- A legal “roadblock” for the White House: The Supreme Court has ruled unequivocally that the president cannot impose tariffs by invoking the International Emergency Economic Powers Act (IEEPA), because the power to levy taxes and tariffs belongs exclusively to Congress. This means that the broad “crisis” tariffs imposed so far have lost their legal basis, drastically limiting the president’s ability to rapidly and unrestrictedly manipulate global tariff levels.

- Billions of dollars in limbo: The ruling opens the door for importers (such as Walmart or Amazon) to recover as much as USD 180 billion, but the process will be an administrative nightmare. Companies have only 180 days to file a claim, and actual repayments may not occur for years due to disputes before the U.S. Court of International Trade—especially as the U.S. budget is grappling with a record deficit.

- The trade war continues under a new sign: Despite the court setback, the Trump administration quickly “switched” the tariffs to other legal authorities (Sections 122 and 301), raising the global rate to 15%. Although the new tariffs are temporary (a 150-day limit without congressional approval) and include numerous exemptions (e.g., pharmaceuticals or energy), they demonstrate the government’s determination to continue protectionism, sustaining market uncertainty and fuelling a rise in gold prices.

- A legal “roadblock” for the White House: The Supreme Court has ruled unequivocally that the president cannot impose tariffs by invoking the International Emergency Economic Powers Act (IEEPA), because the power to levy taxes and tariffs belongs exclusively to Congress. This means that the broad “crisis” tariffs imposed so far have lost their legal basis, drastically limiting the president’s ability to rapidly and unrestrictedly manipulate global tariff levels.

- Billions of dollars in limbo: The ruling opens the door for importers (such as Walmart or Amazon) to recover as much as USD 180 billion, but the process will be an administrative nightmare. Companies have only 180 days to file a claim, and actual repayments may not occur for years due to disputes before the U.S. Court of International Trade—especially as the U.S. budget is grappling with a record deficit.

- The trade war continues under a new sign: Despite the court setback, the Trump administration quickly “switched” the tariffs to other legal authorities (Sections 122 and 301), raising the global rate to 15%. Although the new tariffs are temporary (a 150-day limit without congressional approval) and include numerous exemptions (e.g., pharmaceuticals or energy), they demonstrate the government’s determination to continue protectionism, sustaining market uncertainty and fuelling a rise in gold prices.

In short: The U.S. Supreme Court ruled on Donald Trump’s tariffs and found that the president overstepped his authority under the IEEPA. The Court stressed that this law allows the government, in emergencies, to regulate imports—but the decision does not order any tariff refunds. The case is expected to go to the Court of International Trade (CIT), which would then refer it to U.S. Customs, where proceedings could drag on for years. Still, as much as $180 billion in potential refunds is at stake. Companies have 180 days to file refund claims. Trump first imposed temporary 10% tariffs and then raised them to 15%. Existing trade deals negotiated by Trump remain in force, but the U.S. can no longer collect tariffs under the IEEPA.

What actually happened — the core of the Supreme Court’s decision

In August 2025, importers asked a federal court to block the tariffs. The court found the tariffs unlawful, but allowed them to continue being collected while the case proceeded. Donald Trump then sought a definitive ruling from the U.S. Supreme Court. Trump had imposed the tariffs under the IEEPA (International Emergency Economic Powers Act). On February 20, the Supreme Court ruled 6–3 that IEEPA does not authorize the president to impose tariffs; that authority belongs to Congress. IEEPA only allows the executive to “regulate imports.”

Key points the Supreme Court made:

- IEEPA is not a tariff statute: it does not mention “tariffs” or “duties” anywhere.

- When Congress wants to allow presidential tariffs, it says so explicitly in other statutes—using clear tariff language—and it also sets limits (rate/level, scope, duration).

- The president tried to derive an unlimited power to impose tariffs of any amount, for any period, and on any scope. The Court said: such a delegation would require an unmistakably clear authorization from Congress—and it’s not there.

