Since artificial intelligence became one of the main themes driving global financial markets, investors have primarily focused on semiconductor companies. NVIDIA, AMD, and Broadcom have become symbols of the new technological reality. Increasingly, this group also includes Micron, SK Hynix, Samsung, and SanDisk, which are benefiting from growing demand for memory solutions used in modern data centers.

This should not come as a surprise. Graphics processors and high bandwidth memory are the technologies responsible for training and operating increasingly advanced artificial intelligence models. Without them, the development of AI would look completely different today. However, hidden behind this technological revolution is another segment of the market that rarely receives attention from financial media.

Every artificial intelligence model does not only process data. Above all, it constantly creates new data. Training datasets, analytical results, images, videos, backups, and user archives gradually become valuable resources that must be securely stored. The faster artificial intelligence develops, the faster the global amount of information requiring storage continues to grow.

This leads to a simple question.

If artificial intelligence needs more and more data, where will all of it actually be stored?

The answer does not lead to GPU manufacturers or HBM memory suppliers. It leads to companies building the infrastructure responsible for long term data storage. One of them is Seagate Technology.

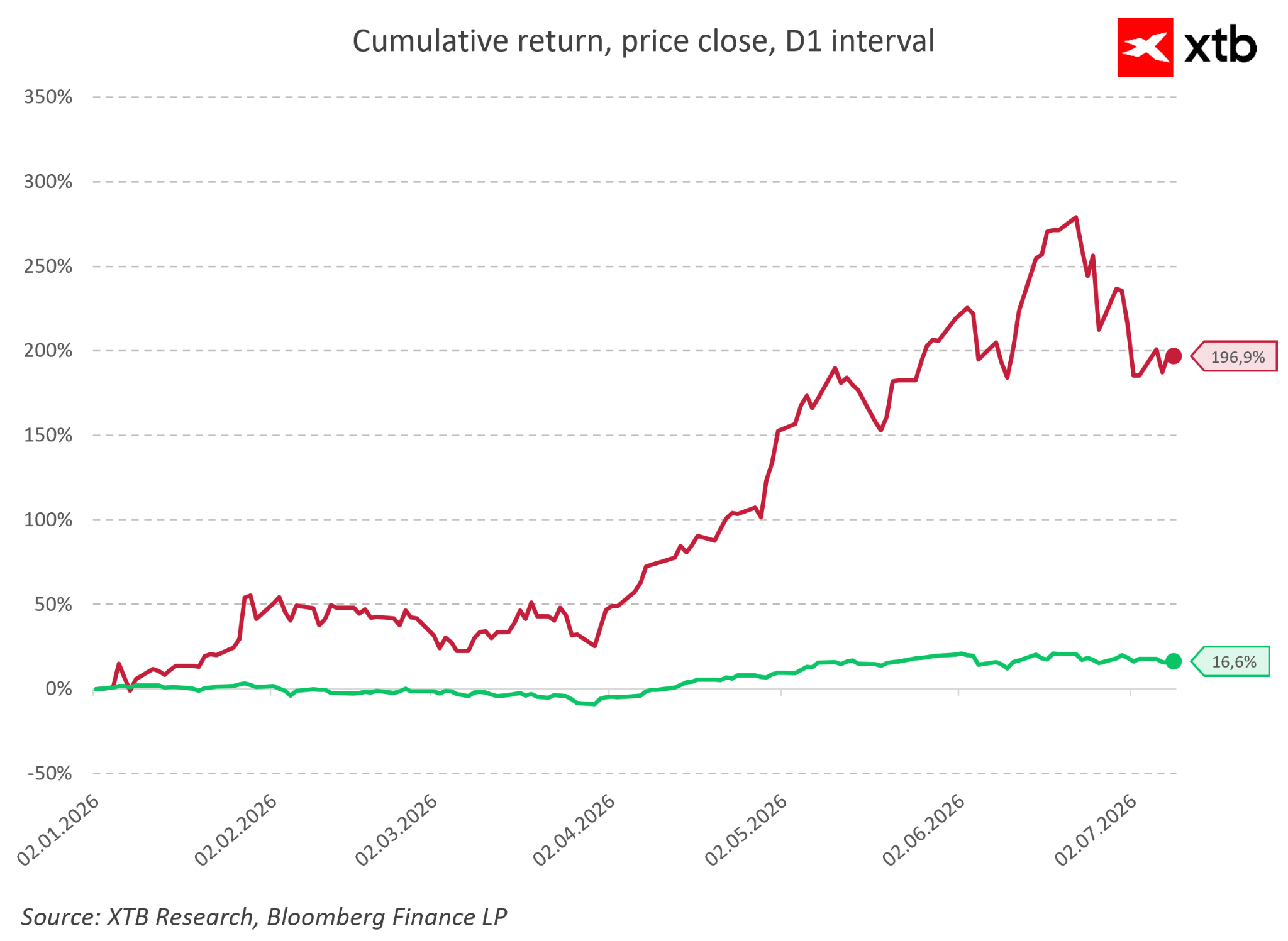

Although the company’s share price has increased by more than 180 percent since the beginning of the year, the market is still primarily focused on the most obvious beneficiaries of the AI revolution. However, artificial intelligence is not only about increasing demand for computing power. It also means an exponential increase in the amount of data that must be stored for years. This less visible part of the infrastructure may prove to be one of the most underestimated elements of the entire AI ecosystem.

