Over the past few months, the narrative has been simple: artificial intelligence is the engine of growth, and companies investing billions in AI infrastructure are the sure-fire winners of the next decade. Tech giants have been competing to announce ever-larger capex budgets, chipmakers have been setting records, and valuations have been rising without regard for fundamentals. Tuesday’s trading session has dealt a brutal blow to this optimism – investors are now asking en masse a question that until now had fallen out of favour: when will this astronomical spending on AI actually translate into profits?

The immediate trigger was Monday’s crash in SpaceX shares (-17%), which, shortly after its high-profile IPO, sought fresh funding – a sign that even the most sought-after ‘new era’ companies need cash sooner than the market had expected. Today, SpaceX is rebounding slightly by around 1%, but the rest of the sector is being taught a harsh lesson. Chipmakers are at the centre of the sell-off: Micron is down over 8%, Intel nearly 7%, AMD and Qualcomm both over 5%, and the iShares Semiconductor ETF (SOXX) is plunging by almost 6% in pre-market trading. In Europe, Infineon is down 6.6%, ASML 6%, and STMicroelectronics over 7%. In Asia, the impact has been devastating – the KOSPI has fallen by 10% in its biggest one-day slump since March, dragged down by Samsung and SK Hynix, both down 12%.

Macroeconomic factors are actively fuelling the sell-off. The Fed, under its new chairman Kevin Warsh, is signalling a hawkish stance on inflation, and the markets are already pricing in a 50 bp rate rise by the end of the year. Yields on 2-year Treasuries have soared to 16-month highs (~4.19%), the dollar has strengthened to annual highs (USDIDX above 101), and gold is down 1.5% to ~$4,127. Brent crude has slipped below USD 76/bbl – under normal circumstances, this would be a positive signal for equities, but today nobody is celebrating, as attention is focused solely on what higher interest rates will do to the valuations of growth stocks.

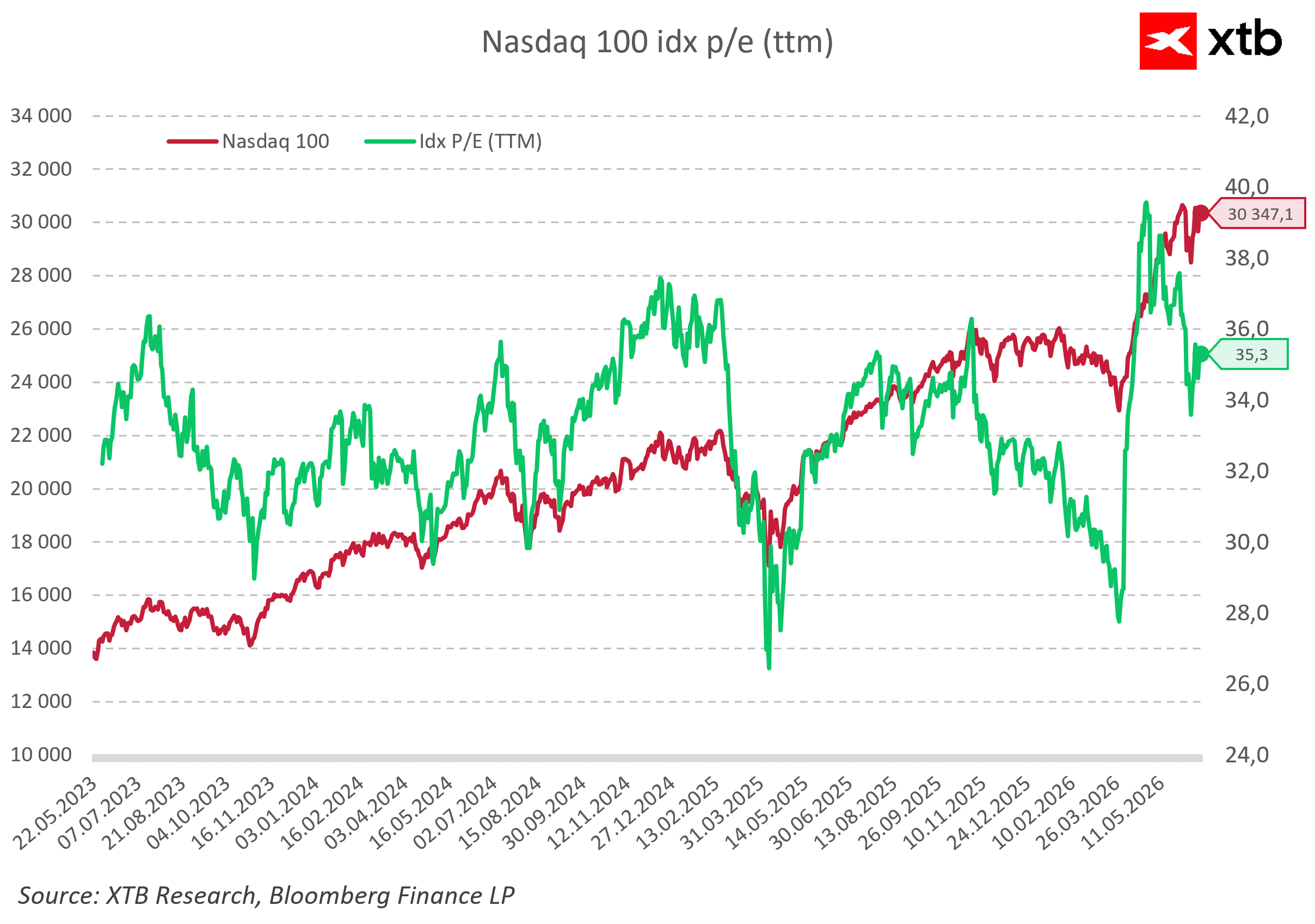

What about valuations? The Nasdaq 100 is currently trading at a P/E ratio (TTM) of around 35.3x – this is still well above historical averages, though a long way from the peak reading of 39–40x seen in May this year, when AI euphoria was at its height. In other words: valuations are elevated, but they are not yet at levels that in themselves scream ‘the bubble is bursting’ – rather, with bond yields on the rise, any wobble in the AI narrative is painfully testing the premium the market has paid for tech giants over recent months. Source: XTB

This table, showing the prices of the most important instruments, gives you a general idea of today’s volatility. Source: xStation

You can find more information on what is driving today’s trading session in our posts on the platform. ⬇️

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.