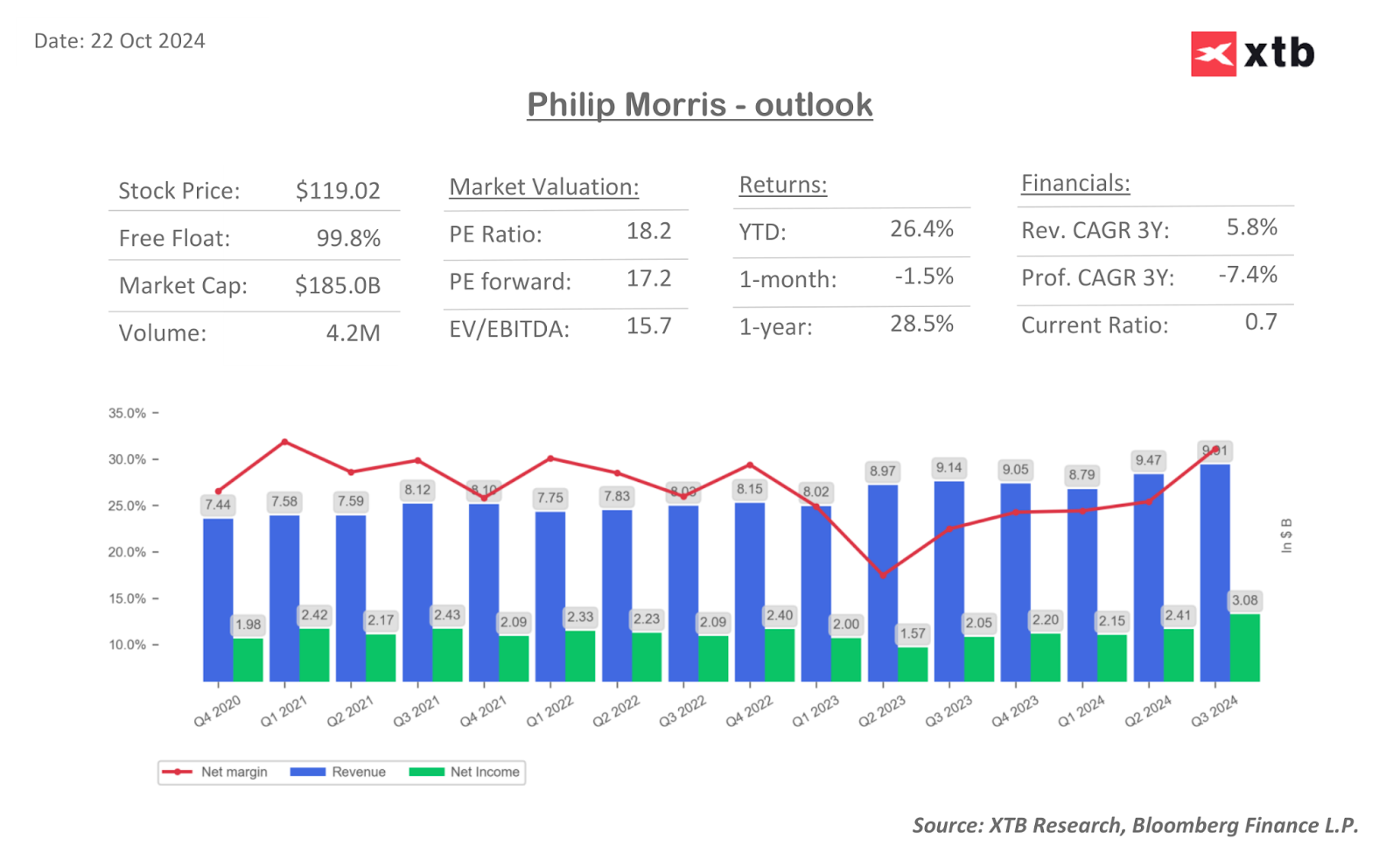

Philip Morris (PM.US) reports better-than-expected results for 3Q24. Higher sales, combined with improved profitability, as well as a final raise in forecasts for the full year 2024, cause the company's stock price to rise more than 7% at the start of the session.

At the revenue level, Philip Morris reported $9.91 billion, beating the consensus forecast of $9.68 billion. The company thus achieved record quarterly revenues, as well as a record net profit, thanks to appropriate cost policies.

Zyn sachets, which contain nicotine and are taken orally by being placed under the upper lip, recorded a 41% increase in sales in the US in the third quarter alone. Philip Morris added that demand for IQOS heated tobacco cartridges in markets such as Greece and Germany is also driving sales.

Philip Morris is seeking to increase sales of alternatives to cigarettes amid growing public awareness of the health effects of tobacco. Although these products contain fewer substances and chemicals linked to cancer and heart disease, their growing popularity is causing controversy, especially among young people who have never smoked before.

Zyn's growing popularity in the U.S. has caused supply problems, but those difficulties are now beginning to abate. The company announced in July that it would invest $600 million in a new manufacturing plant in the US to produce Zyn.

At the adj. EPS level, Philip Morris reported $1.91 (versus a forecast of $1.81). In y/y terms, this represents a 14.4% increase. Underlying such growth was primarily an improvement in net income, which increased to $3.08 billion in 3Q24. The higher growth rate of net income pushed net margin to record highs, thus maintaining the upward trend that has continued since 2Q23. The company reached values in the vicinity of 31%, which in the 2020-2022 period was the upper limits of the margin. The trend of improving net margin in the next quarters may thus be expected to slow down, and may instead consolidate at current levels.

The company also raised its expectations for the full year 2024. It expects adjusted earnings per share to increase 15% this year (excluding changes in foreign exchange rates), up from previous forecasts of 13%, to $6.45-$6.51 (previously: $6.33-$6.45). The upper limit of earlier forecasts as the lower limit of current forecasts is a signal of Philip Morris' confidence in the strength of the current consumer trend regarding the growth in demand for the company's products.

FINANCIAL RESULTS 3Q24:

- Cigarette shipment volume in units 163.24 billion

- Europe cigarette shipment volume 43.74 billion units

- South & Southeast Asia, Commonwealth of Independent States, Middle East, and Africa cigarette shipment volume 91.46 billion Units

- East Asia, Australia & PMI Duty Free Cigarette Shipment Volume 12.81 billion Units

- Americas cigarette shipment volume 15.24 billion Units

- Heated tobacco unit shipment volume 35.35 billion Units, estimate 35.19 billion

- Europe heated tobacco shipment volume 14.20 billion Units

- South & Southeast Asia, Commonwealth of Independent States, Middle East, and Africa heated tobacco shipment volume 7.13 billion Units

- East Asia, Australia, and PMI duty-free heated tobacco shipment volume 13.86 billion Units

- Americas heated tobacco shipment volume 157 million Units

- Adjusted operating income $4.15 billion, estimate $3.93 billion

- Adjusted EPS $1.91, estimate $1.81

Daily Summary: Markets limit the pullback while awaiting the Fed

France Challenges Palantir, Market Reacts.

US OPEN: Deeper sell-off and a SaaS rebound

Mercedes earninigs: Is optimism justified?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.