- Tariffs are part of the taxing power, which the Constitution assigns to Congress. You cannot transfer that power to the president through a vague word like “regulate.”

- Historically, tariffs have been treated as a form of tax, which demands particularly clear statutory authorization.

- “Regulating imports” means tools like embargoes, quotas, licensing regimes—not imposing a tax.

- Some justices emphasized the president must point to a clear and specific congressional authorization and a specific emergency basis.

The decision means the president did not have legal authority to impose tariffs under IEEPA, so those broad, elevated tariffs (on Canada, Mexico, and effectively the wider world) lack a legal basis and cannot be collected under IEEPA. This mainly concerns sweeping, general tariffs, not necessarily every tariff measure issued under other, more explicit trade statutes.

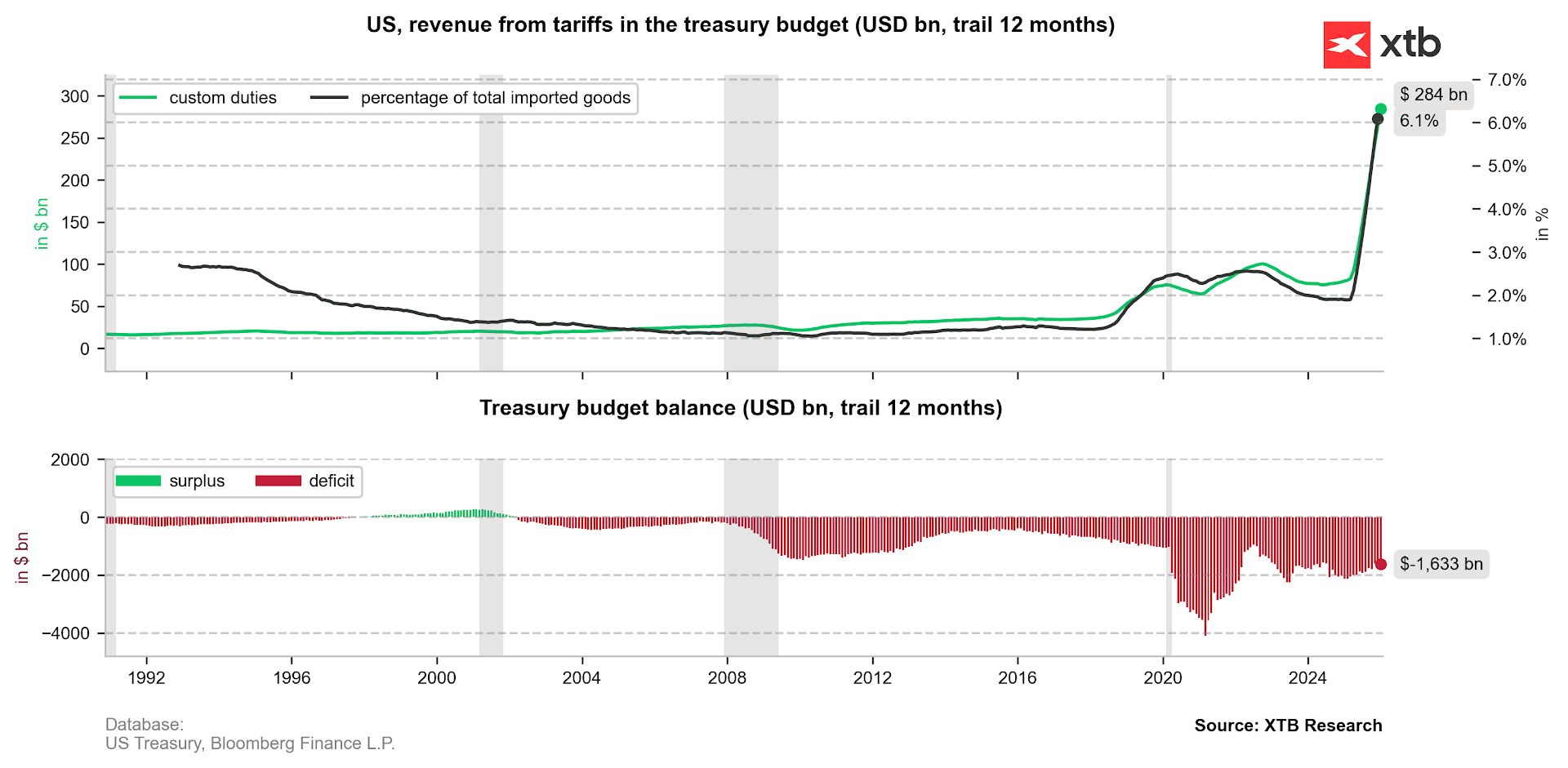

Despite Donald Trump’s new tariffs, the U.S. budget deficit remains very high. However, the amount of money collected through tariffs has increased sharply. The figure of USD 284 billion refers to the last 12 months for which data were available and covers all tariffs collected—not only those imposed under the IEEPA.

Source: Bloomberg Finance LP, XTB.

Although the importance of tariffs has increased, they still remain a relatively small source of revenue when compared with other government income streams. Source: Bloomberg Finance LP, XTB.

The dissent: what did the minority want?

The three dissenting justices (Thomas, Kavanaugh, Alito) supported Trump’s position, arguing that:

- Historically, presidents have had broad discretion in trade and sanctions policy.

- The phrase “regulate importation” can be read broadly, including the use of tariffs as a regulatory tool.

- They criticized applying the “major questions” doctrine in foreign-trade/foreign-affairs cases.

This matters because it highlights a fundamental disagreement over how aggressively courts should curb presidential power in economic and foreign policy.

What does the Supreme Court decision mean in practice?

Immediate effect: IEEPA is removed from the tariff toolkit

