FIFA analysts announced that the World Cup, scheduled to take place in the USA and Mexico in mid-2026, is intended to be a catalyst for over $30 billion in economic activity.

These figures, regardless of how they are estimated, are based on the assumption that the USA (and Mexico) are awaiting a veritable flood of wealthy tourists. But will this actually happen?

In 2025, the USA was visited by 68.3 million tourists. This is a drop of approximately 6% compared to 2024 and a decrease of nearly 15% compared to the record set in 2018. For the US economy as a whole, this decline is not painful, as tourism accounts for only ~3% of US GDP. On the other hand, however, there are industries for which the condition of tourism in the USA is a matter of life and death.

Representatives of the hotel industry are already sounding the alarm about empty reservations. According to reports from "Forbes" and "The Independent," among others, as many as 80% of hoteliers complain that the level of reservations is significantly below expectations, and nearly 70% of respondents point out that guests face regulatory barriers. Industry representatives accuse FIFA of significantly overestimating the number of event participants. In Philadelphia alone, FIFA canceled reservations for 2,000 rooms without giving a reason.

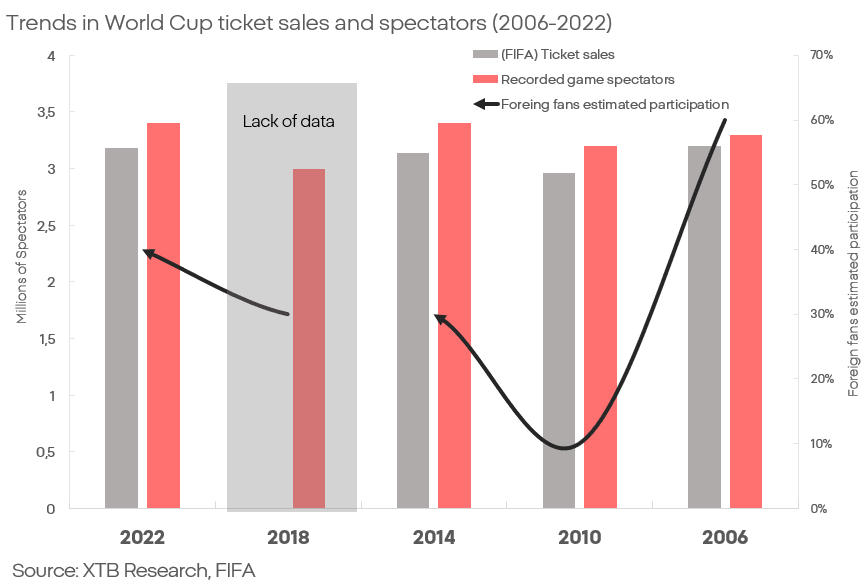

FIFA indicates that the number of tickets sold exceeded 5 million, more than in 2018 and 2022 combined. However, a significant factor is the record number of matches and teams. The organization itself suggests that the record attendance of 3.5 million spectators from the 1994 World Cup may or may not be broken, despite record ticket sales.

An analysis of previous World Cups shows that the share of visiting fans among the audience is less than half of the spectators in the stadiums. This means a smaller impact on global entities than might be expected, and local businesses benefit more. Furthermore, the number of tickets sold hovers slightly above 3 million. Sales above 5 million, as mentioned by FIFA, may mean a big surprise, both positive and negative, in terms of the number of fans.

This should not be a big surprise. Tourism in the USA is under pressure from a series of negative, structural trends in American society, government, and the economy, and this will be reflected in participation in sporting events.

However, in the context of disappointment regarding the attendance at the championships (or lack thereof), one must ask not only what the channels of influence of such an event on the markets are, but also: do the markets react to them at all?

Channels of Influence on Individual Industries

The World Cup is a unique event, with fairly clear directions of influence on individual industries. The fact that the championships will take place in the USA adds additional specificity.

- Airlines: North America is geographically separated from the main hubs of football fans, which are located in Europe and Latin America. Airlines must be the target mode of transport to the USA, Canada, and Mexico. In the context of 5 million tickets, even in such a large market, this will mean a significant increase in demand. However, the question arises whether this increase will translate into profits, given the difficult situation on the jet fuel market.

- Car Rental Companies: North American countries, especially the USA, are uniquely dependent on car transport, which will necessitate adaptation on the part of visiting fans. Obvious beneficiaries of this state of affairs will be car rental companies, but, as with airlines, problems are piling up. These entities are heavily indebted, their customers are also indebted, and the situation seems only to be getting worse.

- Hotels: One of the first concerns about the success of the World Cup is hotel occupancy. This is where the biggest surprise can be observed, but is it really? Global hotel chains are, as the name suggests, global. The World Cup will be limited to only 16 cities, and no scale of success or failure of this event will be able to significantly affect their results. When it comes to hotels listed by the few geographically concentrated REITs enough to feel the results of attendance, these entities are small, illiquid, and very few in number.

