U.S. stock index futures remain higher ahead of the opening bell

U.S. stock index futures continue to trade higher, although they have surrendered part of the gains recorded immediately after the release of a weaker-than-expected U.S. June jobs report. The U.S. economy added just 57,000 jobs, well below the consensus forecast of 115,000, reinforcing expectations that the Federal Reserve may keep interest rates unchanged for longer. The yield on the 2-year U.S. Treasury declined following the report, providing additional support for equities. After Wednesday's sell-off, investors have returned to semiconductor stocks, with AMD, Intel, and Micron each gaining around 1% in pre-market trading. The stronger sentiment in the U.S. stands in contrast to the sharp sell-off in Asian technology stocks, where Samsung and SK Hynix posted steep declines.

Key takeaways

- U.S. labor market disappoints: Payrolls increased by just 57,000 versus expectations of 115,000, while the unemployment rate unexpectedly fell to 4.2%.

- Wall Street futures remain positive: Dow Jones futures are up 0.5%, S&P 500 futures gain 0.4%, and Nasdaq-100 futures advance 0.3%.

- Semiconductor stocks rebound: AMD, Intel, and Micron rise by around 1% after coming under pressure during Wednesday's session.

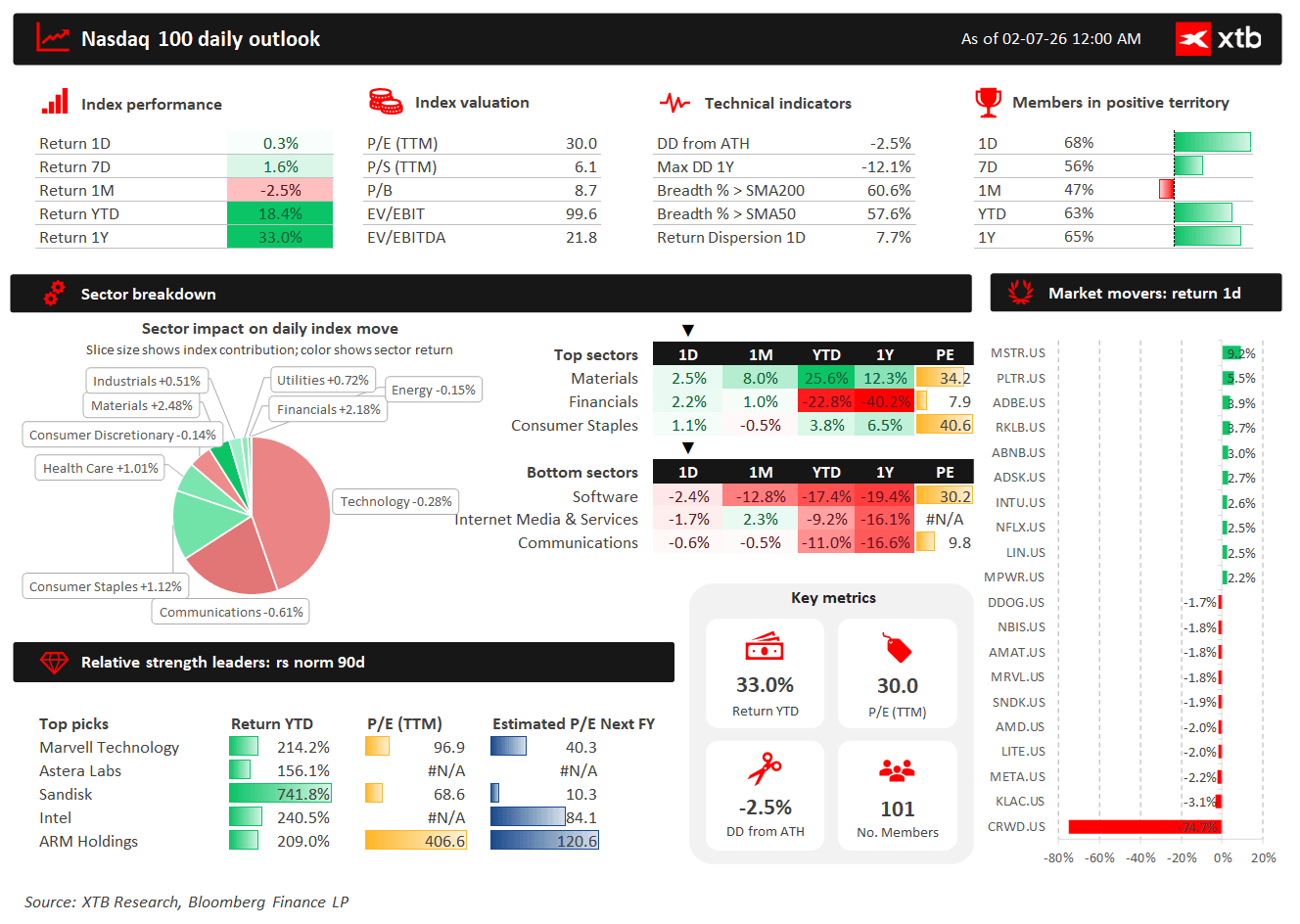

The Nasdaq 100 remains just 2.5% below its all-time high and is up 18.4% year-to-date, confirming that the longer-term bullish trend remains intact. However, the index continues to trade at a demanding valuation, with a P/E ratio of 30. Over recent sessions, materials, financials, and consumer staples have been the strongest-performing sectors, while technology and internet stocks have lagged. Market breadth also remains healthy, with more than 60% of Nasdaq 100 constituents trading above their 200-day moving average. Relative strength continues to be led by AI and semiconductor companies, including Marvell Technology, Arm Holdings, and Intel.

Source: XTB Research, Bloomberg Finance L.P.

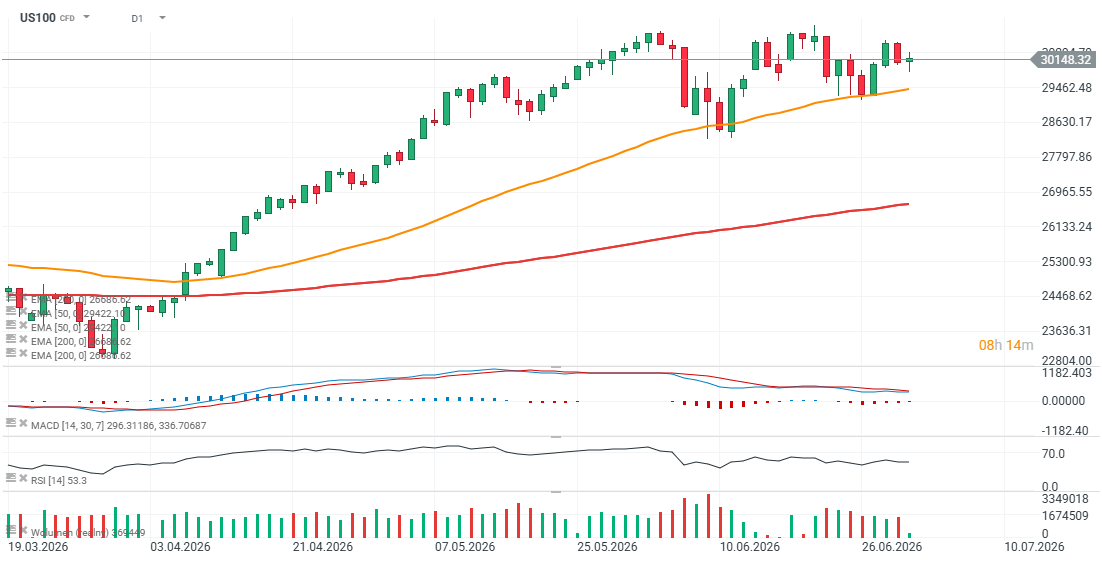

US100 Chart (D1)

Looking at the daily chart, the US100 futures contract continues to trade above the 50-day Exponential Moving Average (EMA50), shown by the orange line, indicating that bullish momentum remains dominant. The market is also forming a series of higher lows, reinforcing the prevailing uptrend. On the upside, 30,300 points remains an important resistance level, reflecting previous price reactions. Initial support can be found around 29,400 points.