That is precisely why Seagate deserves closer attention. The company has spent decades working on something that, until recently, many investors considered a technology slowly approaching the end of its lifecycle.

AI Needs More Than Computing Power. It Needs Storage.

Over the past two years, the market has focused almost entirely on one element of artificial intelligence infrastructure: computing power.

This focus is understandable. Graphics processors are responsible for training AI models and performing trillions of calculations within fractions of a second. Without them, the development of modern artificial intelligence would not be possible.

However, even the most advanced AI model does not operate in isolation. To be trained, it requires enormous datasets. Later, it generates additional information that must also be stored, secured, and managed. Every conversation with a chatbot, every generated image, every document analysis, and every line of code contributes to the global pool of data.

This is why the development of AI does not only increase demand for processors. It also increases demand for infrastructure responsible for storing information.

Moreover, not all data requires the same level of accessibility. In practice, only a small portion of information is constantly accessed by the fastest processors and highest performance memory systems. The vast majority eventually moves into storage layers where the most important factor is not speed, but the cost of storing massive volumes of data.

And this is exactly where hard disk drives remain a solution that has yet to be replaced.

Although SSDs offer significantly higher performance, they remain much more expensive when measured by cost per terabyte of storage. For the largest data center operators managing millions of gigabytes of information, this difference has enormous economic consequences.

In practice, HDDs are not directly competing with the memory technologies used for the most demanding workloads. They serve a different purpose. They are the foundation of long term data storage. This is why artificial intelligence does not eliminate the need for hard drives. On the contrary, it increases demand for solutions capable of offering greater capacity at the lowest possible cost per terabyte.

This shift is clearly visible in the growing demand for HDDs used by cloud providers and the world’s largest data centers.

Old Technology, New Role. Why HDDs Remain a Foundation of AI

The artificial intelligence revolution does not mean that every part of the infrastructure must be the newest and fastest technology available. Quite the opposite. Modern data centers are becoming increasingly complex ecosystems where each technology performs a specific function.

Graphics processors provide the enormous computing power required to train and operate AI models. High performance semiconductor memory allows these systems to process the most important information at incredible speeds. However, somewhere between these advanced components there must be another layer responsible for storing unimaginable amounts of data.

This is where hard disk drives come into play.

Contrary to earlier expectations, the rise of artificial intelligence has not made HDDs obsolete. The reason is simple: data centers do not need only speed. They also need enormous capacity and the lowest possible cost of storing each terabyte of information.

SSDs remain unmatched in applications where maximum performance and instant access to data are critical. However, when dealing with massive datasets, archives, backups, and information generated by AI models, economics becomes the most important factor.

At a scale measured in millions of gigabytes, even a small difference in the cost of storing one terabyte can translate into billions of dollars in savings.

This is why the future of data storage is unlikely to be a complete replacement of HDDs by SSDs. A more realistic scenario is a model where both technologies coexist, each serving a different role within the broader data ecosystem.

The biggest change is therefore not the return of old technology, but its rediscovery in a completely new environment. Hard drives, once viewed by many investors as a declining technology, have become one of the essential components supporting the continued expansion of artificial intelligence. This is where Seagate’s advantage becomes visible.

The company is not competing with AI chip manufacturers for the title of the most advanced technology provider. Its role is different. Seagate provides the infrastructure without which the entire artificial intelligence ecosystem would face significant limitations.

However, the biggest challenge for HDD manufacturers remains the continuous improvement of capacity and maintaining their cost advantage.

This is why Seagate’s development of Heat Assisted Magnetic Recording (HAMR) technology is so important. It is designed to enable further increases in storage density and extend the relevance of hard drives in an era of rapidly expanding data volumes.

From Crisis to Record Profitability. Seagate’s Financial Transformation

Technology alone does not create shareholder value. Even the most advanced solutions have limited importance if they do not translate into measurable improvements in financial performance.

In Seagate’s case, recent quarters show something more than a simple recovery after a difficult period. The company is undergoing a significant qualitative transformation driven by both improving market conditions and the growing importance of data storage in the age of artificial intelligence. Not long ago, Seagate’s situation looked completely different.

The hard drive market was under pressure from weaker economic conditions, customer inventory reductions, and lower enterprise spending on IT infrastructure. After a period of exceptionally strong demand during the pandemic, the industry entered a correction phase, leading many investors to question whether HDD manufacturers were approaching the final stage of their development.

The problem was that part of the market evaluated Seagate only through the lens of its historical business model: traditional data storage hardware.

Meanwhile, the economics of the entire data market were changing.

The rise of artificial intelligence caused demand for storage capacity to grow faster than many expected. The largest data centers now require not only computing power, but also enormous storage capacity for information generated by AI models, cloud applications, and digital services. This shift has already started appearing in Seagate’s financial results.

