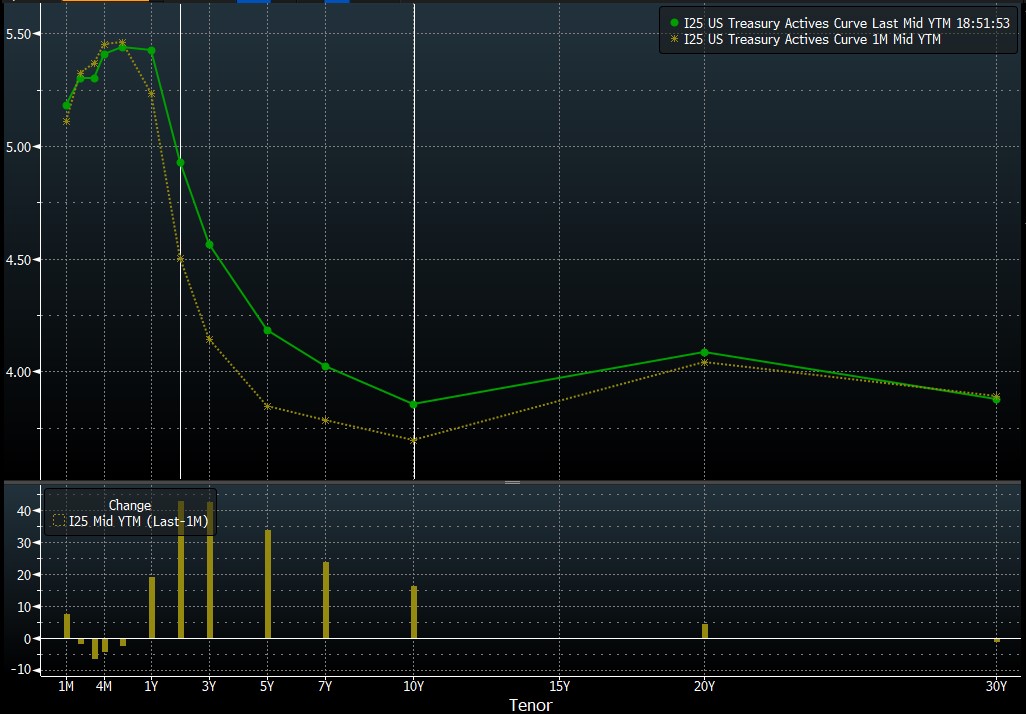

The yield curve in the US is experiencing increasing inversion. Today, a new local low was reached, slightly below -110 basis points. This is a result of the rising yields of 2-year Treasury bonds, while we also observe an increase in the yields of 10-year Treasury bonds. However, the increases in 2-year yields are significantly stronger. When considering the spread between the 10-year and 2-year yields along with interest rates in the US, we can observe pressure for further rate hikes to continue.

The spread between yields has entered a phase of further decline, forming an inverted yield curve. This development suggests similarities to movements observed in the late 1980s or around the year 2000. Source: Bloomberg, XTB.

A month ago, the yield curve was noticeably flatter, although it was still far from reaching positive levels. Despite significant movements in TNOTE (10-year bond prices), as seen on the chart above, it is evident that the magnitude of the movement was not as large as in the case of 2-year yields (which saw a monthly increase of 40 basis points). Source: Bloomberg.

TNOTE is currently at a critical level, supported by the 23.6% Fibonacci retracement level and the local low from December of last year. Additionally, it is near the lower boundary of an upward trend channel. A downside break could pave the way for a test of the 110.30-111.0 zone. On the other hand, last week saw the formation of a hammer or morning star pattern. However, for this formation to be validated, the declines from today's session would need to quickly reverse.

Source: xStation5

Although today we don't have much prospect for a trend reversal, and we also have limited trading volume in the next two sessions, there may be an opportunity for a potential reversal of this trend on Friday with the release of Non-Farm Payrolls (NFP) data. Of course, for this to happen, the NFP data would need to come out weak, which would neutralize the chances of further rate hikes. However, at the moment, a rate hike in July is highly probable.

Daily Summary: Equities rally on not-so-hawkish Fed and AI trade revival, Yen dominates FX, oil retreats (30.07.2026)

Unexpected FX intervention? USDJPY plummets more than 2%! 🇯🇵

BREAKING: US GDP below estimates! EURUSD struggles for direction!

BREAKING: BoE Keeps Rates Unchanged

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.