- Bunge agreed to purchase Viterra

- Transaction finance with 75% in stock and 25% in cash

- Bunge to repurchase own shares worth $2 billion

- Merger will combine world's largest oilseed crusher and one of top grain traders

- Combined entity will be able to compete with heavyweights like ADM or Cargill

- Surprisingly, Bunge does not seem to be strongly correlated with grains market

- Bunge's share price gained 3% after merger announcement but failed to break above $97 resistance

Recent rally on stock markets was driven by the AI craze as well as short covering on meme-stocks. Given all the buzz around those stocks, it was easy for traders to miss other noteworthy stock news, like for example one of the biggest agribusiness merger announcements in history! Bunge (BG.US), US agribusiness company, announced this Tuesday that it will buy Viterra, a grain handling business, from Glencore (GLEN.UK).

Bunge agrees to buy Viterra

Bunge announced on Tuesday, June 13 that it has agreed to purchase Viterra, a grain handling business, from Glencore, Swiss commodity trading and mining company. Bunge will pay around 65.6 million of its own shares worth $6.2 billion as well as additional $2 billion in cash to Viterra shareholders. Bunge also plans to repurchase its own stock worth $2 billion in order to enhance EPS accretion. As a result, shareholders of Viterra will own around 30% of the combined entity after the transaction closes and around 33% of the combined entity once Bunge's stock repurchases are completed. Deal is expected to close in mid-2024 and result in $250 million annual pre-tax synergies within three years.

However, whether the deal goes through or not will depend on regulatory approvals. It is expected that significant antitrust concerns will be raised by regulators in Argentina, world's biggest exporter of soymeal and soy oil, as combined Bunge-Viterra will have a dominant share of the soy processing market in the country.

Viterra sale is not a surprise

Merger between Bunge and Viterra is not entirely surprising. Glencore was approaching Bunge previously over a possibility of friendly takeover of Viterra as Viterra grain business does not synergies well with Glencore's metals business. While Bunge has rejected Glencore's offers in previous years, Bloomberg reported as recently as last month that the two are once again discussing potential merger.

Combination to create agribusiness heavyweight

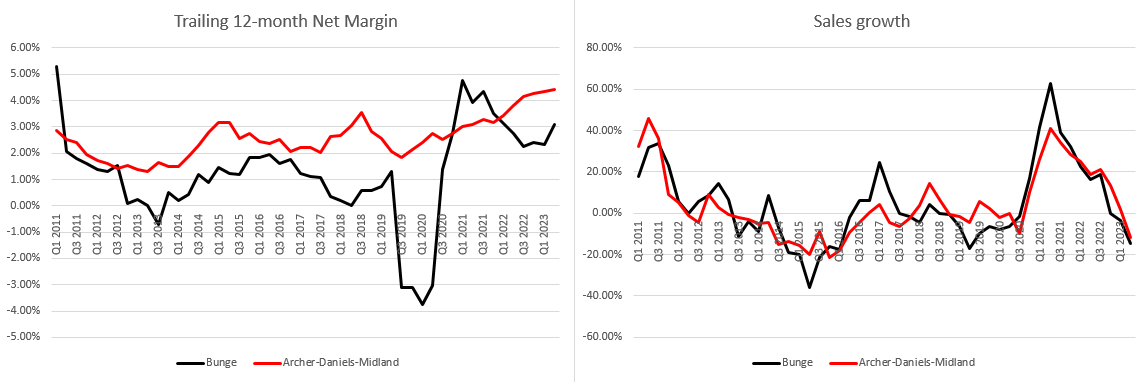

Merger between Bunge and Viterra will be one of the biggest in the agribusiness sector in history and will create a $34 billion heavyweight company that will be able to compete with its top rivals - Archer-Daniels-Midland (ADM.US) and privately-held companies - Cargill and Louis Dreyfus. While data for Cargill or Louis Dreyfus is unavailable, comparing financial data for Bunge and Archer-Daniels-Midland we can see that the two have a very similar profile. Sales growth of the two companies moves in tandem but net interest margins of Bunge are much more volatile. It should be noted that the combination of Bunge and Viterra is a combination of the biggest oilseed crusher in the world (Bunge) with one of top grain traders (Viterra) and therefore should help diversify business and make it more resilient. Assets of the two companies are said to be complementary and Bunge's CEO said that merger will create more capability for the company in down cycles.

While Archer-Daniels-Midland and Bunge enjoyed similar growth in sales in recent years, Bunge's net margin was much more volatile and usually lower than ADM's. Source: Bloomberg, XTB

While Archer-Daniels-Midland and Bunge enjoyed similar growth in sales in recent years, Bunge's net margin was much more volatile and usually lower than ADM's. Source: Bloomberg, XTB

Indirect exposure to the grains market?

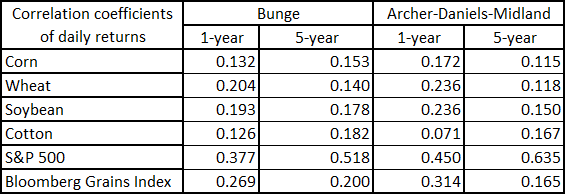

As Bunge is an agribusiness company heavily involved in grains trading, one could think that its shares may offer an indirect exposure to the grains market. Taking a look at the chart below, which plots Bunge share price against Bloomberg Grains Index, one may rule that the stock is indeed highly correlated with the grains market and may be used to obtain exposure to grains. However, a look at the table below with correlation coefficients shows that it is not necessarily the case. Over the past year as well as over the past 5-year period, correlation between daily returns of Bunge and grains has been very weak. The same can be said about Bunge's biggest publicly traded rival - Archer-Daniels-Midland. In fact, those two stock showed moderate correlation (0.4-0.6) only with the broad stock market (S&P 500 in this case).

Bunge (BG.US) seems to have a strong correlation with Bloomberg Grains Index. Source: Bloomberg

Bunge (BG.US) seems to have a strong correlation with Bloomberg Grains Index. Source: Bloomberg

However, correlation between daily returns over 1- and 5-year periods suggest that shares have more stock-like characteristics and are rather weakly correlated with the grain market. Source: Bloomberg, XTB

A look at the chart

Shares of Bunge (BG.US) gained over 3% on Tuesday after the deal was announced. While the upward move continued yesterday, bulls failed to push the stock above a $97.00 resistance zone. A long upper wick of yesterday's daily candlestick suggest that there is a strong bear camp in the area and a catalyst may be needed for a move above the zone and regulatory clearance for the deal could be such a catalyst. However, regulators are likely to take time to assess the impact on the merger. Unless such a catalyst surfaces, stock may remain locked in the $89.50-97.00 trading range.

Bunge (BG.US) at D1 interval. Source: xStation5

Bunge (BG.US) at D1 interval. Source: xStation5

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.