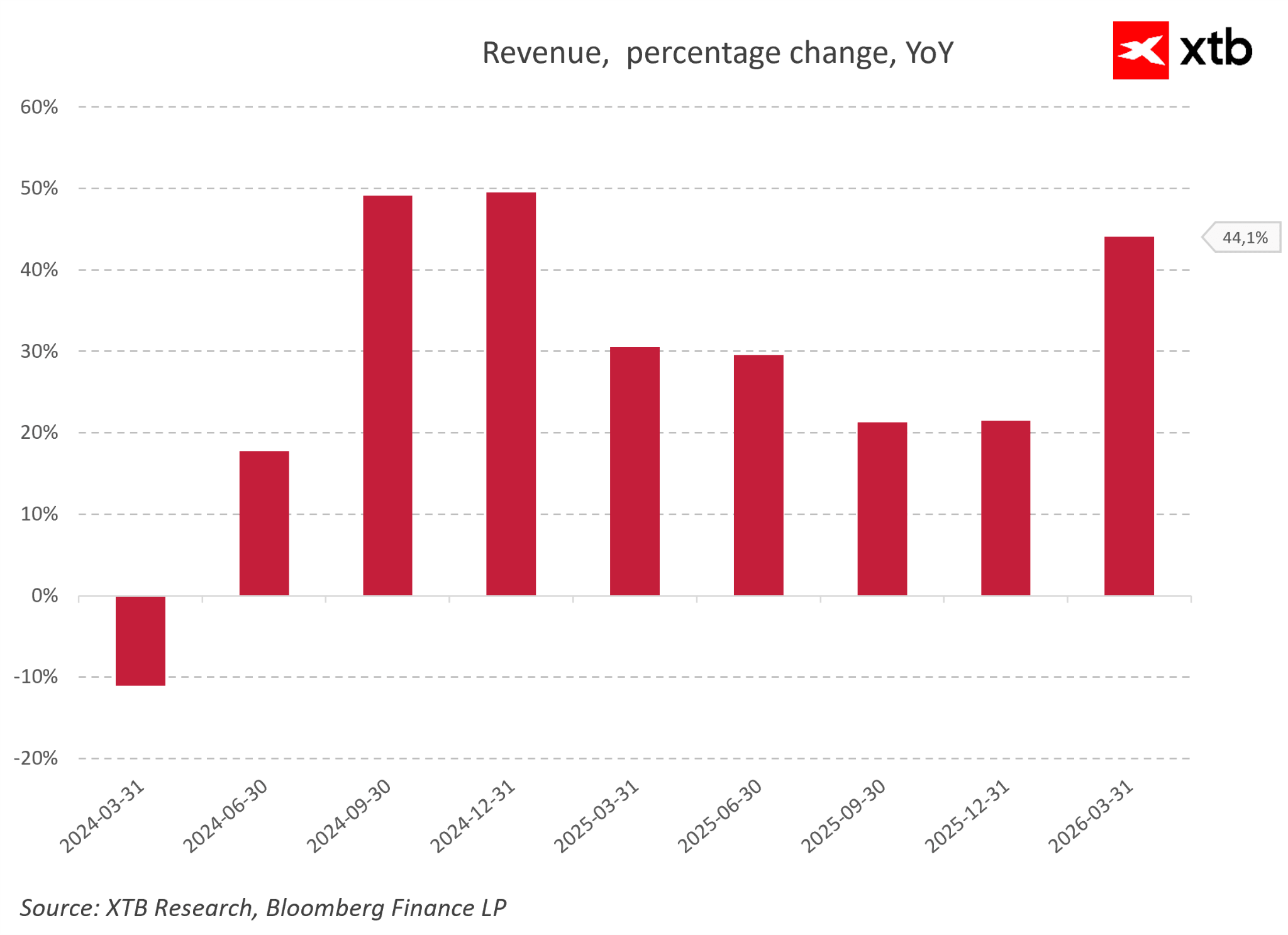

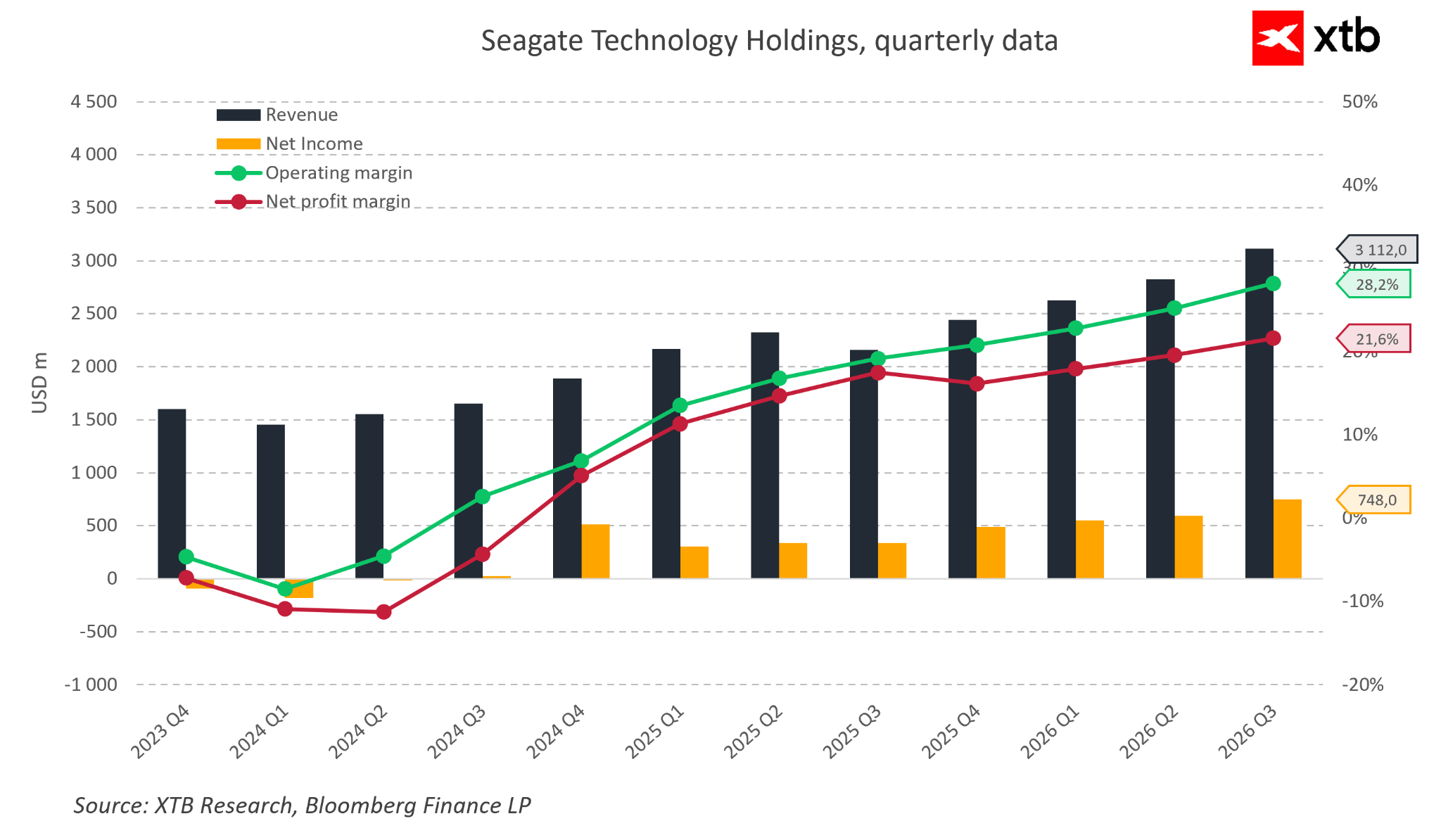

In the third fiscal quarter of 2026, the company generated $3.11 billion in revenue, representing growth of approximately 44 percent compared with the same period a year earlier. Even more important was the improvement in profitability. GAAP gross margin increased from 35 percent to nearly 47 percent, while operating margin expanded from 20 percent to more than 32 percent.

This means Seagate is not only selling more products. The company is also benefiting from a more favorable product mix, with high capacity solutions for data centers becoming increasingly important.

Seagate is moving away from a business model focused primarily on shipment volume toward a model where the technological value of each product and its importance within the broader data infrastructure ecosystem matter significantly more. From an investor’s perspective, the key point is that Seagate’s investment thesis is not based solely on the assumption that the storage market will grow alongside the amount of generated data.

Market growth alone would not be enough to create an attractive investment opportunity. What matters more is that Seagate operates in a segment where technology leadership and manufacturing scale allow the company to continuously improve its economic efficiency.

The growing share of high capacity drives increases the value of each product sold while allowing the company to better utilize its existing manufacturing infrastructure.

