The confirmation of the partnership between the Swatch Group (UHR.CH) and the independent watchmaker Audemars Piguet marks one of the most unprecedented events in the modern history of the watchmaking industry. The collection, named “Royal Pop”, whose global launch is scheduled for 16 May 2026, has electrified not only horology enthusiasts but, above all, investors. The decision to merge a brand associated with the mass market with an elite manufacturer from the so-called “Holy Trinity” of luxury is a move with colossal implications for the entire sector. To fully understand the potential of this event and its possible impact on the Swiss conglomerate’s share price, it is necessary to analyse the fundamentals of both companies, their historical financial results and the structure of the product itself.

A Clash of Worlds: An Analysis of Swatch and Audemars Piguet

For those unfamiliar with the watch market on a day-to-day basis, the significance of this collaboration may be difficult to grasp without a proper understanding of the historical background of both companies. This is because we are dealing here with a merger of two radically different business models and manufacturing philosophies.

Audemars Piguet is synonymous with the very pinnacle of luxury. Founded in 1875 in the Swiss village of Le Brassus, this manufacture remains one of the few on the market to be entirely independent and controlled by the founding families. In the watchmaking industry, Audemars Piguet ranks alongside brands such as Patek Philippe and Vacheron Constantin. The most recognisable creation from this manufacturer is the Royal Oak model, unveiled in 1972. Designed by the legendary Gérald Genta, this timepiece – distinguished by an octagonal bezel inspired by a diver’s helmet, visible screws and an integrated steel bracelet – redefined the category of luxury sports watches. Prices for the base models in this line currently start at several tens of thousands of euros, and their supply is deliberately and strictly limited to around 50,000 pieces per year, creating multi-year waiting lists and generating substantial premiums on the secondary market.

At the other end of the spectrum is Swatch. This brand forms the cornerstone of the mighty Swatch Group and is widely regarded as the entity that, in the 1980s, saved the Swiss watch industry from collapse caused by the influx of cheap quartz watches from Asia. Swatch revolutionised the market by introducing affordable, colourful plastic watches, which became a pop-culture phenomenon and a canvas for artists such as Keith Haring. Today, the brand bases its business model on economies of scale, massive production volumes and innovative materials such as bioceramics. Swatch watches are widely available and aimed at a broad demographic, which is the complete opposite of Audemars Piguet’s elite strategy.

The pairing of a manufacturer at the pinnacle of the luxury market with a brand catering to the masses represents a marketing strategy with enormous commercial potential. For Swatch, this is an opportunity to boost sales and replicate the success of 2022, whilst for Audemars Piguet it is a bold yet controlled experiment aimed at exposing its historic design to a completely new, younger generation of consumers without the risk of permanently diluting the prestige of its flagship product.

Product Design and Format: Royal Pop as a Key Variable

Details regarding the final design of the AP x Swatch collection are closely guarded, but an analysis of the teaser campaign and historical product lines allows us to draw some significant conclusions. The name ‘Royal Pop’ itself is a hybrid, referencing on the one hand the iconic Royal Oak model, and on the other the Swatch POP line, which debuted on the market in 1986. The watches in the POP series were characterised by a modular design. Their chunky cases could be easily detached from standard straps and attached to clothing, collars or special chains, transforming the classic timepiece into a versatile fashion accessory.

From a market perspective, the ultimate commercial success of this project depends to a large extent on the form the watch will take. This variation gives rise to two main scenarios.

If the Royal Pop proves to be a faithful, bioceramic replica of the classic Royal Oak wristwatch, the Swatch Group can expect an immediate and unprecedented sales hit. Retaining the distinctive octagonal case with an integrated strap guarantees massive demand amongst millions of enthusiasts who have long dreamed of Genta’s design but do not have a budget exceeding thirty thousand euros. In this scenario, offering a substitute for the world’s most expensive sports watch at an anticipated price of around 300–500 US dollars (approximately 2,000 PLN) would trigger mass consumer hysteria, similar to that of 2022. Such an option is safe from a business perspective and would almost automatically translate into hundreds of millions of francs in additional revenue.

A completely different perspective emerges when we consider the promotional materials. Advertising posters and leaks from boutiques have shown colourful straps and fabric loops, strongly suggesting a return to the concept of a clip-on watch. Audemars Piguet has a history of creating exclusive Royal Oak-shaped pocket watches, such as the 5961 reference from the 1980s.

