The biggest company in CEE region, polish oil giant Orlen (PKN.PL) entered 2026 with its strongest quarterly performance in three years, significantly outperforming market expectations. The group’s results were primarily driven by the sharp rise in oil prices following the escalation of the Middle East conflict and the blockade of the Strait of Hormuz, a key route for global crude oil transportation. As a result, the company not only improved profitability across its fuel and energy segments, but also demonstrated a very strong financial position despite an exceptionally volatile market environment. Importantly, Orlen is also reporting growth in non-fuel margins, which should be viewed positively by investors.

Key takeaways

-

Orlen posted PLN 8.15 billion in net profit in Q1 2026, up nearly 94% year-over-year and almost 25% above market expectations.

-

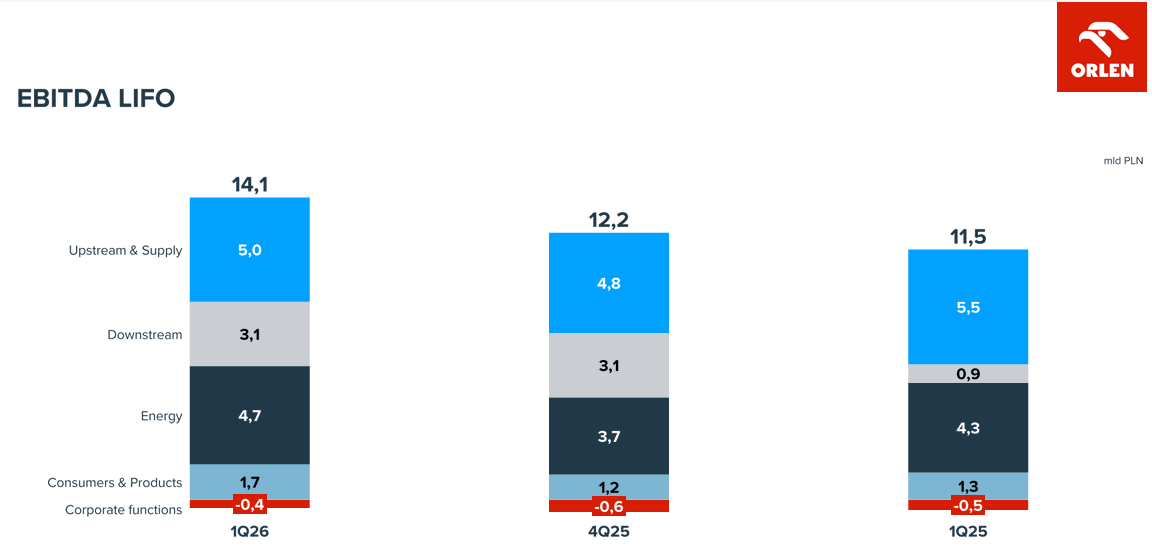

Adjusted LIFO EBITDA increased to PLN 14.1 billion, exceeding analyst forecasts by more than 5%.

-

Group revenues reached PLN 75.8 billion, with the company beating virtually all analyst consensus estimates.

-

Higher oil and fuel prices supported strong performances across refining, energy and retail sales segments.

-

Management recommended a record dividend worth PLN 9.3 billion while maintaining elevated investment spending.

-

Orlen shares are up nearly 37% year-to-date and 86% year-over-year, slightly below the company’s 94% YoY earnings growth.

The sharp improvement in profitability justifies the recent stock rally, and if oil prices remain close to USD 100 per barrel in the second half of the year, the company could be heading toward the strongest year in its history.

Source: Orlen

Geopolitics and higher oil prices fueled Orlen’s record quarter

The first quarter of 2026 highlighted how closely Orlen’s performance remains tied to global commodity markets. Rising geopolitical tensions in the Middle East and the blockade of the Strait of Hormuz triggered a sharp increase in oil prices, with average Brent crude prices reaching USD 81.1 per barrel compared to USD 75.7 a year earlier. By March, markets had already begun pricing in scenarios where oil could rise toward USD 100–120 per barrel.

For Orlen, this translated into a major profitability boost. The group delivered PLN 14.1 billion in adjusted LIFO EBITDA and PLN 8.15 billion in net profit, marking its best quarterly result since early 2023. What stands out even more is how strongly the company outperformed analyst expectations. Market consensus pointed to net profit of roughly PLN 6–6.5 billion, while the actual result came in almost 25% higher.

The strong macro backdrop also pushed fuel prices in Poland to record levels. Diesel temporarily approached PLN 8 per liter, while Pb95 gasoline moved close to PLN 7. The government responded with temporary price caps and tax reductions, while simultaneously starting work on a windfall tax targeting energy companies.

Orlen’s balance sheet strength also deserves attention. The company generated PLN 8.5 billion in operating cash flow while maintaining a near-zero net debt-to-EBITDA ratio. This created room both for a record dividend payout and continued investment spending exceeding PLN 5 billion during the quarter alone.

Business segments confirmed the strength of Orlen’s integrated model

The Q1 results once again confirmed that Orlen’s key competitive advantage remains its diversified business structure. The strongest contributor was the Upstream & Supply segment, which generated around PLN 5 billion in EBITDA, benefiting directly from elevated commodity prices. The Energy segment also delivered very strong results, reporting PLN 4.7 billion in EBITDA supported by higher electricity and heat production.

