memorandum are still being refined and to a large extent this plan is a wish list, however, the market is already dynamically discounting the prospect of a wide stream of raw material returning to the market, which translated into a drop in prices by nearly 40% from the peak of the conflict. Brent oil contracts fluctuate in the range of $78–$79 per barrel, while American WTI oil temporarily fell below the psychological barrier of $75, before stabilizing around $75–$76.

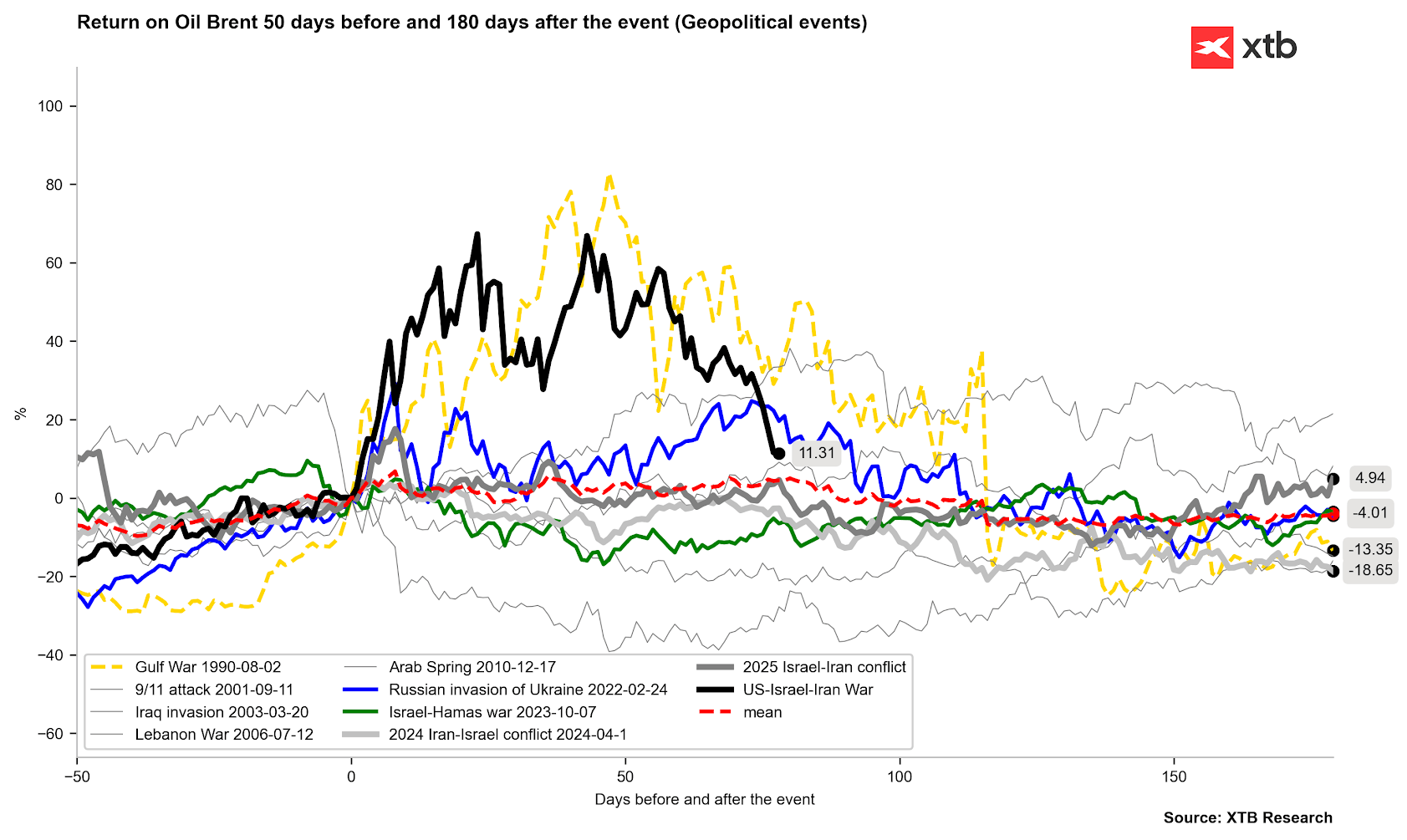

The oil price is about 11% above pre-conflict levels.

The oil price is about 11% above pre-conflict levels.

Source: Bloomberg Finance LP, XTB

What affects oil prices?

- Consent for immediate export: Although the official content of the agreement has not been published, incoming reports show that Iran will be able to immediately sell oil and fuels right after signing. Furthermore, the US has committed to lifting the blockades of its ports and issuing sanctions waivers covering oil exports, the petrochemical sector, and related banking and insurance services.

- Tanker activity: Shipowners are already preparing for the opening of the Strait of Hormuz by relocating their empty ships towards the Middle East. Analysts take as a base scenario that traffic through this key logistical point will be fully restored in both directions.

