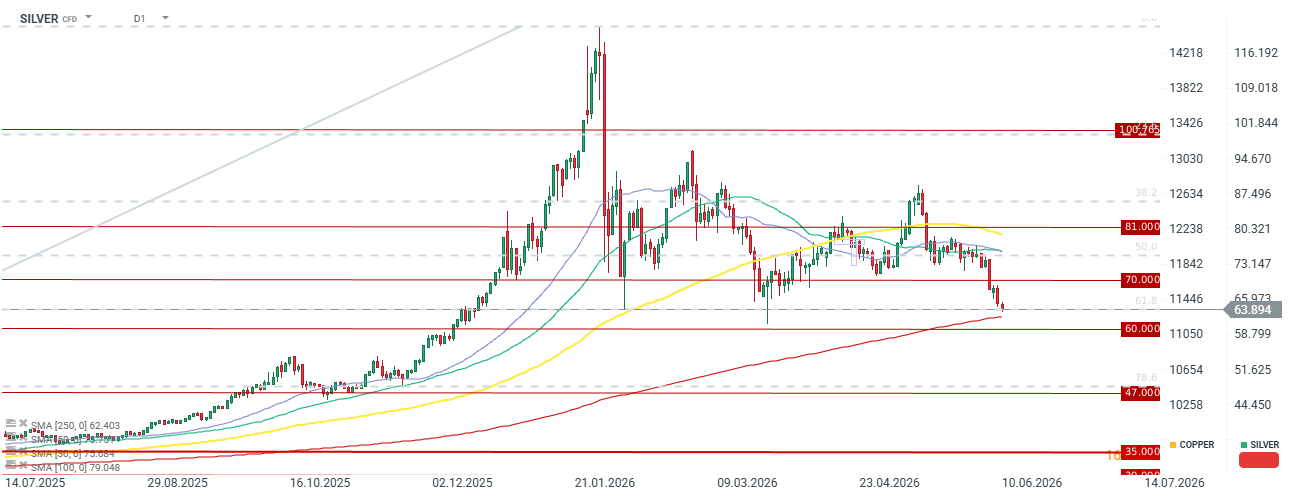

After a strong ~5% sell-off during yesterday's session and a sharp pullback last Friday following NFP data, silver continues to decline today. The decline at the start of Wednesday's session is already 2.5%, and silver is approaching key support defined by the local low from February 6th and March 23rd. Potentially, silver could also be preparing to test the 250-session moving average, which is located just above the $60 level. It is worth mentioning that the 250-session average was last tested in March 2025. Gold has also been declining in recent days, trading below $4,200, although it remains some distance from its local low in March. What are the most important fundamentals in the market right now?