After this ruling, IEEPA can no longer serve as a legal basis for imposing tariffs. The president previously claimed he could impose tariffs on any country, at any rate, for an unlimited time under an “emergency” rationale. Now, without direct congressional authorization, he cannot. For this president and future presidents, that means:

- Tariffs must be imposed using the traditional trade statutes (especially the Trade Act tools such as Section 301, Section 232, etc.), or

- Congress must pass a new law (or explicitly grant special tariff authority).

Refunds: a massive administrative and legal mess

The Supreme Court did not resolve the issue of refunds, damages, or compensation. It did not create a mechanism and did not order repayments—effectively leaving the cleanup to lower courts and the administration.

Next steps are expected to be:

- The case goes to the Court of International Trade (CIT).

- CIT will likely push implementation details to Customs and Border Protection (CBP), which would have to design refund procedures.

Likely problems for the administration include:

- Who gets the refund: the importer of record, or the party that ultimately bore the cost (consumers, distributors)?

- How to prove who bore the economic burden of the tariff (e.g., whether it was passed through via prices).

- The process could take months or years, especially given operational strains within DHS (CBP sits within DHS).

Working around the ruling: Trump launches a new trade fight under different statutes

Signs suggest the administration was prepared for this outcome, given how quickly it acted.

In parallel to the IEEPA dispute, the Trump administration:

- Began implementing 10% across-the-board import tariffs under Section 122 of the Trade Act of 1974 (a provision that allows significant flexibility for temporary tariffs),

- Raised the rate to 15% over the weekend,

- Can keep these tariffs in place for up to 150 days without Congress (continuation beyond that would require congressional action),

- Intensified actions/investigations under Section 301 (retaliation against “unfair trade practices”),

- Continued using other classic trade instruments,

- While previously negotiated trade agreements remain in force, which may increase the likelihood of some congressional involvement or responses.

What options does Donald Trump have, and how quickly can he impose replacement tariffs?