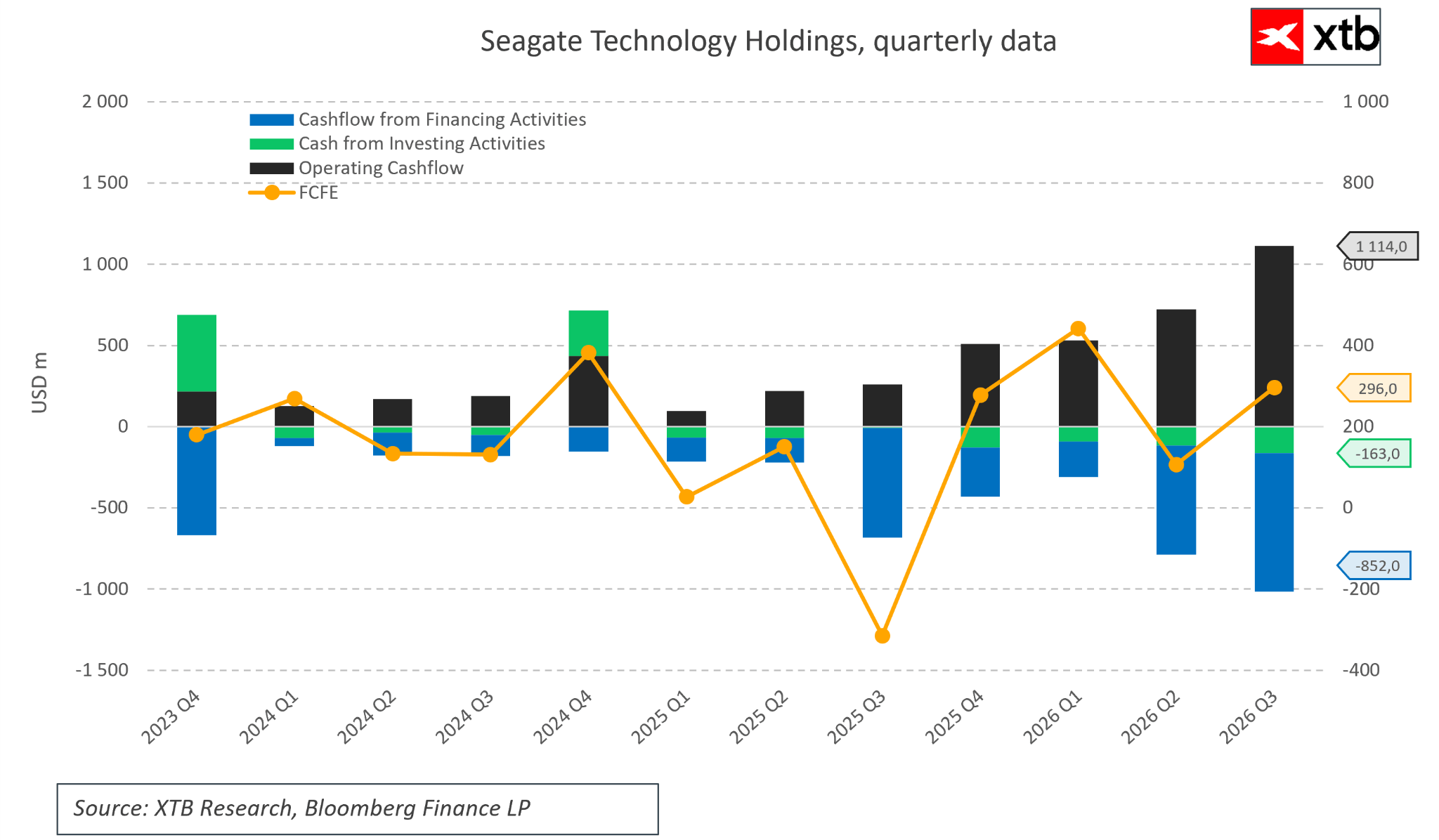

For the largest cloud providers, higher capacity per drive translates into lower storage costs, reduced energy consumption, and less physical space required in data centers. In a world where the amount of information is expanding exponentially, infrastructure efficiency is becoming one of the most important competitive advantages. The strongest evidence of improving business quality is not only revenue growth or higher profits, but also the ability to generate cash.

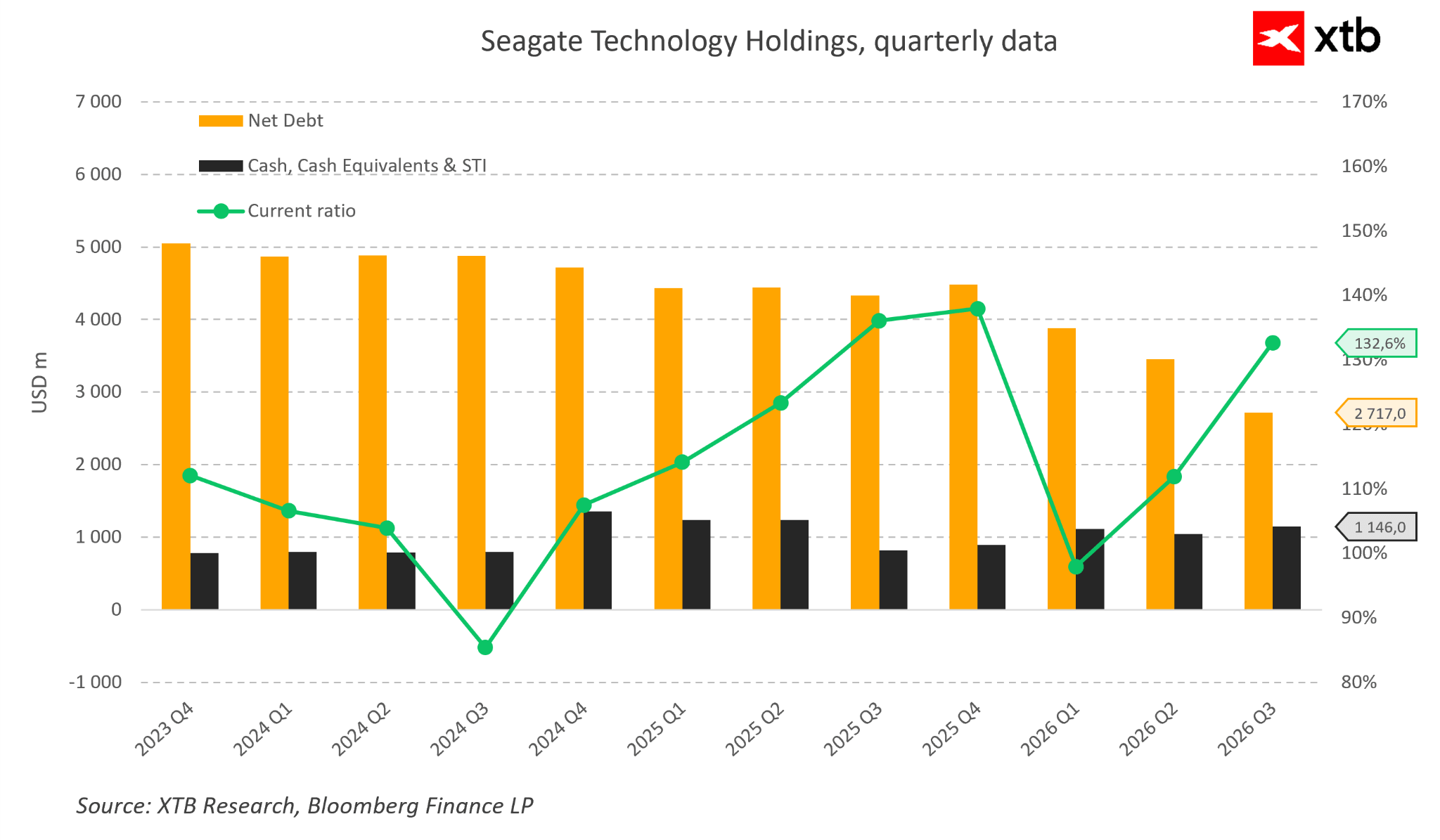

In the third fiscal quarter of 2026, Seagate generated approximately $953 million in free cash flow. Such strong cash generation allowed the company to simultaneously reduce debt and return capital to shareholders. During the analyzed quarter, the company allocated approximately $641 million toward debt reduction, while continuing shareholder returns through dividends and share repurchases.