A significant improvement was also visible in the Consumers & Products segment, which includes retail fuel, gas and electricity sales. EBITDA in this division rose to PLN 1.7 billion from PLN 0.8 billion in the previous quarter. Fuel sales increased by 2% YoY, gas sales by 11%, and electricity sales by 14%.

Refining operations also remained exceptionally strong, with total crude throughput reaching 9.4 million tons. At the same time, petrochemicals continued to operate in a more challenging market environment, showing that not every business segment benefited equally from higher commodity prices.

One of the more interesting elements of the report was the change in refinery margin reporting methodology. Orlen replaced its previous model refining margin indicator with a new CEE refining margin metric, which according to the company better reflects actual market conditions following the outbreak of conflict in the Middle East. The updated methodology materially reduced previously reported historical margin levels, which may be interpreted as a more conservative and realistic presentation of refining profitability.

Orlen increases sales and investments despite market pressure

The latest data shows that the company’s performance improvement was driven by much more than simply higher oil prices. Orlen delivered growth supported by tangible increases in sales volumes across nearly all major business areas — from fuels and gas to fertilizers and electricity. This is particularly important because it suggests the company’s stronger results were not solely the effect of a temporary commodity price shock.

Margins on refining products improved especially strongly. Diesel prices increased by 25% YoY, jet fuel prices surged by 40%, while light heating oil prices rose by 21%. This created a highly supportive environment for the downstream segment, which benefited from both stronger pricing and higher sales volumes.

The structure of sales growth also deserves attention. Orlen increased LPG sales by 35% YoY, fertilizer sales by 17%, PVC sales by 38%, and PTA sales by 33%. This suggests that improving market conditions extended beyond the traditional fuel business and into petrochemicals and industrial segments, which had remained under pressure from weak European demand in previous quarters.

Another positive factor was the decline in operating costs. Total operating expenses fell by PLN 2.6 billion year-over-year, mainly due to lower costs of natural gas and crude oil purchases. As a result, the group improved profitability not only through higher product prices, but also through a more favorable cost structure.

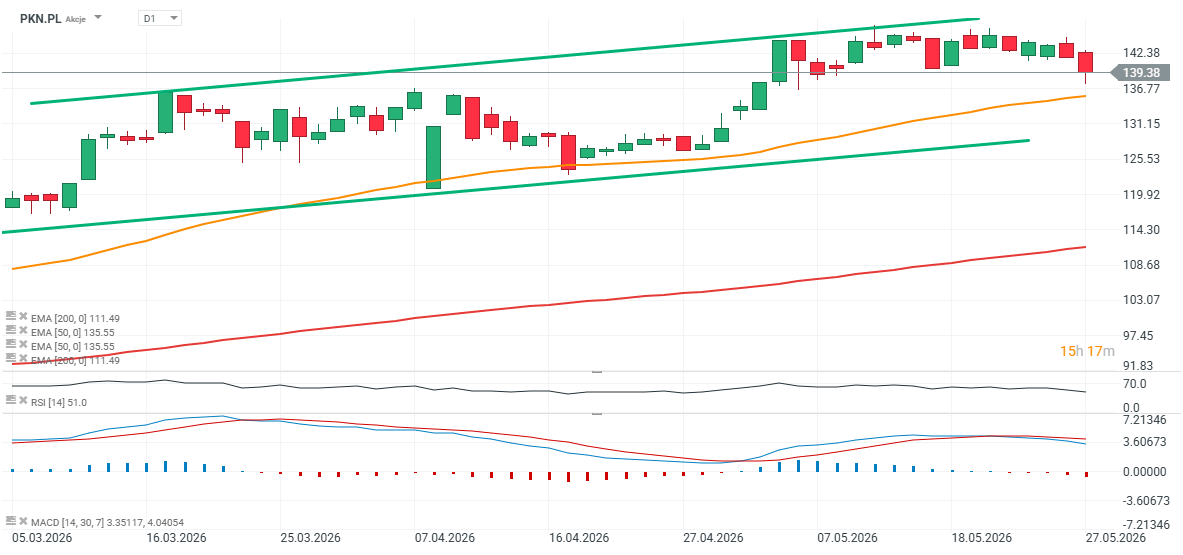

Orlen shares (PKN.PL)

Orlen shares have experienced a modest cooling in sentiment in recent weeks, but the company’s exceptionally strong earnings will likely support another move toward record highs after the opening of today’s trading session in Poland. On the other hand, oil prices declined slightly during Q2, suggesting that repeating such outstanding results may be difficult though not impossible in the current quarter. Key short-term support levels are located near PLN 135 and PLN 128 per share, corresponding to the EMA50 and the lower boundary of the upward trading channel. Meanwhile, the long-term EMA200 support remains almost 30% below the current share price. Resistance is defined by recent highs near PLN 147 per share and the upper boundary of the rising price channel.

Source: xStation5

Eryk Szmyd Financial Markets Analyst, XTB

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

Pfizer is no longer just about COVID; the company reports solid results 💰

Palantir Earnings: High Expectations and Even Bigger Gains

AMD Preview: The Market Has Already Priced in Success. Now the Company Must Deliver

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.