Key Market Fundamentals

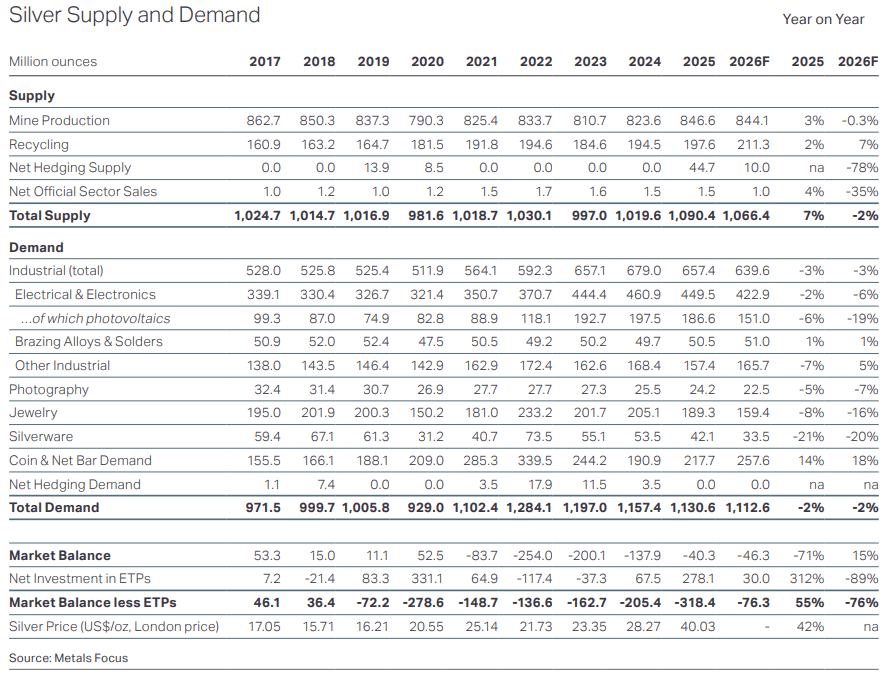

- Six-year structural deficit: The silver market continues to suffer from a shortage of physical metal. According to HSBC analyses, the global market deficit will gradually shrink: from 143 million ounces in 2025 to 73 million in 2026 and 25 million ounces in 2027. Despite the decrease in deficit dynamics, the market remains undervalued. Nevertheless, in the event of an economic collapse, reduced demand in the photovoltaic sector, and a total retreat from ETFs, there is a chance for even a slight oversupply to appear. The $50-60 level range seems attractive, however, considering that silver remains a strategic metal.

- Demand from "green technologies": The industry generates a key supply base. Silver is essential in the production of photovoltaic (PV) panels, next-generation electronics, 5G technology, and the electric vehicle (EV) sector. Despite attempts to reduce the amount of silver in PV cells, the high demand from the technology sector (estimated at over 610–640 million ounces annually) strongly stabilizes the price floor. It is worth noting, however, that the high price of silver will cause attempts to find alternatives such as copper silvering, which significantly limits the costs of building photovoltaic panels.

- Market supply rigidity: Increasing silver mining is technologically difficult because most of this bullion is produced as a by-product of copper, zinc, and lead mining. Mine production in 2026 is expected to remain flat (approx. 844-848 million ounces) and increase only in 2027 (to approx. 868 million ounces), which prevents a quick response to high prices.

- Gold-to-Silver Ratio: This ratio is currently at 65, which is a relatively low level compared to recent years, but still above historical averages. Therefore, it can no longer be said that silver is extremely cheap compared to gold, although we observed a drop to the 40 range during the bull market in precious metals.

- Macroeconomics and geopolitics: Analysts agree that in 2026–2027, the actions of the US Federal Reserve (scale of interest rate cuts), the behavior of the dollar driven by new US trade policy, and high institutional and retail demand in Asian markets (mainly in India and China) will be of fundamental importance for valuation.

The deficit in the markets is expected to decrease significantly, but there is even a chance for an oversupply to appear, with further sell-offs from ETFs and a reduction in photovoltaic demand, which is expected to fall by almost 20% year-on-year. Source: Silver Institute

Price Forecasts from Banks and Institutions

- J.P. Morgan: Forecasts that the average price of silver in 2026 will be $81 per ounce, reaching a quarterly peak in Q4 at an average of $85. In 2027, the bank expects a stable trend and an average price of $85. Analysts, however, warn of increased volatility and the possibility of deeper corrections (even to the $50–60 range) if the economic pace slows down. If JP Morgan's forecasts were to prove true, current prices are starting to look attractive.

- Bank of America (BofA): Presents some of the most aggressive, bullish forecasts. In its base scenario, it assumes a quick return above $100. In the maximum scenario (the so-called bull case), analysts indicate a growth potential to $135, and with an extreme shortage of physical bullion, they allow for a rally even to $309 before the end of 2026.

- Citigroup (Citi): Maintains a very optimistic attitude toward the metal, pointing to the $110–150 range as a realistic medium-term price target.

- Commerzbank: Expects silver to end 2026 at $90. In 2027, it predicts further appreciation, setting a target for the end of that year at $95.

- HSBC: Has raised its forecasts but remains the most conservative among the big players. It expects the average price in 2026 to be $75 (with the year closing around $70), while in 2027 it will fall to an average of $68 (with a target price of $65 at the end of the year). The bank's experts believe that the shrinking supply deficit will cool investor sentiment in the second half of the period.

- LBMA: The annual consensus of analysts affiliated with the LBMA sets the average for 2026 at around $79.57. However, the discrepancy in opinions is enormous – the lowest bear forecasts are around $42, while extreme optimists predict levels of 165+ USD.

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.