- Bookmakers: One of the few industries, apart from the technology and defense sectors, that is performing so fantastically in terms of profits (not always valuations), are companies related to sports betting. The trend in this sector is rather the result of the dismantling of regulations that were in force for many decades and the unleashing of suppressed demand, and not the influence of the sporting events themselves. However, a large temporal concentration of important matches may additionally support these companies.

- Apparel: For decades, the World Cup has been one of the main opportunities for sportswear manufacturers to promote their products. Theoretically, this is also a period when interest in this type of product should be greater, but theory is not enough for valuable conclusions. What do the data say?

The World Cup in Data and Forecasts

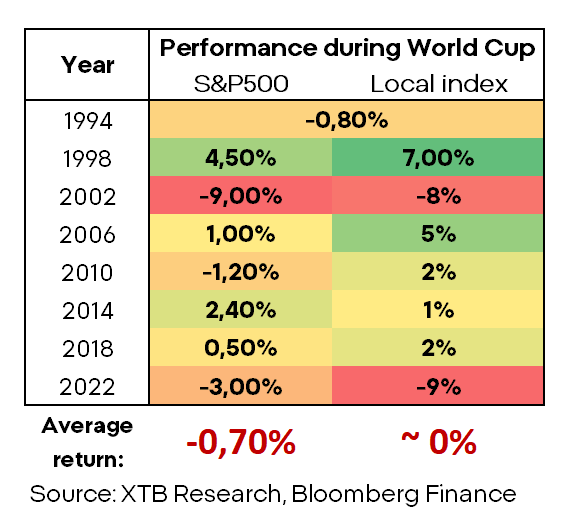

Before we proceed to formulating forecasts, it is worth getting acquainted with historical trends and precedents. Historical trends show quite eloquently that the connection between the World Cup and the behavior of major indices is more often than not - negligible.

Based on the behavior of the S&P 500 index and the main index of the host country, the average rate of return during the World Cup period is minimally negative. What is worth emphasizing: in the examined period of about 30 years, the main stock indices show a tendency toward relatively low volatility during June/July, when the championships are taking place.

In the context of a possible surprise, positive or negative, regarding the scale of the World Cups and the accompanying consumption, one must first determine: is there anyone to surprise and with what?

The FIFA organization announced that the World Cup will take place in the USA, Canada, and Mexico, during a conference in 2026. Were any upward revisions in expected results for 2026 for stock market entities related to the event registered during this period?

Among airlines and car rental companies, there is no qualitative data that would allow the conclusion that the market is actually expecting improved profitability due to the World Cup.

The situation is different for hotels. A number of analytical entities indicate that American hotels can count on an increase in revenue per available room (RevPAR) of 1.7% year-on-year and over 12% in the month of the tournament itself. However, it is important that studies by entities such as CoStar and Tourism Economics do not find full confirmation in the declarations of hotels such as Hilton, which already in February predicted that revenue growth would be smaller, not greater than expected.

Investment firms see a bullish thesis on the back of the World Cup for companies dealing with sportswear sales. According to Bernstein, Nike and Adidas may increase annual sales by an additional 4%. Reuters, in turn, reported that Adidas expects an additional 250 million euros in orders on the back of the World Cup. Goldman Sachs also pointed to Puma as a beneficiary.