Source: xStation 5

Company news

- Tesla (-1%) – Shares of the EV manufacturer are trading lower despite reporting stronger-than-expected second-quarter delivery results. Tesla delivered 480,126 vehicles, well above the consensus estimate of 406,600 and significantly higher than the 384,000 vehicles delivered in the same period last year.

- Alphabet (-1%) – Google's parent company is lower after a European court upheld a €4.1 billion ($4.67 billion) antitrust fine related to the company's practice of giving preferential treatment to its own applications within the Android ecosystem.

- Bending Spoons (-7%) – Shares of the Italian technology company are retreating following Wednesday's IPO debut. Despite today's decline, the stock remains roughly 40% above its IPO price.

- AeroVironment (+4%) – The defense technology company is higher after securing a $500 million U.S. Army contract to develop counter-drone capabilities.

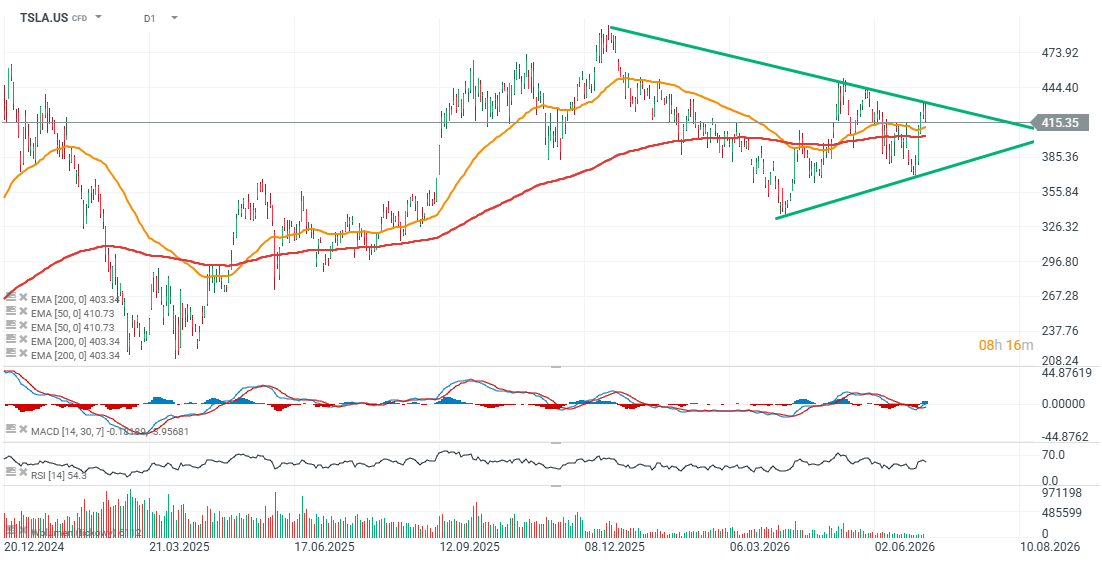

Tesla Chart (D1)

Tesla's daily chart shows a potential triangle formation. Unless the stock breaks above $425, the primary technical risk remains a downside breakout that could lead to a retest of the $390 support area. Conversely, a breakout above the upper boundary of the pattern could open the way toward $480, near the highs reached in 2025.

Source: xStation 5

Tesla surprises Wall Street as deliveries jump 25% and crush expectations

Tesla reported significantly stronger-than-expected vehicle delivery results for the second quarter of 2026, signaling that the company's prolonged sales slowdown may finally be coming to an end. The EV maker delivered 480,126 vehicles, far above Wall Street's consensus estimate of approximately 406,600. The results not only comfortably beat expectations but also marked a return to strong growth after two consecutive years of declining annual vehicle sales.