Based on the administration’s actions, the Supreme Court ruling does not appear to mark the end of Trump’s strict trade policy. While Trump likely no longer has full freedom of action, he will probably try to pursue his agenda through other—potentially more complex—legal routes.

The current situation also sets the stage for multi‑year disputes over tariff refunds and over who is actually entitled to them. Even though markets reacted positively, in practice there are now more sources of uncertainty than before. It should also be emphasized that a trade war can be fought from both sides. New lawsuits are likely to emerge challenging the use of tariffs under Sections 122 and 301 of the Trade Act.

According to Bloomberg, using the new tariffs under Section 122 of the Trade Act could lead to even higher customs revenues—especially if previously negotiated trade agreements are not honored. Source: Bloomberg Economics.

The fight over refunds: who can get money back, and how much could it be?

Government sources do not provide a specific figure for how much was collected under the tariffs imposed pursuant to IEEPA. It’s important to note that Trump repeatedly changed course—introducing suspensions and adjusting rates—so the total is hard to pin down.

-

Estimates based on tariff-rate and country-level data (available on Wikipedia but reportedly confirmed by Bloomberg) suggest at least $130 billion. This seems conservative and is likely a lower bound.

-

Estimates from the Penn-Wharton Budget Model (cited by Reuters) indicate roughly $175 billion that could be subject to potential refunds.

At least $130 billion in tariffs was collected under IEEPA. Source: Bloomberg Finance LP, XTB.

The Supreme Court deliberately did not decide the refund issue. The IEEPA ruling itself was about 150 pages; if the Court had tried to calculate refund amounts and determine who should receive them, the decision could have taken years and run to thousands of pages. It is also important that the U.S. currently does not have the money for such refunds: despite substantial tariff revenue, the United States is running a record budget deficit (excluding the pandemic period).

Refund eligibility criteria (the procedure has not formally started yet)

- The company paid IEEPA-based tariffs (not other tariffs, e.g., under Sections 232/301).

- The company has documentation: an ACE (Automated Commercial Environment) entry summary and proof of payment of IEEPA duties.

- The entry is either liquidated (finalized by CBP) or unliquidated (not yet finalized).

- Importers have 180 days to file a protest with CBP, and then potentially a lawsuit in the Court of International Trade (CIT). Some companies reportedly filed protests even before the ruling was published.

Examples of companies affected:

- Large importers: Walmart, Target, Amazon (e-commerce; China/EU exposure), Home Depot.

- Mid-sized firms: electronics, apparel, toys, imported-food businesses (e.g., importers sourcing from China, the EU, Mexico).

- Small businesses: any registered importer that brought in goods subject to IEEPA tariffs (e.g., from India or Brazil).

- Scale: potentially hundreds of thousands of firms, because IEEPA covered global imports (all countries, with exceptions tied to USMCA). By December 2025, CBP had collected about $133 billion from importers.

- Roughly 60% of Trump-era tariffs are estimated to be IEEPA-linked (around $175 billion in potential refunds).

CBP will most likely announce a special refund program, similar to the Harbor Maintenance process. However, it remains unclear how refunds will be settled and who will ultimately receive them. Another open question is whether refunds could be taxed as income.

Which tariffs remain in force?

- Section 232 tariffs (steel, aluminum, copper, cars, timber, some furniture, etc.).

- Section 301 tariffs (primarily against China—IP and subsidies—but potentially other countries where investigations were completed). The U.S. also wants to apply these tools toward Mexico and Canada (hostile actions).

- All “standard” tariffs: WTO MFN duties, plus anti-dumping and countervailing duties.

- A new global tariff: 10%, raised to 15%, on almost all imports, based on Section 122 of the Trade Act of 1974—currently temporary (up to 150 days without Congress).

- A key date is July 24, when 150 days will have passed since February 24 (the start date for the 15% rate). In theory, Congress could extend these new rates—hence the political importance of the midterm elections for Trump.