An improving balance sheet reduces financial pressure and increases Seagate’s flexibility during future phases of the industry cycle. The improvement in cash generation is also accompanied by a change in the quality of profitability.

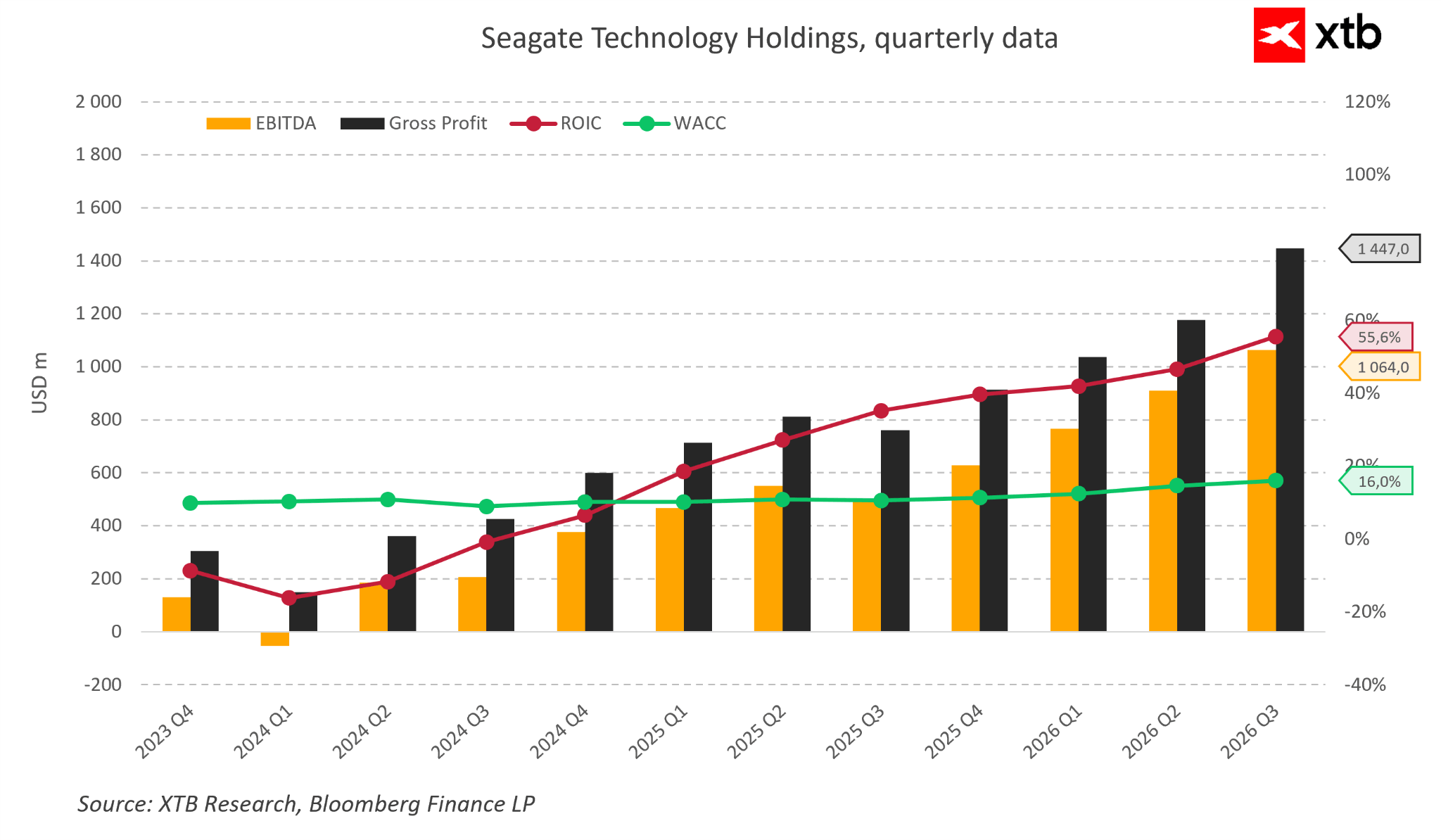

Rising operating income and higher returns on invested capital suggest that Seagate’s current phase increasingly resembles a value creating business rather than simply a company recovering from a temporary downturn.

If capital allocated toward HAMR technology development, production expansion, and the growth of the Lyve platform continues generating returns above the company’s cost of capital, it would represent a fundamental improvement in the economics of the entire business. Until recently, the main argument against Seagate was concern about the future of the traditional hard drive market.

Current results suggest, however, that Seagate is no longer competing only as a manufacturer of storage devices. It is increasingly becoming a provider of critical infrastructure for a global economy built around artificial intelligence and data.

Of course, this does not mean that all risks have disappeared.

The industry remains cyclical, and the current improvement in results is partly supported by an exceptionally favorable demand environment. Competition from semiconductor based storage technologies remains an important factor, especially in applications requiring the highest performance.

