- Software stocks fall ahead of the U.S. market open

- IBM warns that enterprise customers are cutting software spending

- Investors fear the entire industry could enter a slowdown in new orders

- Software stocks fall ahead of the U.S. market open

- IBM warns that enterprise customers are cutting software spending

- Investors fear the entire industry could enter a slowdown in new orders

Software and consulting stocks are selling off sharply after IBM released preliminary second-quarter results that missed expectations on both revenue and earnings. More importantly, IBM highlighted a noticeable shift in enterprise customer behavior, which investors interpreted as a potential warning sign for the broader enterprise software market.

The biggest decliners include:

- IBM: more than -20%

- Accenture: around -8%

- Cognizant: around -7%

- ServiceNow: around -7%

- Salesforce: around -5%

- Workday: around -5%

- Adobe, HubSpot, Datadog, and Microsoft: more than -3%

Companies are shifting spending from software to AI infrastructure

Beyond the disappointing financial results, the market focused primarily on comments from IBM CEO Arvind Krishna regarding customer behavior toward the end of June. According to IBM, many enterprise customers have begun redirecting IT budgets away from software, traditional IT services, and digital transformation projects toward servers, storage systems, and memory chips in an effort to secure critical hardware before prices rise even further.

The main driver behind this trend is the ongoing global shortage of HBM and DRAM memory. Massive demand from hyperscalers and AI infrastructure investments continues to push up prices for key data center components. As a result, enterprises are allocating a growing share of their IT budgets to hardware purchases, leaving less capital available for software licenses, SaaS subscriptions, consulting services, and new software deployments.

The market fears a broader slowdown across enterprise software

For investors, the key concern is that this issue may extend well beyond IBM. If enterprises continue reallocating capital from software toward AI infrastructure, software and consulting companies could face slower revenue growth over the coming quarters.

These concerns have found fertile ground because investors were already worried that AI could eventually reduce demand for traditional enterprise software and consulting services, creating longer-term headwinds for many companies in the sector. IBM also pointed to rapidly increasing cybersecurity threats, which further diverted customers' attention from executing some IT projects during the final weeks of the quarter.

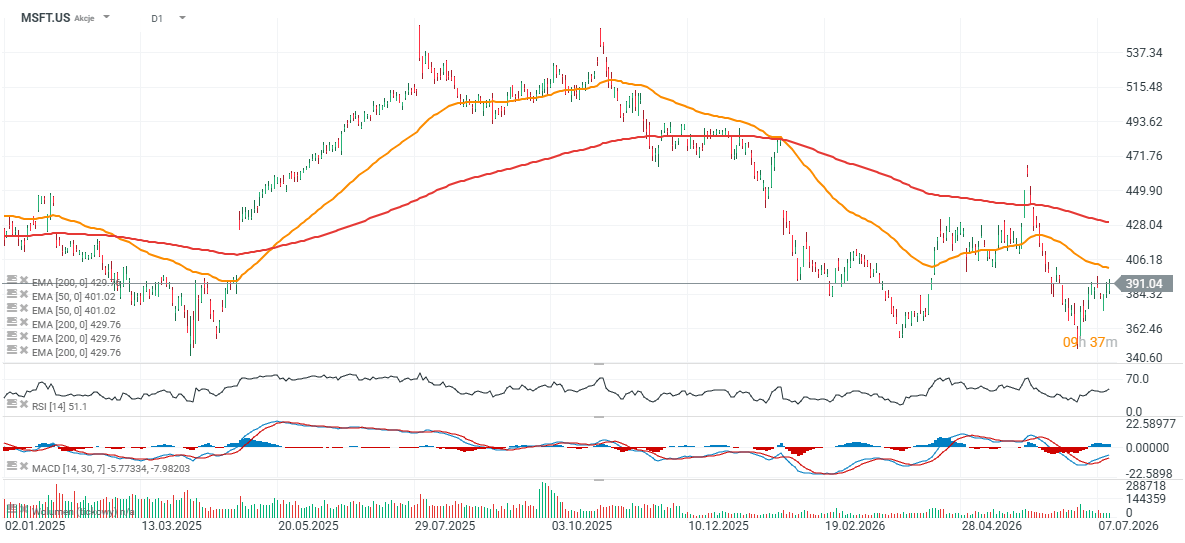

Microsoft shares (D1 timeframe)

Microsoft shares have fallen roughly 7% below their 200-day EMA (red line) and are now down nearly 30% from their all-time highs. The company has endured a challenging start to the year. After rebounding by around 10%, the RSI has recovered to 51, indicating a neutral technical position from which the stock could theoretically experience either a strong bullish or bearish move.