Source: Audemars Piguet Archives

If the new collection takes the form of a pocket watch or a designer pendant, the market may react with considerably more caution. Traditional customers looking for a cheaper alternative for the wrist may feel disappointed by the lack of wrist-worn functionality. Variations that deviate directly from the classic way of wearing them carry a higher sales risk in the initial phase. It should be noted, however, that in 2025–2026, the luxury goods and street fashion market was dominated by collectable toys and gadgets, such as the popular Pop Mart Labubu figurines. Competing for a place on the wrist is becoming increasingly difficult in the era of the global expansion of smartwatches, but entering the segment of exclusive wrist charms sidesteps this problem and perfectly appeals to the tastes of Generation Z.

Regardless of the chosen format, there are strong indications that the watch will be powered by a mechanical movement rather than a quartz one.

Source: Swatch website

The use of an automatic movement, combined with a pop art aesthetic, further enhances the product’s perceived value and explains the higher estimated retail price compared to previous collaborations. The colour scheme and pop-culture flair, also evident on the official packaging, confirm the desire to reach a completely new audience.

Source: Swatch website

Business Background and Financial Results of the Swatch Group

To answer the question of why the Swatch Group took such a radical step, one must conduct a dispassionate analysis of its financial health. Reports published for 2024 and 2025 exposed the structural weaknesses of this powerful conglomerate, which was immediately reflected in drastic falls in its stock market valuation.

In 2022, largely thanks to the success of the MoonSwatch collection, the group posted excellent results, generating net sales of 7.49 billion Swiss francs with an outstanding operating margin of 15.5 per cent. Unfortunately, the following years brought a sharp slowdown. The close of 2025 revealed a decline in net revenue to 6.28 billion Swiss francs, representing a fall of almost six per cent in nominal terms. The main damage to the balance sheet was caused by a fall in demand in the Asian region, particularly in China, combined with the negative impact of the strong Swiss franc on the conversion of foreign revenues.

However, the key issue turned out to be the operating profit of the entire conglomerate. It fell from over one billion Swiss francs in 2023 to just 135 million Swiss francs in 2025. The consolidated operating margin shrank dramatically to 2.1 per cent. Net profit amounted to a symbolic 25 million francs, which for a company with a market capitalisation of around nine billion is a highly unsatisfactory result. A breakdown of these figures shows that the watch sales segment itself performed quite well, generating an operating profit of 549 million francs in 2025. The manufacturing segment was largely responsible for the group’s disastrous performance. The management made a conscious and costly decision to maintain full production capacity and jobs at its Swiss factories, despite shrinking order volumes. This generated massive, inefficient fixed costs.