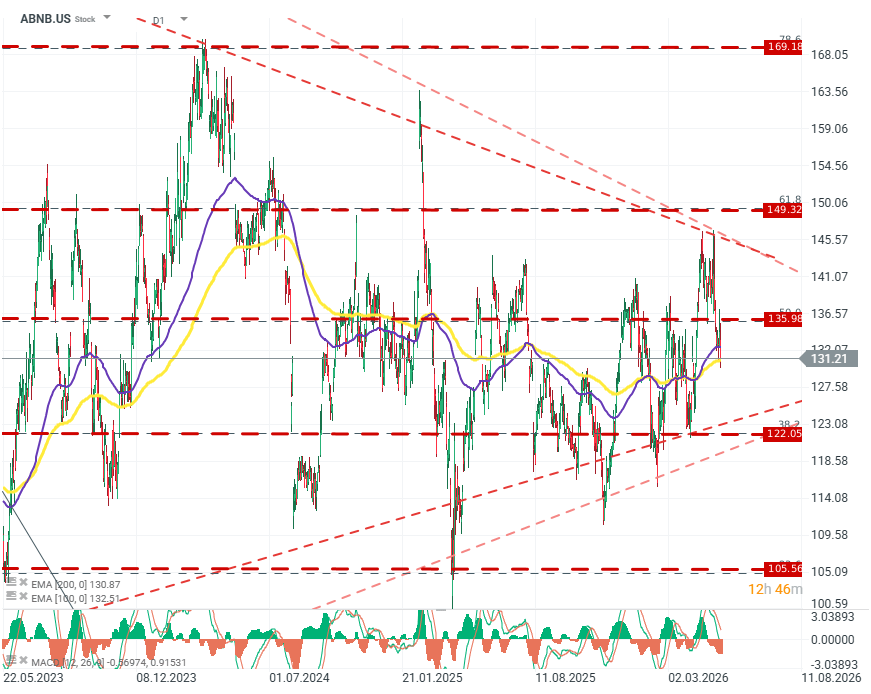

Two entities that did not play such a large role in previous World Cups, and which may turn out to be a "wild card" in market terms, are short-term rental companies and bookmakers. Airbnb secured official partnership with FIFA, and Deloitte sees an additional 380,000 guests due to the World Cup. Airbnb itself declares an 80% increase in inquiries in host cities, which may suggest real and measurable profits above current consensus – which may be particularly important in the context of a company that has had clear problems with profitability in recent quarters.

Two entities that didn't play such a significant role in previous World Cups, but which could prove to be a "wild card" in market terms, are short-term rental companies and bookmakers. Airbnb secured an official partnership with FIFA, and Deloitte predicts an additional 380,000 guests for the World Cup. Airbnb itself reports an 80% increase in enquiries in host cities, which could suggest real and measurable profits above current consensus - which could be particularly important for a company that has clearly struggled with profitability in recent quarters.

ABNB.US (D1)

The company is in a multi-year, narrowing consolidation channel. The market will soon be more willing to make decisions about the long-term trend for the company. The results from the World Cup period may prove crucial. Source: xStation5

The second class of entities are bookmakers, especially in the USA. Why?

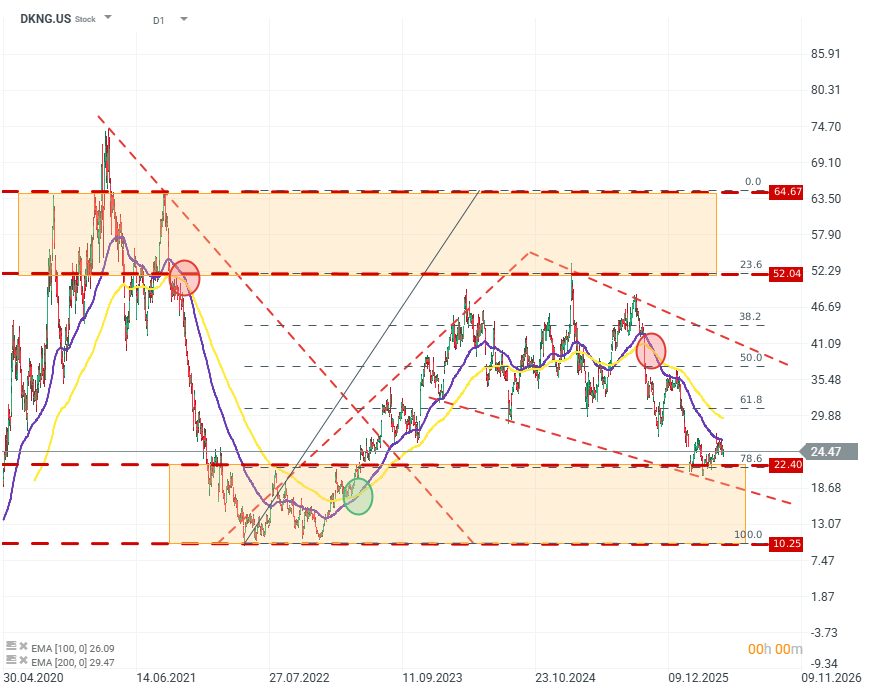

The support for their business model from one of the largest sporting events is obvious. What is less obvious, however, is that there is no good comparative basis, because the presence of these entities on the stock exchange was previously negligible. Sports betting and gambling is one of the fastest-growing industries on the wave of deregulation conducted by the new US administration, and a surprise in the results of these companies may (but does not have to) turn out to be large.

One of the entities for which the World Cup in the USA may prove to be a turning point is DraftKings. DraftKings is one of the leaders among bookmakers in the USA, and sentiment towards the company is still cool, partly due to high valuation multiples. There is no reason for pessimism on the financial data side. EPS only in Q1 2026 increased to $0.2, which is more than 5 times the forecasts. With double-digit revenue growth, a gross margin of around 76%, and strong momentum, the market may soon start to focus more on the company's strengths than its threats.

DKNG.US (D1)

The company's stock price has fallen to the lower limit of the long-term consolidation channel, and the defense of the FIBO 78.6 level is a potential place to build a base for the demand to try to take the initiative. Source: xStation5

Ultimately, despite its scale and real impact on the economy of even a large country, the World Cup's influence on financial markets will be limited, and many entities that should benefit from the influx of football fans to America may bring disappointment. At the same time, knowledge of the realities and operational advantages of selected entities and market niches may allow careful investors to profit.

Kamil Szczepański

Financial Market Analyst XTB

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)

Cocoa loses 4% amid news from Ghana 🚩 What's next for the market?

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.