- USMCA-covered goods from Canada and Mexico are excluded from the new global tariff, but rates on certain commodities and cars still apply.

For importers in practice:

-

The IEEPA route disappears, but high tariff levels remain, rebuilt via other statutes (232, 301, 122).

-

The real change is the legal basis and the refund risk for the IEEPA period—not a sudden return to a “tariff-free” era.

It is also worth noting that trade arrangements reached with the EU, Japan, the UK, South Korea, Vietnam, and Taiwan opened many markets for the United States, while those countries allegedly received little in return. So far, only the EU has demanded more clarity on tariffs but still intends to respect the deal. As a result, some zero-rate treatment for U.S. goods, lack of retaliation, market-opening measures, and commitments for large purchases of energy and agricultural commodities remain in place.

What does this mean for markets?

Strong gold, weaker dollar

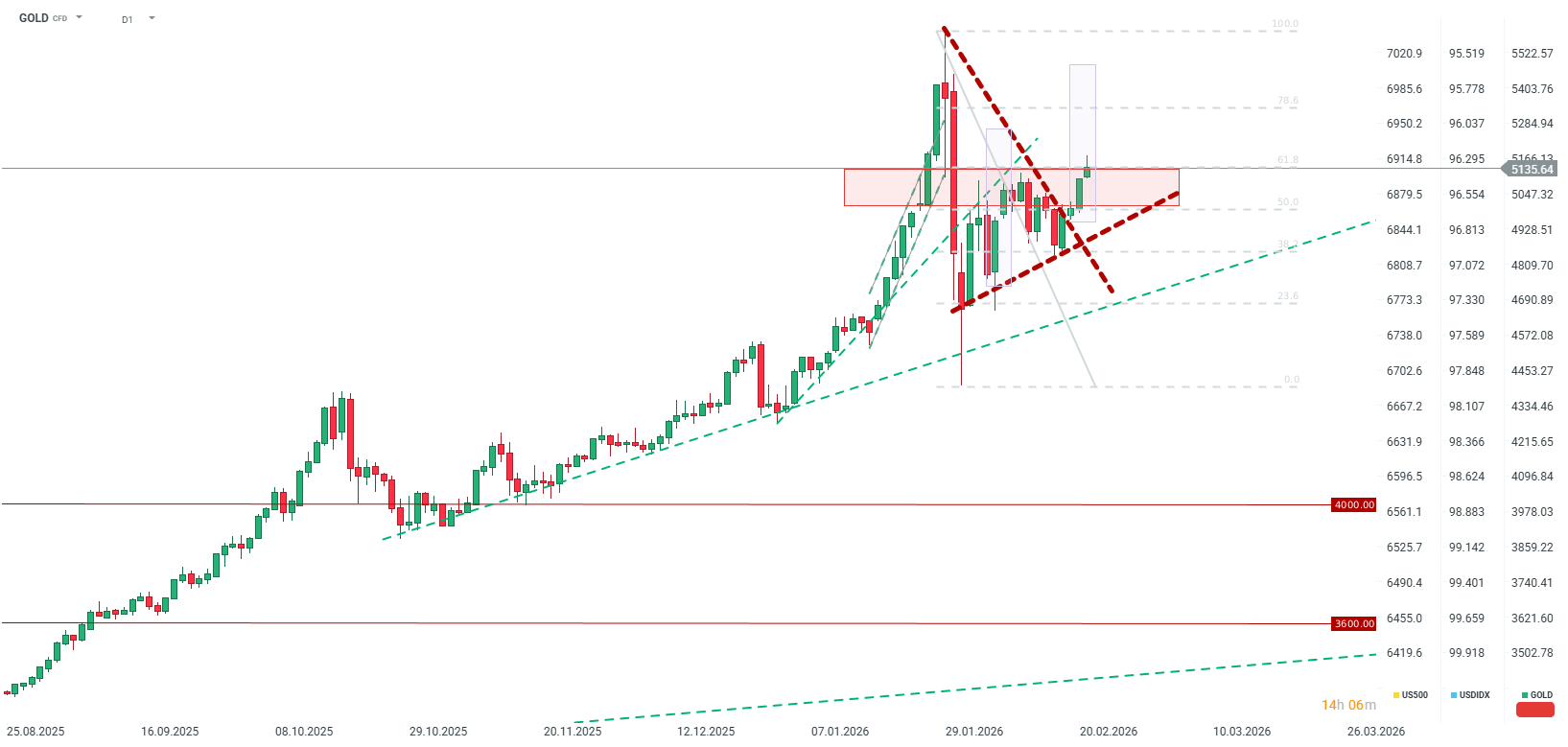

Trump’s trade policy was supposed to strengthen the U.S. dollar to offset the impact of new tariffs. Instead, the dollar has weakened amid major uncertainty about the next steps by U.S. authorities and gradual diversification away from the dollar as the dominant reserve currency. The dollar will remain central to reserves and global trade, but diversification—especially toward gold—has become more visible. The additional tariff uncertainty could push gold toward new all-time highs. Trade uncertainty and reduced appetite for the dollar were among the most important drivers behind gold’s rally in 2025.