Key Q2 2026 figures

- Vehicle deliveries: 480,126 (consensus: 406,600)

- Vehicle production: 451,758

- Year-over-year delivery growth: +25%

- Quarter-over-quarter delivery growth: +34% versus Q1 2026

For comparison, Tesla delivered approximately 384,000 vehicles in the second quarter of last year, while first-quarter 2026 deliveries totaled 358,023 vehicles.

Model 3 and Model Y continue to dominate

Once again, the Model 3 sedan and Model Y SUV accounted for the vast majority of Tesla's deliveries.

Together, they represented 467,762 vehicles, or roughly 97% of total deliveries during the quarter.

Tesla does not disclose deliveries by region or individual model, but the figures clearly show that its lower-priced mass-market vehicles remain the company's primary growth driver.

Why were the results so strong?

The stronger-than-expected deliveries were likely driven by several factors:

- the launch of lower-priced versions of the Model 3 and Model Y,

- the rollout of Full Self-Driving (Supervised) in selected European markets,

- stronger demand for electric vehicles in Europe during the period of elevated fuel prices caused by the conflict with Iran.

At the same time, Tesla is attempting to recover after facing several headwinds over the past two years, including consumer backlash against Elon Musk, the expiration of U.S. federal EV tax credits, and intensifying competition from manufacturers such as BYD, Nio, Xiaomi, Hyundai, and Volkswagen.

Energy business also beats expectations

Tesla's Energy segment also delivered a positive surprise.

The company deployed 13.5 GWh of energy storage systems during the second quarter, exceeding analysts' expectations of 13.3 GWh and improving from 9.6 GWh a year earlier.

Additional support came from a transaction with SpaceX, which purchased $269 million worth of Tesla Megapack battery systems in April to power xAI's energy-intensive data centers.

What's next?

During the second half of the year, Tesla plans to focus on ramping production of several key projects:

- the autonomous Cybercab,

- the Tesla Semi electric truck,

- the Optimus humanoid robot.

The company has also announced that it will discontinue production of the Model S and Model X in order to repurpose manufacturing capacity at its Fremont factory for Optimus production.

What challenges remain?

Despite the strong delivery numbers, Tesla continues to face several important challenges:

- growing competition from Chinese EV manufacturers,

- weaker demand for fully electric vehicles in the United States, where consumers are increasingly choosing hybrid models,

- uncertainty surrounding inflation, trade policy, and rising costs of semiconductors and other key components.

Investors now turn their attention to earnings

While the delivery report has significantly improved investor sentiment, attention now shifts to Tesla's full second-quarter financial results, which the company is scheduled to release on July 22 after the close of Wall Street trading. Investors will be looking to see whether the sharp increase in deliveries also translated into stronger revenue growth, improved margins, and higher profitability.