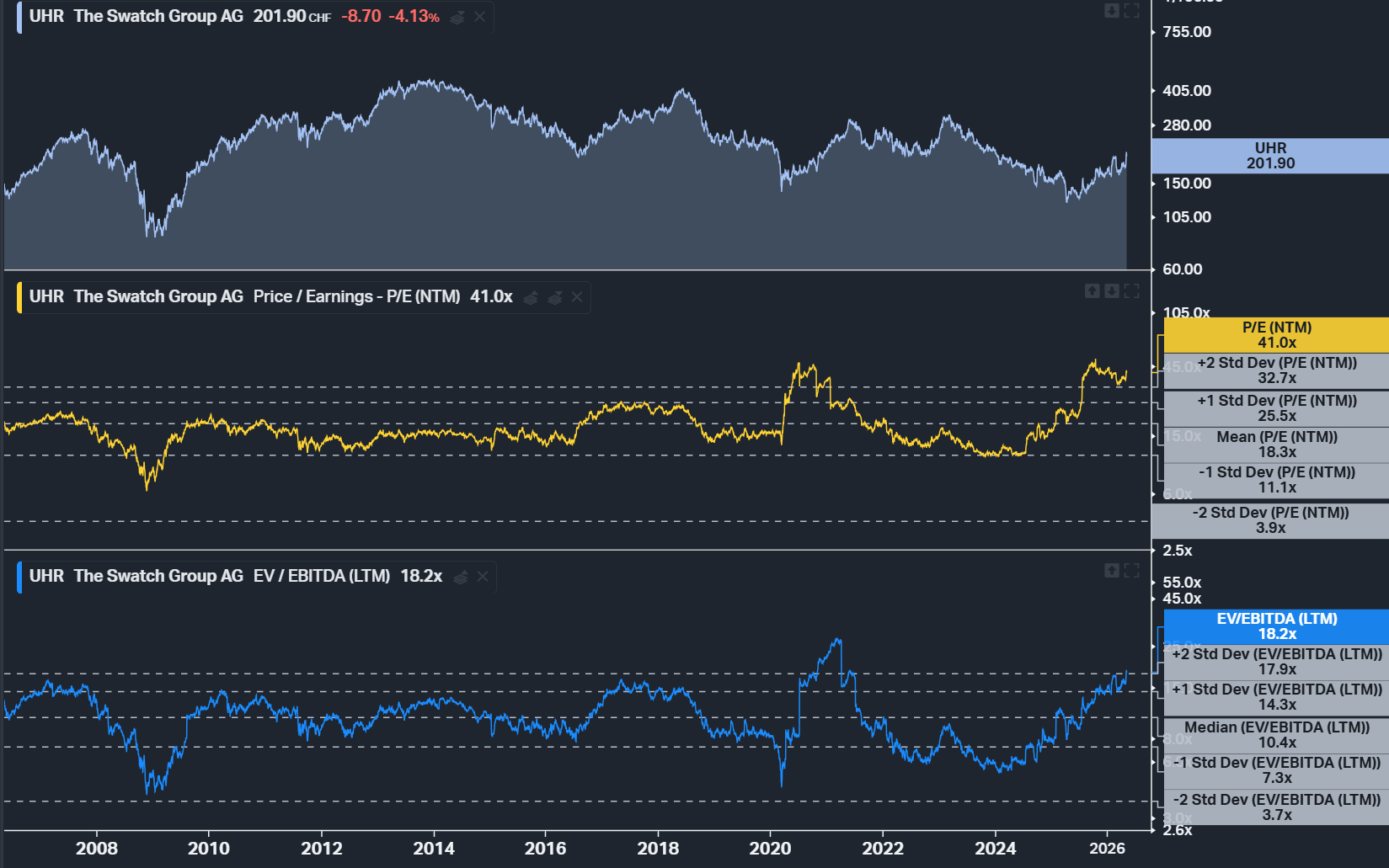

This situation caused a massive anomaly in the stock market’s indicators. The price-to-earnings ratio for the company listed under the ticker UHR.CH skyrocketed to unprecedented levels exceeding three thousand, which was a direct result of the mathematical collapse of the denominator, i.e. earnings per share. The company’s shares tumbled from the heights of the bull market and stabilised in the range of 180–210 Swiss francs.

The launch of the Royal Pop project is therefore a perfectly tailored rescue strategy. With spare production capacity, the Swatch Group’s factories can absorb the production of a mass-market hit at virtually no cost. If the new collection generates demand in the hundreds of thousands, the huge volumes will absorb the fixed costs weighing on the group. The company will thus activate powerful operational leverage, whereby each additional model sold, due to the very high gross margin, will contribute disproportionately to the net profit.

When viewed against its historical EV/EBITDA and P/E multiples, the company’s shares are currently trading at a significant premium to their average value. Source: Koyfin

The Impact of the Collaboration on Share Prices and Analysts’ Estimates

From a stock market perspective, the announcement of a partnership with an independent brand is part of a strategy to generate sudden spikes in demand. The financial markets’ reaction to such events is usually two-fold. Initially, we see short-term enthusiasm based on estimates and expectations. In the first few days following the announcement of the May teasers, Swatch Group shares reacted positively, rising locally to around 213 francs, which signalled the return of speculative capital.

Nevertheless, analysts at leading financial institutions such as Morgan Stanley and Citigroup are approaching these revelations with the requisite caution. They are maintaining neutral recommendations, setting average target prices of around 152 to 158 Swiss francs for the coming months. This is because even a highly profitable single product has limited power to offset negative macroeconomic trends in Asian markets, on which the Swatch Group has traditionally relied for a significant portion of its revenue.

