-

Indices extend above recent all-time-highs

-

Major financial institutions pass Fed’s stress tests

-

Moderna flu shot success boosts combo vaccine hopes

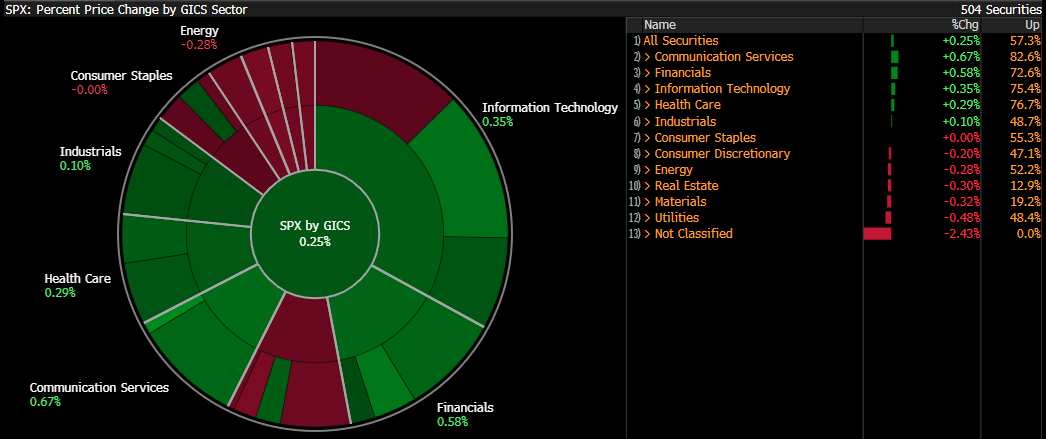

Wall Street begins the week with a great dose of optimism, with major indexes extending gains beyond recent all-time highs. Investor sentiment remains upbeat, driven by hopes for a swift de-escalation of tensions in the Middle East and communicated progress on trade agreements with key U.S. partners. The S&P 500 and Nasdaq are up 0.25%, while the Dow Jones and Russell 2000 each gain 0.3%.

New week opens on a high note primarily for the financial institutions. US banks rallied after passing the Federal Reserve’s stress tests, clearing the way for increased buybacks and dividends. Wells Fargo, Goldman Sachs, Bank of America, JPMorgan, Morgan Stanley, and Citigroup all gained in early trading. Analysts view the results as very positive, expecting lower capital buffers and higher shareholder payouts, with Goldman Sachs and Wells Fargo seen as key beneficiaries.

Volatility within S&P 500 sectors. Source: Bloomberg Finance LP

US500 (H1)

S&P 500 futures extended gains beyond Friday’s all-time high, supported by positive developments in trade negotiations and dovish expectations for U.S. monetary policy. Sellers attempted to fade the rally but were contained at the 24-hour EMA (light purple). The RSI remains comfortably below overbought territory, suggesting room for further upside—barring unexpected macroeconomic or geopolitical shocks. However, disappointment over post-July trade talks outcomes or prolonged negotiations could dampen sentiment and trigger a potential correction.

Source: xStation5

Company news:

-

Boeing (BA.US): The UK’s CMA has launched an antitrust review of Boeing’s $4.7B acquisition of Spirit AeroSystems, part of an $8.3B total deal including debt. A decision on a deeper probe is due by August 28. The deal would reunite Boeing with its former unit, a major supplier for the 737 and 787 jets. The planemaker’s stock falls 1.5%.

-

GMS (GMS.US): shares surged nearly 12% after Home Depot’s unit SRS Distribution agreed to acquire GMS for $110 per share, valuing the deal at about $4.3 billion equity and $5.5 billion enterprise. The deal, expected to close by fiscal 2025-end, will be cash- and debt-funded and is projected to boost adjusted EPS in the first year post-close.

-

HP Enterprise (HPE.US): The DOJ settled its antitrust lawsuit against HPE’s $13 billion Juniper acquisition, avoiding trial by requiring HPE to sell its Instant On wireless business and auction a license to Juniper’s Mist unit. The deal preserves competition while allowing the merger, which aims to boost AI-ready networking. This reflects a pragmatic DOJ approach to merger challenges. HPE’s stock is currently up 13%.

-

Moderna (MRNA.US): company’s experimental flu vaccine surpassed efficacy goals in a late-stage trial, showing 27% better protection than existing vaccines for adults 50+. This paves the way for a combined Covid-flu shot, potentially boosting vaccine uptake. Shares rose 7.4%. Moderna aims to file for approval of both standalone and combo vaccines next year, leveraging faster mRNA technology. The stock is up nearly 3.2%.

-

Oracle (ORCL.US): shares jumped 5.4% after revealing a cloud deal expected to generate over $30B in annual revenue starting FY2028. While the client remains unnamed, the deal highlights Oracle’s growing momentum in cloud and AI infrastructure. CEO Safra Catz noted database growth of 100%+ on rival clouds. The stock is up 26% YTD, near record highs.

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.