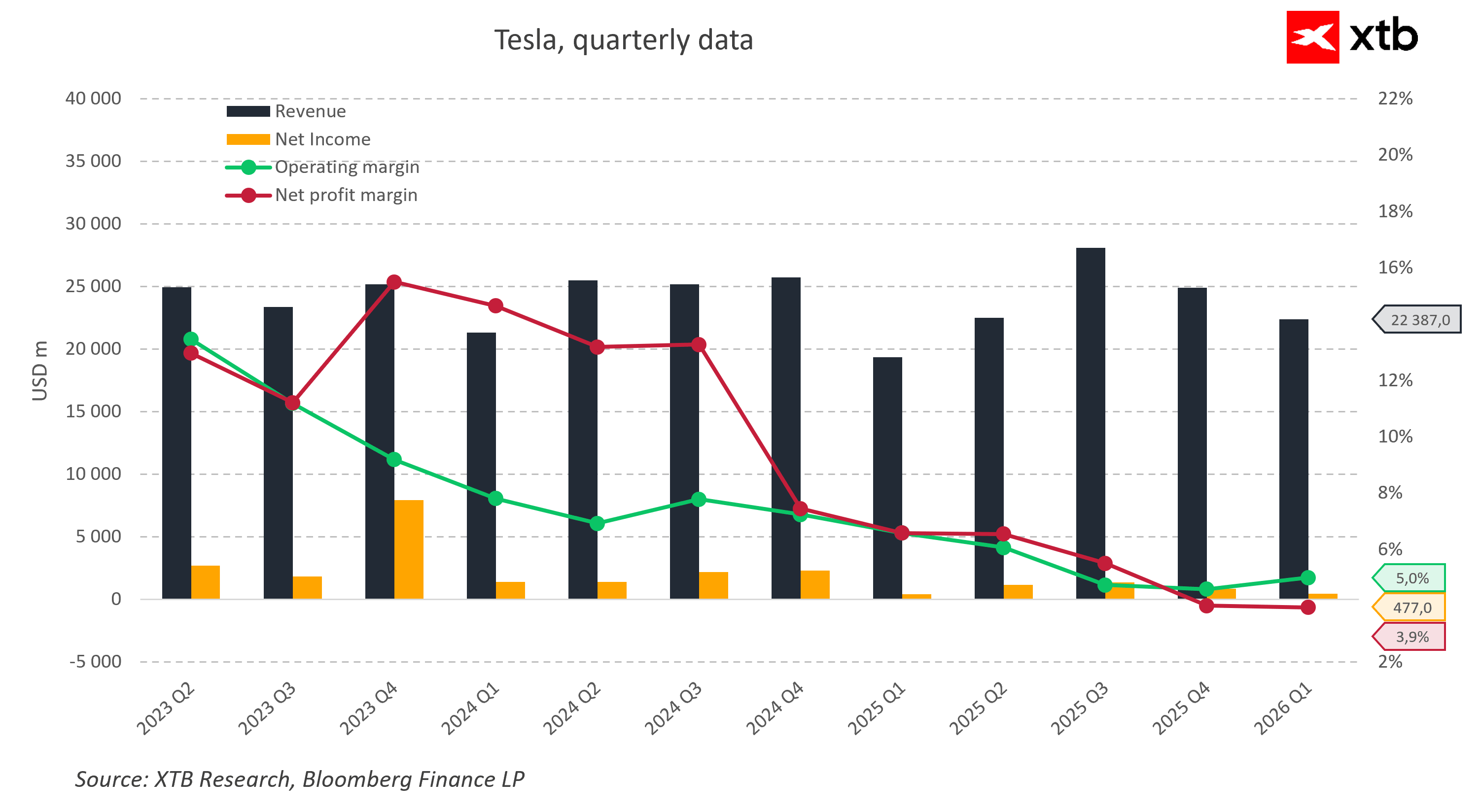

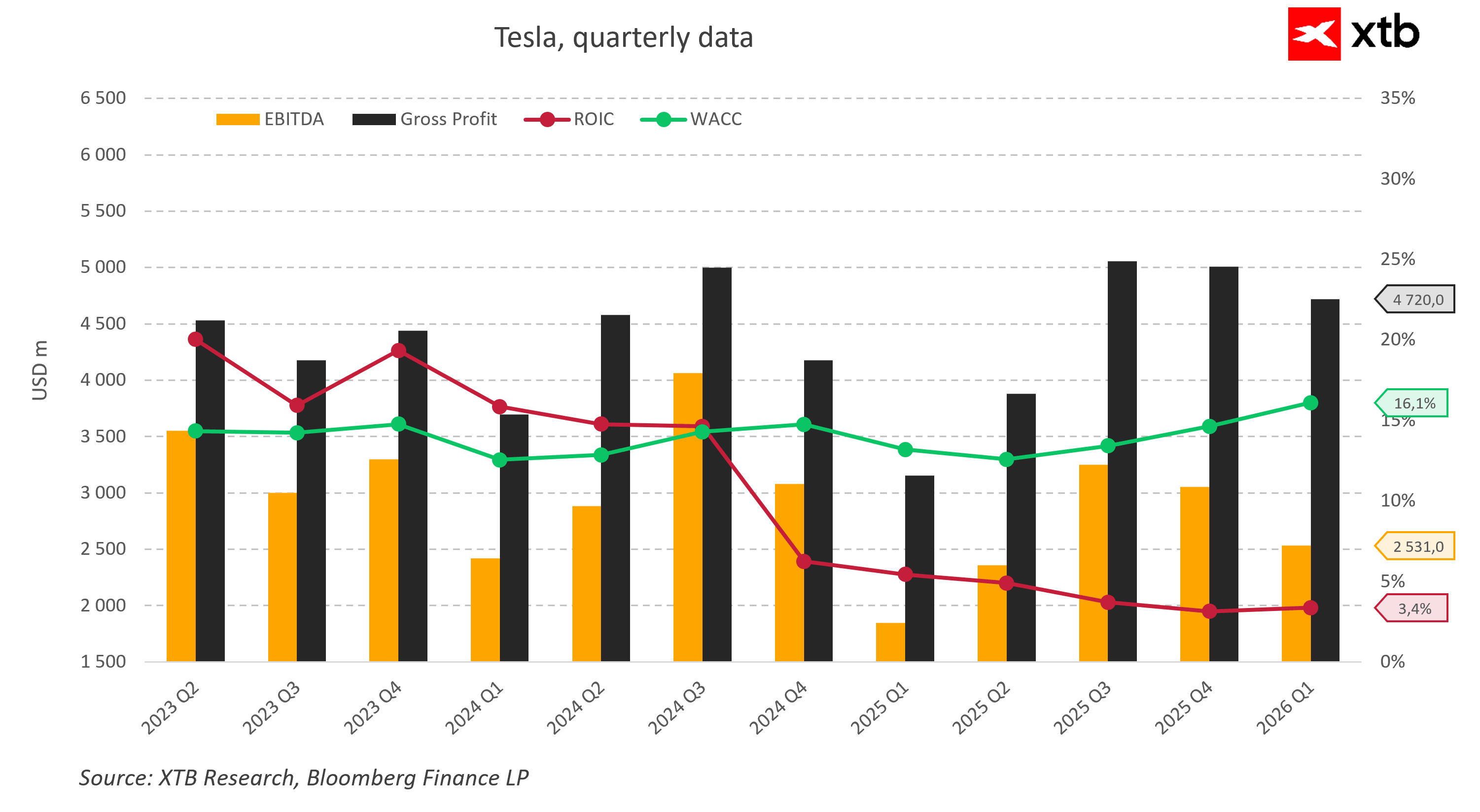

Tesla – Financial dashboards

The first chart shows that although Tesla continues to generate substantial revenue, its profitability has deteriorated significantly over the past two years. In the first quarter of 2026, revenue totaled approximately $22.4 billion, while net income fell to just $477 million. Operating margin recovered slightly to 5.0%, but net profit margin remained low at just 3.9%, well below the levels above 15% recorded at the end of 2023. This suggests that Tesla continues to face pricing pressure and rising costs driven by intensifying competition in the electric vehicle market. The upcoming second-quarter earnings report will show whether the much stronger-than-expected vehicle deliveries also translate into higher margins and improved profitability.

The second chart illustrates that Tesla's ability to generate returns on invested capital has weakened considerably over the past two years. In the first quarter of 2026, the company's ROIC declined to approximately 3.4%, while its weighted average cost of capital (WACC) increased to 16.1%, indicating that Tesla is currently generating returns well below its cost of capital. EBITDA declined to roughly $2.5 billion, while gross profit stood at approximately $4.7 billion, remaining below the levels recorded during the second half of 2025. Such a wide gap between ROIC and WACC highlights the continued pressure on profitability and capital efficiency. The stronger-than-expected second-quarter delivery figures will need to be reflected in improving profitability metrics to confirm a sustainable improvement in Tesla's underlying fundamentals.

Source: XTB Research

Alphabet and Tesla report earnings 🚩 Google's AI business shines, Tesla accelerates Optimus plans

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

All or nothing: ServiceNow earnings preview

Cocoa loses 5% amid rising inventories on ICE

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.