- Effect of releasing stocks: It is estimated that opening the strait will allow over 100 loaded ships belonging to other countries in the region, which were blocked there due to the conflict, to leave the Persian Gulf. Such a sudden influx of oil will act on the market like a powerful release of reserves. Nevertheless, a full return of exports to pre-war levels will take at least several months, among other things due to the need to clear water routes of mines.

- Return of production to normalcy: Production in the region could have fallen by as much as 14 million barrels per day. Flexibility in production occurs primarily on the part of Saudi Arabia and the United Arab Emirates. In the 90s, production returned to normalcy only after about 12 months, but in the main countries of the conflict, i.e., in Iraq and Kuwait, the return took much longer.

International Energy Agency (IEA) Forecasts

In its latest report, the IEA again presents a more bearish (pro-supply, and downward for prices) view of the market:

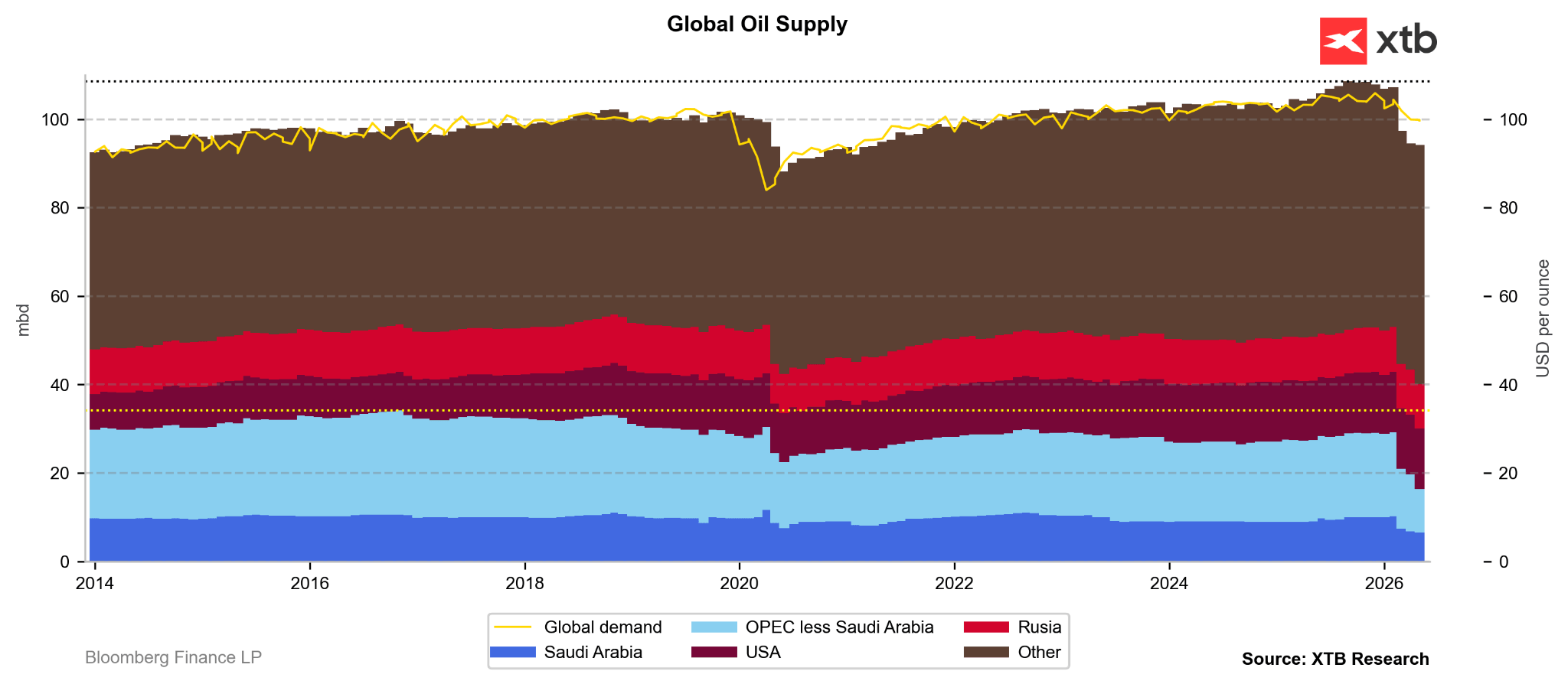

- Deep blow to demand: The Agency has significantly revised its estimates regarding this year's demand. It is estimated that global oil consumption will shrink this year by as much as 1.1 million barrels per day (bpd) due to high prices at stations and problems with the availability of refined products (previously a drop of 420 thousand bpd was expected). Already globally, demand has decreased according to preliminary estimates to levels of 100 million barrels per day.

- Perspective of a huge oversupply in 2027: The IEA's first detailed forecasts for 2027 point to an approaching massive supply overhang. It is expected that global supply will increase by an impressive 8 million bpd, while demand will increase by only 2 million bpd. Although these are quite strong statements, even if they come true in half, the oil market should find itself under pressure.

- State of global reserves: Currently, global stocks are shrinking at a record pace. However, the expected surplus at the end of the year is intended to give the market much-needed respite and an opportunity to rebuild these depleted stocks.

