Wall Street extends yesterday’s gains after a stronger-than-expected US retail sales report eased concerns over consumer spending. The surprise reading helped counter fears of stagnation, adding to evidence that the US economy remains resilient despite elevated interest rates and persistent trade uncertainty.

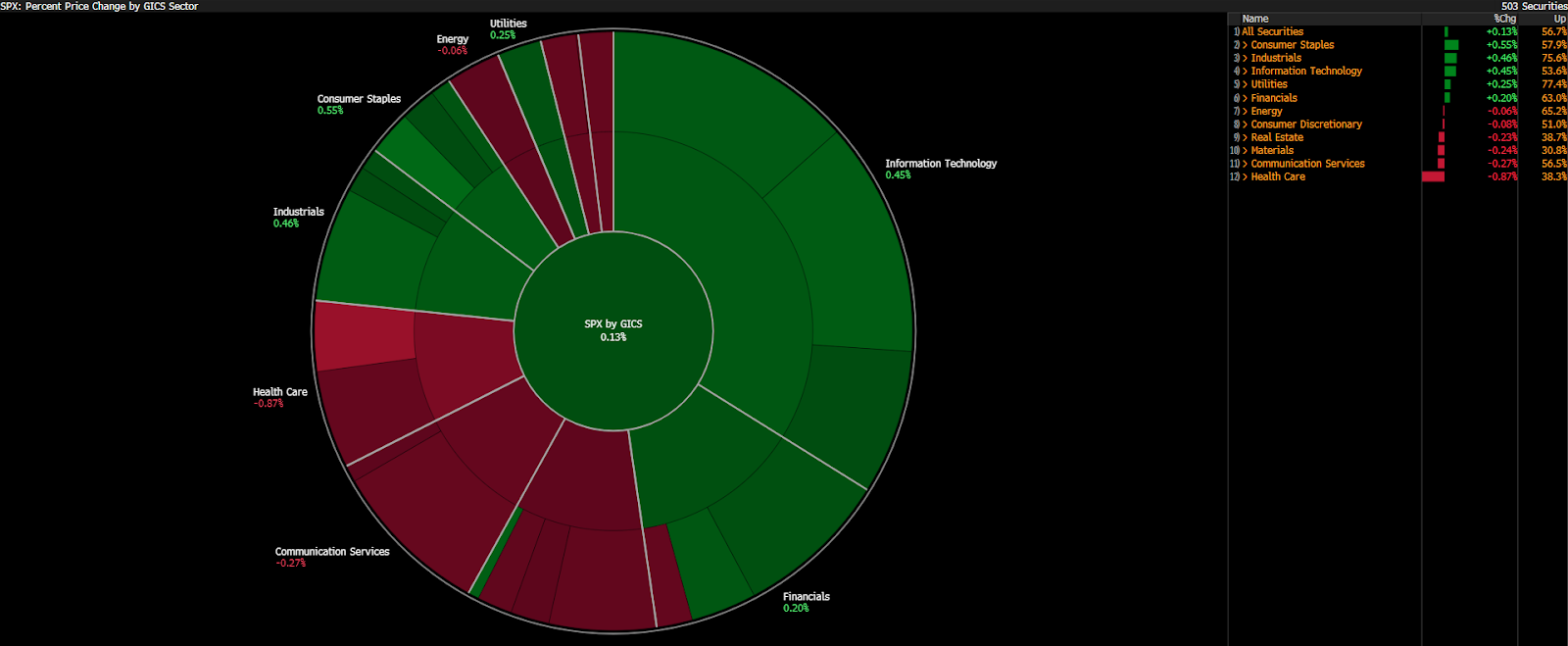

All of the major US indices are trading in the green. S&P 500 is up 0.3%, driven mostly by industrial and consumer staple sectors, benefiting from a positive sentiment after strong earnings from General Electric and PepsiCO. Dow Jones also rose 0.3%, Nasdaq 100 futures added 0.4%, staying only 0.3% away from the all-time, intraday record high around 23,220. Russell 2000 is up 0.9%.