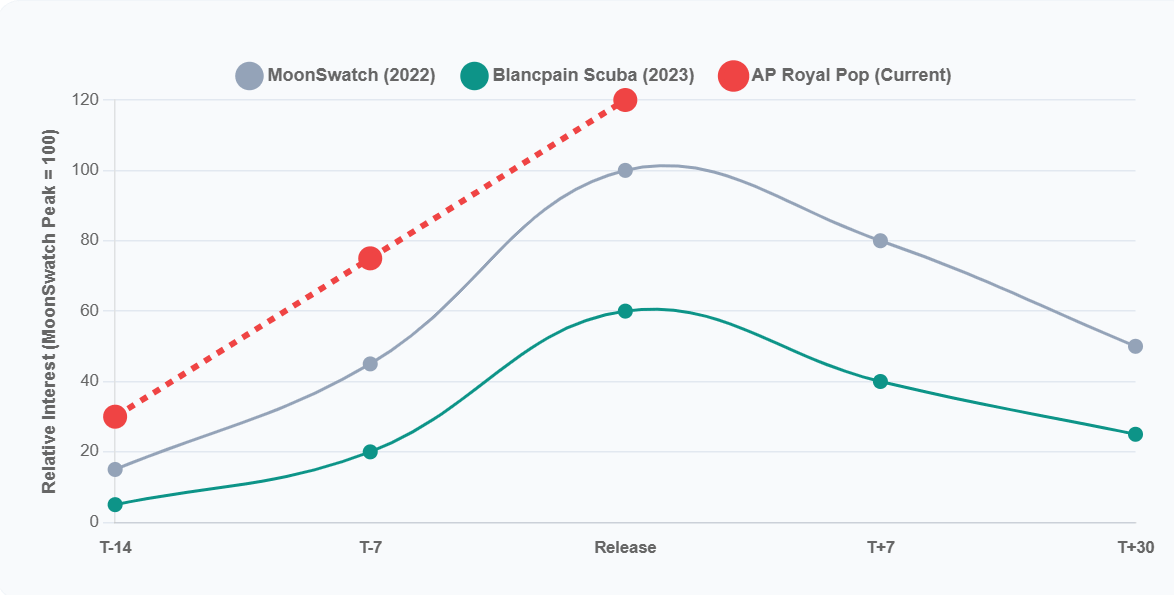

To properly assess the prospects for a sustained improvement in the company’s valuation, it is worth comparing the projected impact of Royal Pop with past collaborations. The visualisation below will help with this.

Table 1: Comparative Overview of the Swatch Group’s Key Collaborations

As the above analysis shows, the Royal Pop project possesses all the attributes needed to replicate the sales success of 2022, with the added advantage of a partnership with an external brand. MoonSwatch boosted short-term sales of original Omega watches by over fifty per cent. In the case of Audemars Piguet, such a strong sales effect for the partner’s classic watches will not occur, as AP operates under a strict supply rationing regime. This, however, works to the advantage of the Swatch Group, which focuses all consumer attention on its own boutiques.

Applying a limited distribution policy exclusively to high-street shops is another key element of excellent financial optimisation. By bypassing e-commerce channels, the company builds organic media coverage through images of huge queues, which serves as a free advertising equivalent. Furthermore, the direct-to-consumer model in its own retail outlets maximises margins by eliminating commissions for external distributors. Thousands of customers visiting physical stores who are unable to purchase the limited-edition model generate revenue through cross-selling, buying regular collections available on the shelves.

However, the secondary market is causing concern among investors. Initial estimates from prediction markets suggest substantial premiums for Royal Pop models, with transactions forecast to be well above the retail price. On the one hand, this demonstrates the product’s excellent positioning; on the other, it risks discouraging genuine customers through the mass activity of so-called ‘flippers’ and speculators, a phenomenon already observed in the late stages of the MoonSwatch model’s lifecycle.

The "Hype Life Cycle" index is a normalised aggregation of global search queries from Google Trends, where a base value of 100 corresponds to the absolute peak in searches for the term "MoonSwatch" on the day of its launch. Source: Own analysis, Google Trends

The success of this venture depends on the management’s ability to carefully control the supply of goods to the market. Maintaining interest in the Royal Pop collection for the remainder of 2026 by introducing new colourways may be the only way to meet the management’s forecasts, which have announced a massive reduction in losses in the manufacturing segment and a return to high profitability this year. A surge in the share price will depend on confirmation in the forthcoming quarterly reports that this phenomenon is capable of permanently boosting the company’s operating cash flow, rather than being merely a one-off anomaly in the sales statistics.

Mateusz Czyżkowski

Financial Markets Analyst XTB

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.