Demand fell to 100 million barrels per day and will most likely not experience a dynamic recovery in the near future.

Demand fell to 100 million barrels per day and will most likely not experience a dynamic recovery in the near future.

Source: Bloomberg Finance LP, XTB

Banks cut price forecasts: Goldman Sachs expects stabilization

Financial institutions immediately react to the change in the geopolitical paradigm. Goldman Sachs decided on a clear downward revision of its price expectations:

- Forecast for 2026: The bank lowered its average Brent oil price forecast for this year to 85 USD per barrel (compared to the earlier 90 USD) and WTI to 80 USD per barrel (compared to 85 USD). It is worth noting that current prices are lower than the average forecast.

- Forecast for 2027: In the horizon of the next year, Goldman Sachs experts see the average Brent price at the level of 75 USD, and WTI at the level of 70 USD per barrel. The level of 75 USD per barrel is currently priced in the contract curve for May 2027.

- Faster normalization: This correction results from the assumption that thanks to the opening of the Strait of Hormuz, exports from the Persian Gulf will return to the pre-conflict norm already by the end of July (previously it was estimated that this would happen only at the end of August).

- Persistent risk: However, the bank stipulates that Friday's agreement is preliminary. If further, detailed talks regarding the Iranian nuclear program end in failure, Tehran may again decide to block the strait.

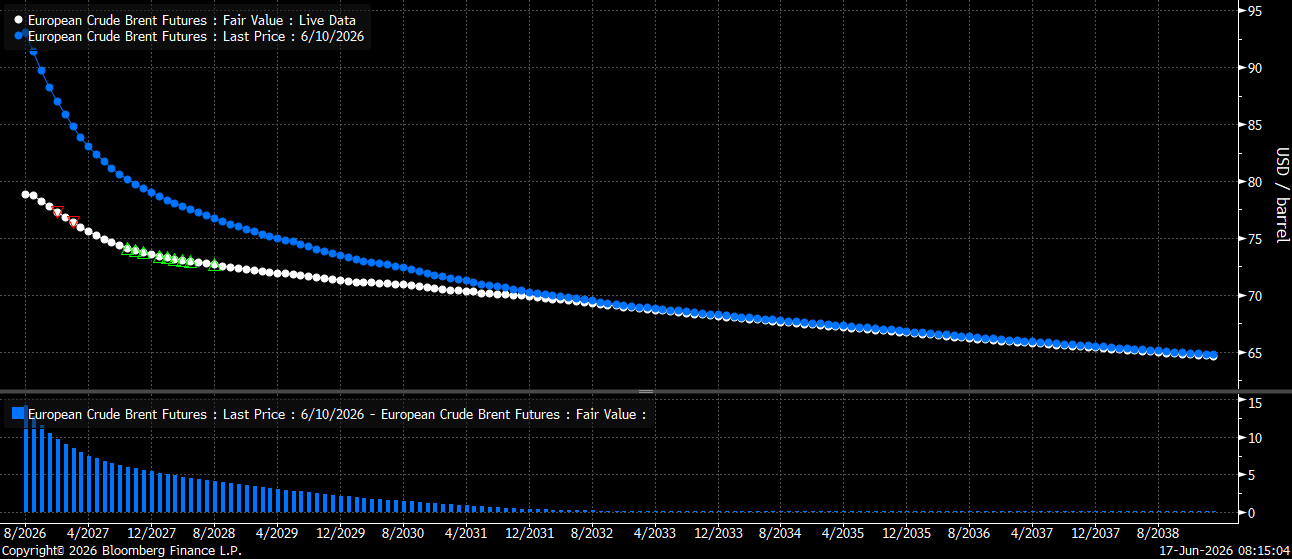

The forward curve has clearly fallen in the short and medium term and the 75 USD level is already marked for May 2027. On the other hand, the 70 USD level is priced in 2031. The forward curve is at this moment very flat compared to the past.

The forward curve has clearly fallen in the short and medium term and the 75 USD level is already marked for May 2027. On the other hand, the 70 USD level is priced in 2031. The forward curve is at this moment very flat compared to the past.

Source: Bloomberg Finance LP

Market indicators and technical analysis

Investors are clearly living in the future and the potential for a large oversupply next year and are forgetting about the possible physical pressure on the market. On the other hand, we observe a very interesting situation in regional prices and from the perspective of technical analysis

- Contango Structure: In the key Middle Eastern market (Dubai), forward spreads moved into a bearish contango structure, which directly signals a physical oversupply of the raw material on the market. For a moment, we even observed an attempt by the nearest calendar spread on Brent oil to enter a minimal contango.

- Technical Signal: The sellers' pressure was reinforced by the fact that on Wednesday the price of Brent oil tested the 200-session moving average for the first time since February. Breaking this support is very important from the perspective of long-term trends, but at the same time may suggest short-term over-selling.

BREAKING: BoE Keeps Rates Unchanged

🛢️Further escalation and tense situation do not drive oil further

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

Not so hawkish words, dovish dodges. EURUSD at 1.1450 during Kevin Warsh's Q&A

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.