Trade uncertainty, coupled with geopolitical uncertainty, has pushed gold out of its triangle formation. Currently, gold is trading at its highest level since the turn of January and February. Source: xStation5.

FX market

European currencies are highly sensitive to how international trade affects pricing. Although most currencies strengthened against the U.S. dollar after the Supreme Court decision was announced, the moves were not large.

It is also worth noting that despite the ruling, the overall level of tariff rates is unlikely to change materially—and customs collections could even increase. Under the new framework, China appears to be a relative winner, although some tariffs remain in place. On the other hand, the UK looks like a loser, as the effective rate could rise to 15% from the previously negotiated 10%. Moreover, the rate for the EU could also be slightly higher if the broader trade agreement is challenged or undermined (including sector-specific exemptions).

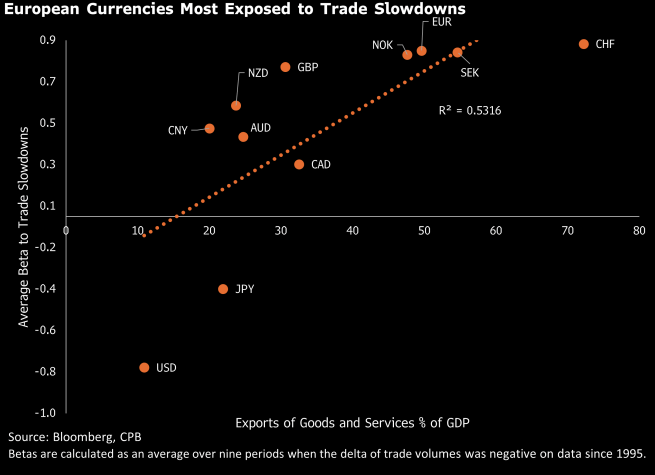

The euro, the Swedish krona, the Norwegian krone, and also the Swiss franc are highly exposed to trade slowdowns—although CHF also reacts as a safe-haven currency. Source: Bloomberg Finance LP.

Will European companies benefit?

A potential freeze of the EU–U.S. trade agreement could lead to a marginal increase in tariff rates. On the other hand, lower tariffs on Chinese products in the U.S. could redirect part of Europe’s export flow back toward the U.S. This, in turn, could make European products more attractive again in the domestic market.