Source: xStation5

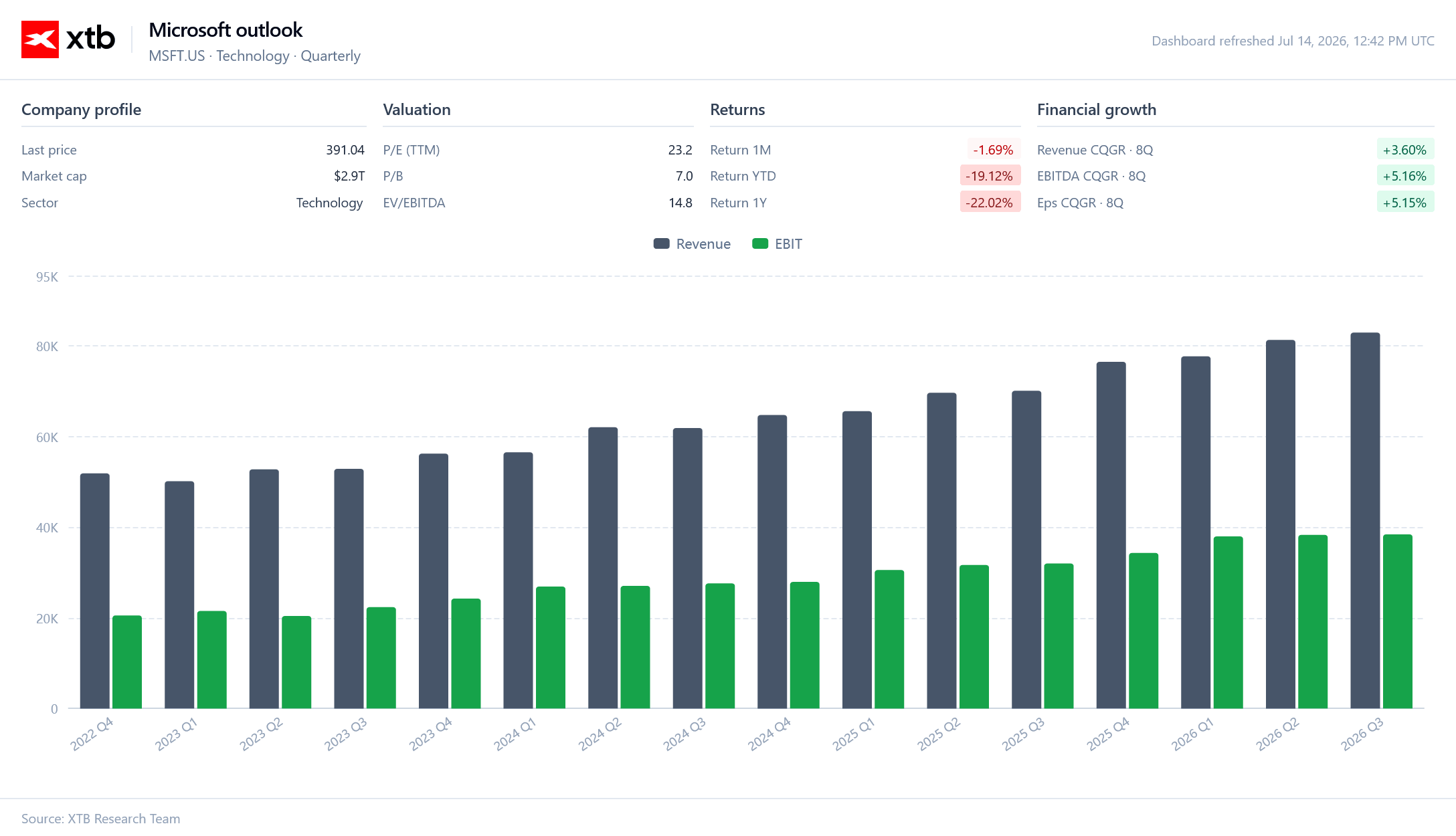

Microsoft shares are now down approximately 20% year-to-date, making the company one of the weakest performers among Wall Street's mega-cap technology stocks despite a significant year-over-year improvement in its financial results. With a P/E ratio of around 23, the valuation is not particularly demanding relative to the Nasdaq average. However, investors remain concerned about the company's massive AI-related capital expenditures, its exposure to a potentially slowing enterprise software cycle, and its substantial investment in OpenAI, which competes directly with other leading AI developers, including Anthropic.

Source: xStation5

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.