Rivian is a (still) new, relatively small player in the e-mobility market, yet with enormous potential. Are the risks facing the company just as enormous?

Electric vehicles, regardless of individual investors’ personal attitude toward them, will remain an indispensable part of automotive and transportation for many years, if not decades. The rivalry between Tesla, BYD, and traditional automotive companies is at the center of market interest and research. However, despite the scale of these players and the intensity of their competition, it does not mean that everything has already been said when it comes to business models.

Both Tesla and BYD are focused on chasing economies of scale, which pushes margins in the sector to new lows, forces costly investments, and fuels price wars. Traditional car manufacturers, both in the U.S. and Europe, clearly struggle to “re-tool” their factories, model lineups, dealerships, and design departments for electric cars. In this context, Rivian’s “incremental” approach is a breath of fresh air in the industry and in the market. Innovations in production technology, management, and materials allow even relatively small companies to compete with massive conglomerates, something that would have been difficult to imagine just a dozen or so years ago.

The upcoming launch of the company’s “R2” model is, in the view of many analysts and investors, a “make-or-break” moment for the company, and for good reason. The R2 can be viewed from two perspectives. On the one hand, it represents a departure from the company’s previous imperative: lightness and efficiency. On the other hand, it is a step toward scalability and growth, which is essential if the company is to become more than a market curiosity.

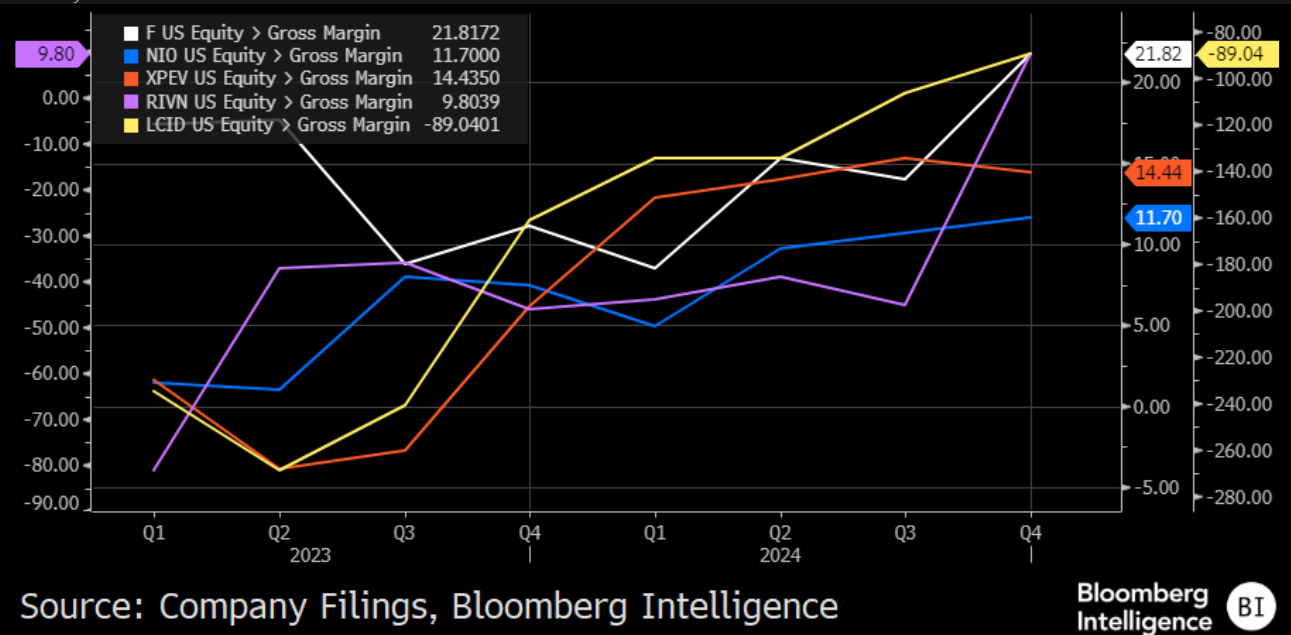

As of today, the company has a number of industry-unique solutions, proprietary components, and software that can compete with industry leaders despite only a fraction of the costs it incurs for development and production. Vertical integration of systems and solutions, as well as platformization, also give the company an edge it desperately needs in an ultra-competitive market.

Source: Bloomberg Finance L.P.

What also gives the company an advantage, one that does not seem to be fully priced in by the market, is its recent agreement with Uber. Considering the potential to supply vehicles to the ride-hailing market’s hegemon, as well as the recent joint venture with Volkswagen, Tesla may find itself in a situation where Rivian “skips a few steps” and begins monetizing robotaxis while bypassing most of the problems Elon Musk’s company is struggling with.

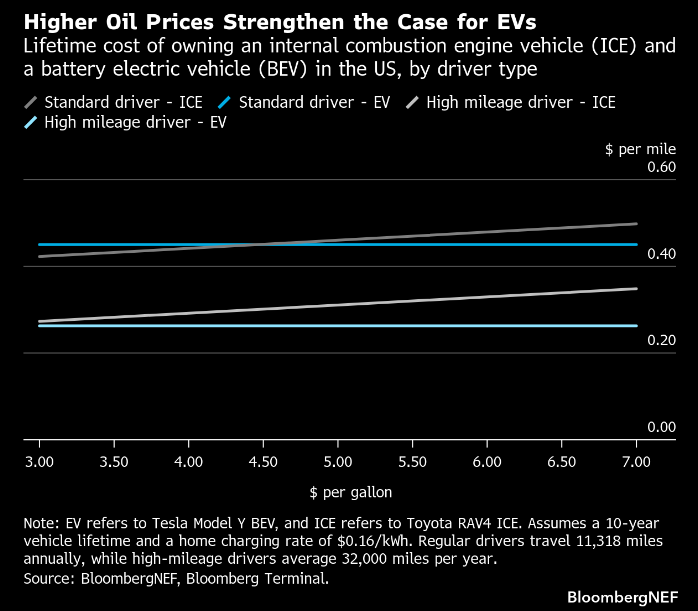

Source: Bloomberg Finance L.P.

Additional support for Rivian is the hard-to-ignore rise in fuel prices. The oil market is not able to wean itself off, or even meaningfully reduce, its dependence on the Middle East, but the global economy can significantly reduce its dependence on oil. The price of gasoline in the U.S. has risen by around 30% over the past month. With Elon Musk’s nearly permanent reputational crisis among current and potential EV owners

in mind, high fuel prices may give Rivian a chance to capture a meaningful share of the market at the best possible moment, especially with the R2 launch ahead.

However, the company still faces a number of risks, not just opportunities. As of today, it is still not profitable—although the trend is strongly improving. The company promises significant growth in financial metrics, and the data partially supports these intentions, but it is worth asking:

- How much of this growth is already priced in (if at all)?

- How likely is it that the company will deliver such an ambitious expansion scenario in such a difficult market?

Investors, both current and prospective, will be looking for answers to these questions during the company’s earnings call on May 12.

RIVN.US (D1)

The company’s shares have continued a bumpy uptrend since the beginning of 2024. A very important signal is the crossover of the EMA100 and EMA200, which is a strong bullish signal. However, it is worth remembering that the valuation—despite the recent gains—still remains far below the peak levels seen at the IPO in 2021.

Ethereum close to $2,000

Texas Instruments earnings: Growth without cash

All or nothing: ServiceNow earnings preview

Did SaaS lost too much? Morgan Stanley says yes.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.