Volatility in S&P 500 sectors. Source: Bloomberg Finance LP

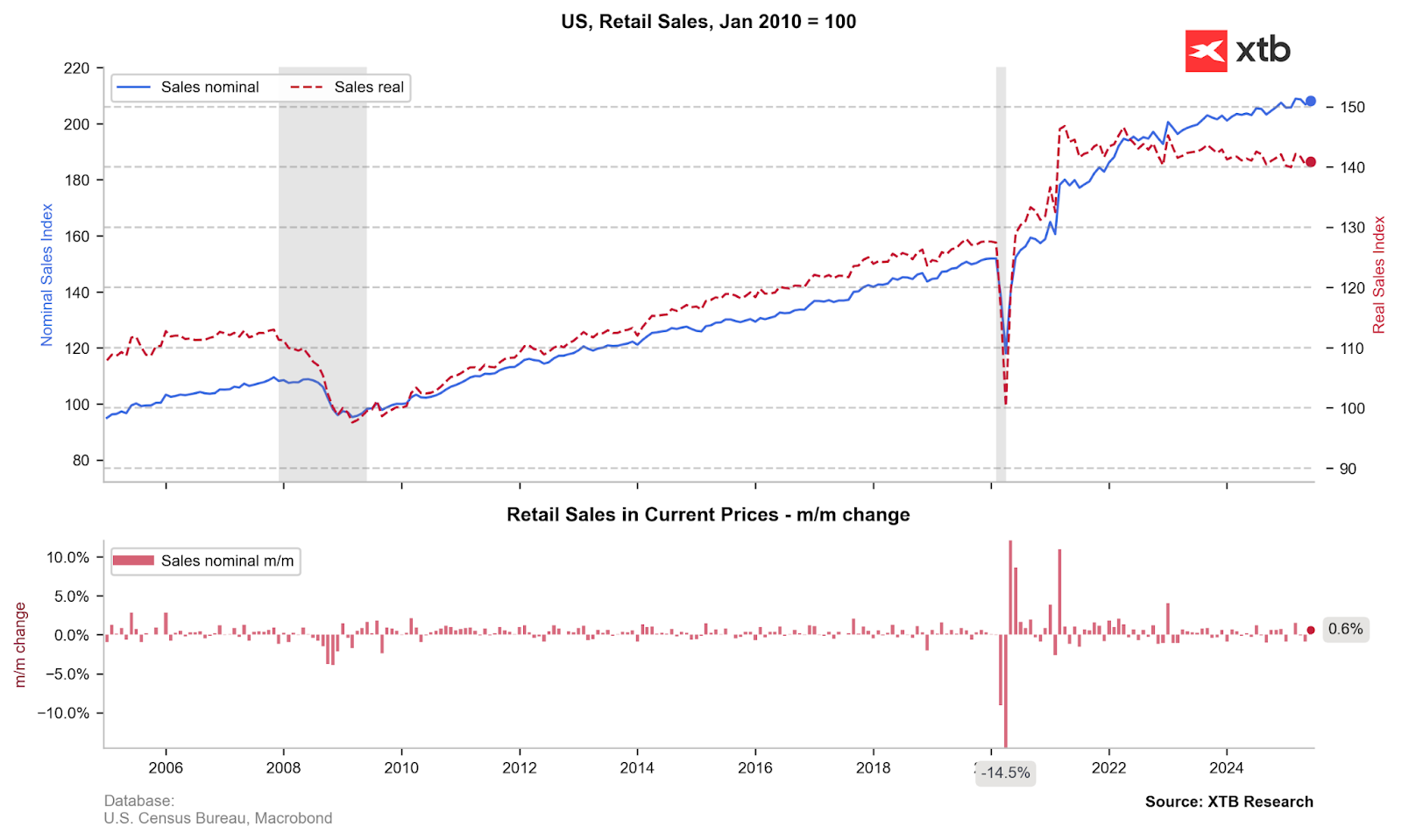

US retail sales rose 0.6% in June, beating forecasts and rebounding from May’s drop. Auto sales led gains with a 1.2% jump, while restaurants and bars rose 0.6%, signaling resilient discretionary demand. The control group climbed 0.5%, suggesting solid core spending. Discount and warehouse retailers outperformed, driven by bargain-hunting, while apparel and footwear lagged. Despite tariffs nudging prices higher, the strong labor market and job growth are keeping consumer wallets open — at least for now.

Source: XTB Research

US500 (H1)

S&P 500 futures are paring early gains after finding support near the 24-hour EMA (light purple). The uptrend remains intact, with the contract trading above both key moving averages. However, resistance around 6330 (and nearby record highs) may prove tough to break amid tariff uncertainty and upcoming tech earnings. Strong earnings beats could trigger a breakout to new highs, while disappointments risk a pullback toward the lower end of the current consolidation range.

Source: xStation5

Company news:

-

ADM (ADM.US) shares are down 2.3% after Trump said Coca-Cola will switch to cane sugar in US sodas. The move could hurt ADM’s corn-processing business, which produces high-fructose syrup. Analysts say a shift by Coke could boost sugar demand and leave corn in oversupply, weighing on ADM’s margins.

-

GE Aerospace (GE.US) raised its 2025 outlook, citing strong aviation demand and a 30% jump in commercial revenue. Q2 adjusted EPS of $1.66 beat forecasts ($1.43 est), with revenue at $10.2B vs. $9.6B expected. The company now sees FY EPS at $5.60–$5.80. Despite tariff risks, CEO Larry Culp remains optimistic, aided by cost controls and new deals like a major Qatar Airways engine order. Despite premarket gains, the stock is currently down 2%.

-

MP Materials (MP.US) shares trade flat after launching a $500m stock offering to fund operations, expand its 10X magnet facility, and pursue strategic growth. The raise follows a 69% surge in the stock over the past month.

-

PepsiCo (PEP.US) beat Q2 estimates, citing strong international growth, with organic sales up 2.1% and EPS at $2.12. The company maintained its 2025 outlook and highlighted improvements in North America. It flagged ongoing supply chain costs, including tariffs. Shares rose 6%, though they remain down around 10% YTD. Pepsi is also pushing healthier product options and expanding low/no sugar offerings to regain share.

-

Sarepta (SRPT.US) shares surged 16% after confirming its Elevidys gene therapy will stay on the market with a black box warning, despite recent patient deaths. The company also announced it will cut ~500 jobs and pause some drug programs, targeting $400m in annual savings. Investors welcomed both the cost-cutting and clarity on Elevidys, which accounted for over half of preliminary Q2 revenue of $513m.

Chart of the Day: What will drive the US stock market? (07.08.2026)

🔼 Silver surges 4%

Economic Calendar: Will NFP Move the Market? (07.08.2026)

Morning Wrap: Oil Rises Again (07.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.