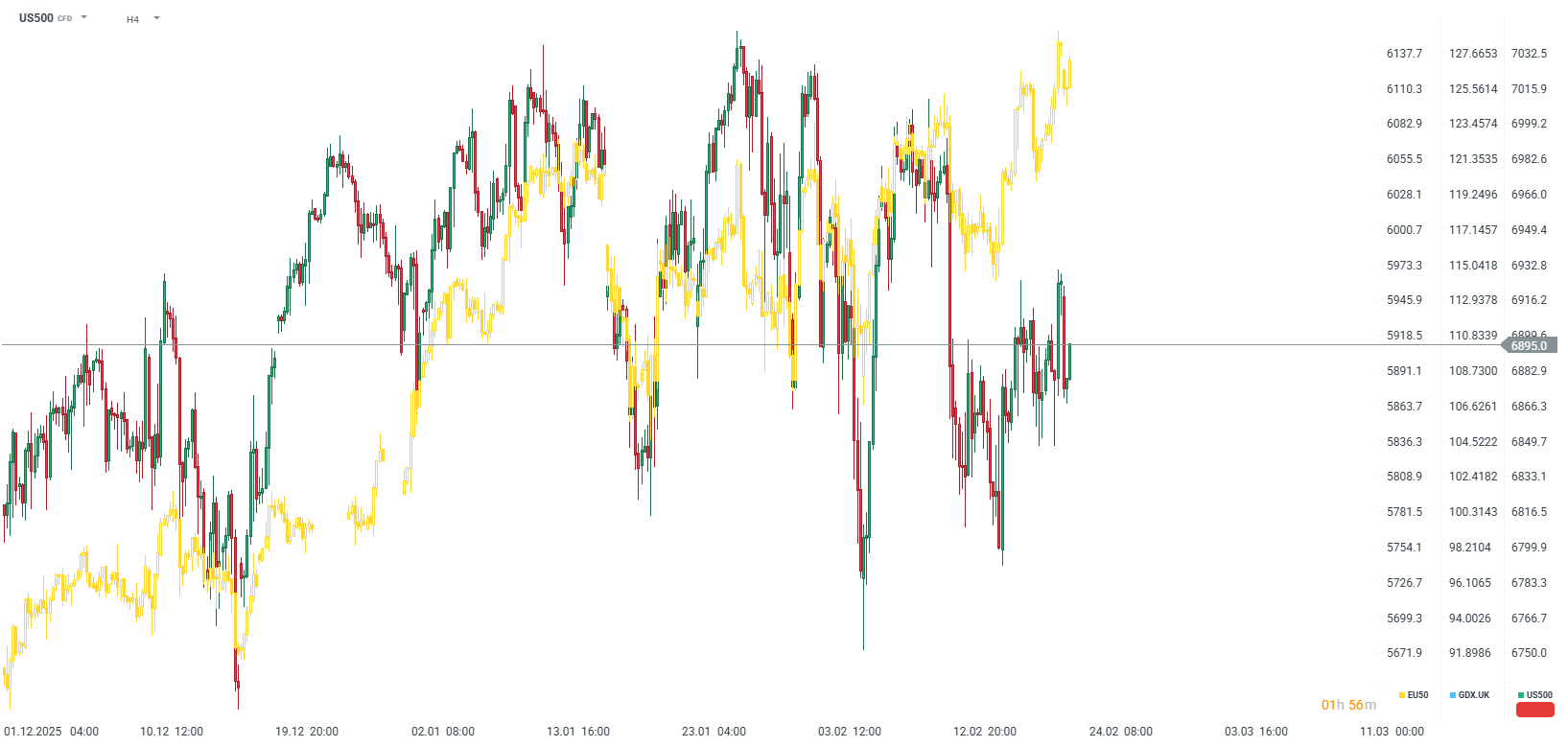

It is worth noting that European stocks have continued to outperform U.S. stocks since the start of the year, although trading at Monday’s open began with the Euro Stoxx 50 down.

The EU50 index is up year-to-date, while the US500 is showing almost no change (close to flat).

Source: xStation5.

Three markets to watch next week (07.08.2026)

Chart of the Day: What will drive the US stock market? (07.08.2026)

Morning Wrap: Oil Rises Again (07.08.2026)

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.