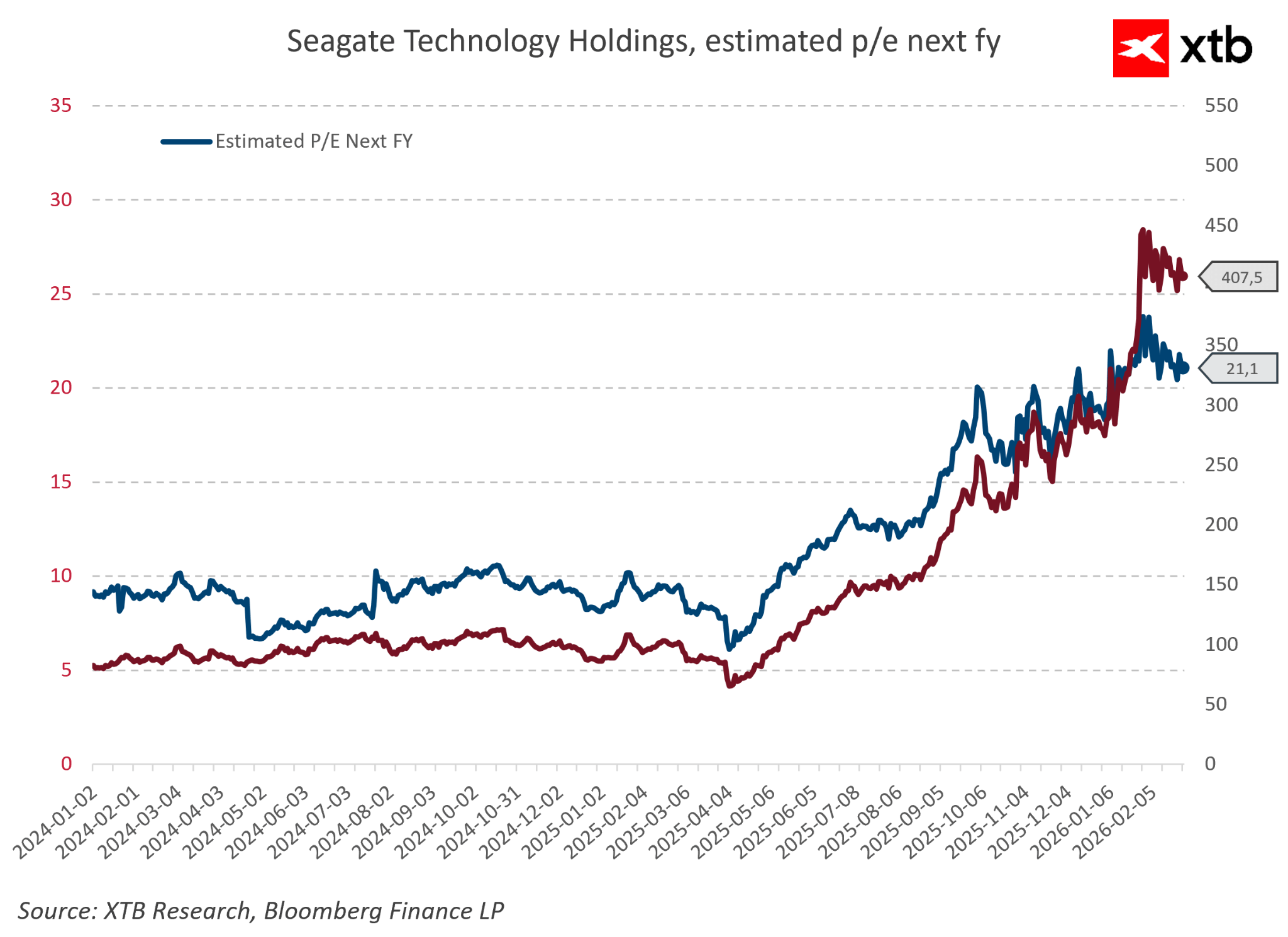

Additionally, the significant increase in Seagate’s share price has raised investor expectations regarding future results. The market dimension of this transformation cannot be ignored either.

The increase in Seagate’s valuation has been driven not only by stronger fundamentals, but also by a change in investor perception.

For years, Seagate was viewed as a company operating in a mature industry with limited growth prospects. Today, investors increasingly recognize it as a potential beneficiary of the long term increase in global data creation.

At the same time, such a rapid change in market perception serves as a reminder that investment stories rarely move in a straight line. After periods of strong appreciation, corrections often occur, particularly when market expectations rise faster than actual business performance. The most important change is therefore not only financial.

It is the way investors now view Seagate.

The company is gradually moving away from being perceived as a manufacturer of outdated technology and is increasingly being considered one of the beneficiaries of the long term growth in data demand.

If artificial intelligence continues to increase demand for storage infrastructure, Seagate may find itself in a much stronger position than previous market narratives suggested.

Therefore, the key question for investors is no longer whether the company can survive another industry cycle.

The real question is whether the current improvement in results represents the beginning of a new chapter in Seagate’s history or simply another temporary peak created by unusually favorable market conditions.

Key Risks

Every strong investment thesis has another side.

In Seagate’s case, the arguments supporting long term growth are compelling, but investors must remember that the company operates in an industry characterized by high cyclicality and significant sensitivity to changes in demand.

The current improvement in results may represent the beginning of a lasting transformation, but there is also a scenario where some of today’s benefits prove to be the result of an unusually favorable market environment. The biggest risk remains the cyclical nature of the storage industry.

History has repeatedly shown that periods of strong demand often encourage companies to increase production capacity, which can eventually lead to oversupply and pricing pressure. If investment in artificial intelligence related data centers slows, Seagate could once again face pressure caused by demand normalization.

