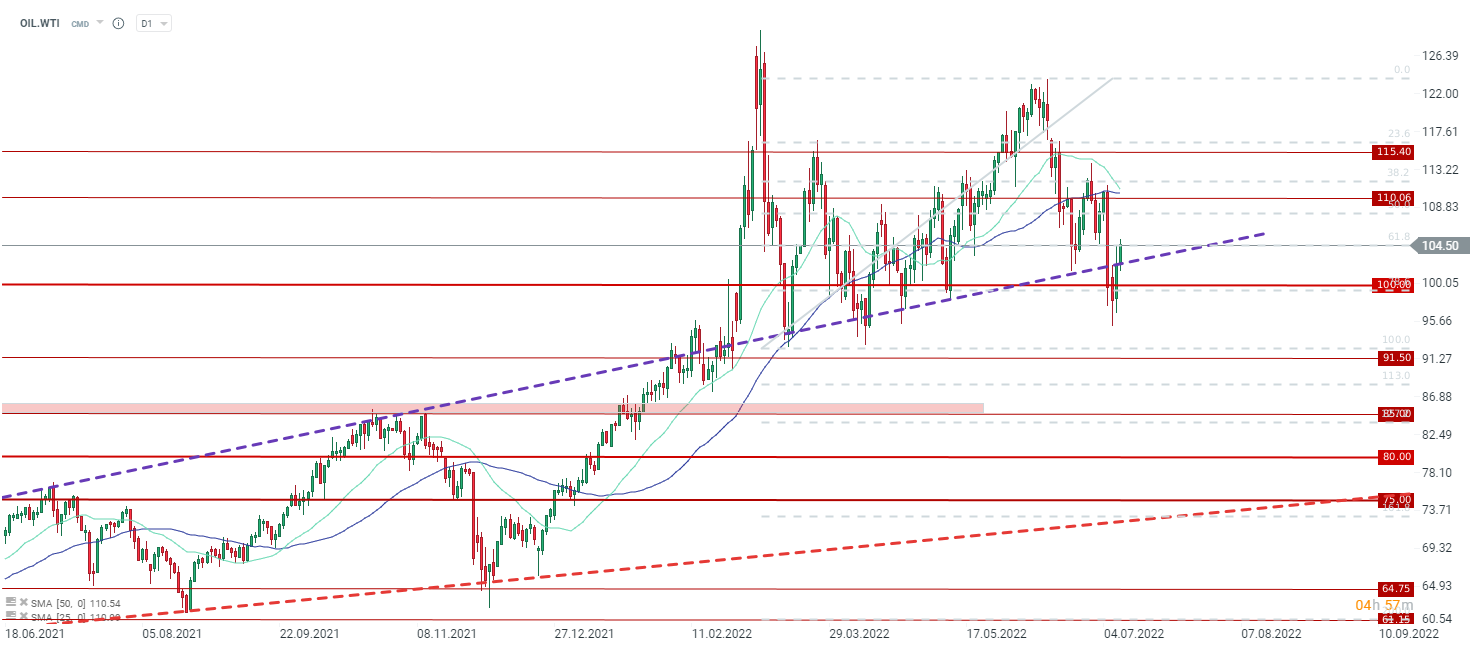

The massive declines in the oil market earlier in the week were the result of major recession fears around the world. Recessionary fears have emerged primarily in Europe in the face of a strike in Norway, which is leading to a cut of up to 50% of gas exports to European countries. Lack of access to gas from a major supply, a 60% drop in exports from Gazprom and the shutdown of exports next week due to maintenance repairs are pushing the price of the vital energy commodity very high again, but also increasing the chances of a recession if large supplies are not resumed. From all this, we had a massive sell-off in the euro and the pound and the strengthening of the US dollar, which led to an even bigger sell-off in the commodity market.

On the other hand, there are no serious signs of demand destruction yet. Yes, in the United States, the holiday plans of millions of Americans have been altered due to high fuel prices, and demand for marine fuel in the first half of the year was lower than a year earlier. However, in addition to this, overall global demand is growing all the time along with a very large supply constraint, primarily in terms of the fuel market. The physical market continues to see very strong demand, which is characterized by a large difference between the spot price and the next contract. The crack spread, or the difference between the price of the petroleum product and the price of crude, is still very large (despite a slight pullback), showing that the biggest problem is seen on the end product side. U.S. refineries are currently producing as much as they can, but after the summer, maintenance time will come, which could put upward pressure anew.

Citi points out that in the event of a recession, oil prices will fall into the area of $65 per barrel. This level seems remote, but we should not rule out such a situation either. As the covid situation showed, demand can very quickly collapse as much as 30% in the space of a few weeks, which led to more than 2 years of recovery from the pre-pandemic situation. On the other hand, the current fundamental situation does not justify levels below $100 per barrel, but rather the continuation of high levels.

At the end of the week, oil recouped more than half of the declines of the entire week, thanks to the last two sessions. On the other hand, the downward sequence in oil is maintained all the time.

Source: xStation5

The coffee market in the grip of weather and empty warehouses: The paradox of record Brazil harvests

Chart of the Day: Who suffers from the oil price drop? (28.07.2026)

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.