The second major factor is competition from semiconductor based storage technologies.

SSDs already dominate applications where maximum speed is essential, while HDDs remain critical in areas where the cost of storing massive amounts of data is the primary consideration.

The key question is whether further declines in NAND flash prices could gradually weaken the economic advantage of hard drives. This does not mean SSDs will automatically replace HDDs.

The difference in cost per terabyte remains the strongest argument supporting Seagate’s technology. However, maintaining this advantage requires continued technological development, including future generations of HAMR technology and further increases in storage density. Another risk comes from customer concentration.

The largest data center operators possess significant negotiating power, and their investment decisions can directly influence the growth rate of the entire market.

Even the best technology must compete in an environment where price and cost efficiency remain critical purchasing criteria. The final factor is valuation risk.

For many years, Seagate was treated as a company operating in a declining industry. However, improved financial results and the AI driven change in market perception have significantly increased investor interest.

The current share price assumes that high profitability will continue and that the data storage market will keep expanding. Any disappointment regarding margins, revenue growth, or AI infrastructure investment could lead to a sharp correction in valuation. The biggest challenge for investors is therefore not whether Seagate is a better company today than it was several years ago.

Financial results and improving competitive positioning suggest that it is. The key question is how long Seagate’s technological advantage, favorable market structure, and rising demand for data storage will continue supporting further growth.

Valuation Perspective

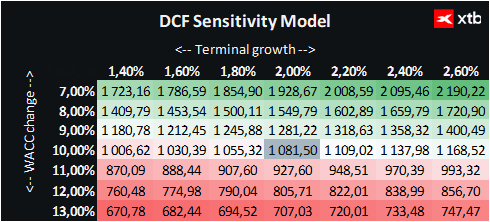

The following valuation of Seagate Technology Holdings is based on the discounted cash flow (DCF) method. It should be emphasized that this analysis is provided for informational purposes only and should not be considered an investment recommendation or a precise determination of the company’s fair value.

Seagate is currently at an important point in its history.

For many years, the company was viewed primarily as a representative of a mature hard drive industry. However, the development of artificial intelligence has changed the way the entire data storage sector is perceived.

The growing amount of information generated by AI models, cloud services, and digital applications is increasing the strategic importance of infrastructure responsible for storing and managing data.

Based on the current share price of $853 and a DCF valuation indicating an estimated intrinsic value of $1,081, the implied upside potential is approximately 27 percent. This suggests that, assuming Seagate maintains strong profitability and the AI driven storage market continues expanding, the current valuation may still leave room for further appreciation.

At the same time, the market has already recognized part of Seagate’s transformation. The increase in the company’s share price has been driven not only by stronger financial results but also by a shift in how investors perceive the business.

The market increasingly views Seagate not simply as a traditional hard drive manufacturer, but as one of the beneficiaries of the long term growth in global data creation. However, the biggest risk remains the possibility that the current improvement in profitability is partly cyclical.

A slowdown in data center investments, renewed pricing pressure, or stronger competition from semiconductor based storage technologies could limit future margins.

Therefore, the key question for investors is not whether Seagate has improved its position compared with several years ago, because financial results clearly indicate that it has.

The most important question is whether the current transformation represents a permanent change in Seagate’s role within the artificial intelligence ecosystem, or simply another phase of the traditional storage industry cycle.

Conclusion. Can Seagate Become One of the Long Term Winners of the AI Revolution?

The biggest technological shifts often create winners that are difficult to identify at the beginning. In the case of artificial intelligence, investor attention has focused primarily on companies providing computing power.

NVIDIA, AMD, and Broadcom have become symbols of the new technological era because their solutions enabled the development of the most advanced AI models. However, every technological revolution also requires infrastructure operating outside the spotlight.

Artificial intelligence does not rely only on processors. It also requires enormous storage capacity capable of preserving the constantly growing amount of information generated by modern digital systems.

This is where Seagate enters the story. For years, the company was viewed as a representative of a mature hard drive industry with limited growth prospects. The development of AI has changed the economics of the entire data market.

The rapidly increasing volume of information generated by data centers has given storage technologies renewed strategic importance.

Today, Seagate has several elements that create an interesting investment case.

The company operates in a highly concentrated market, continues developing HAMR technology, benefits from rising demand for data infrastructure, and has already started translating these trends into measurable financial improvements.

Higher margins, strong cash generation, and an improving balance sheet indicate that the current transformation is more than just a future promise. However, this does not mean the investment case is without risk.

Seagate still operates in a cyclical industry, competes with alternative storage technologies, and must prove that its current profitability level can be maintained over the coming years.

Additionally, the market has already priced in part of the positive scenario, increasing expectations for future performance. The biggest paradox of this story is that one of the beneficiaries of the artificial intelligence revolution may be a company that for years was associated with outdated technology. Yet technological progress does not depend only on creating faster processors.

It also requires building the infrastructure that allows humanity to store, manage, and utilize an ever growing amount of information.

And this is exactly why Seagate remains a company worth watching.

Not because it stands at the center of today’s AI narrative, but because without storage infrastructure, the entire artificial intelligence ecosystem would struggle to scale.

Meta shows how to lose almost 10% despite record sales due to AI development

Microsoft shows how to make money on data centers. AI investments are starting to pay off

Meta Preview: Will Advertising Fund Its AI Ambitions?

Microsoft Preview: AI Must Prove It Is Worth the Massive CapEx

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.