- US indices open significantly lower today due to the return of geopolitical risk aversion

- Donald Trump announces the end of the truce with Iran; Brent crude prices rise sharply for the second day in a row, adding over 3%. Brent crude is approaching $78 per barrel

- The tech sector continues its retreat from AI-linked companies, while Alibaba gains nearly 10%

- US indices open significantly lower today due to the return of geopolitical risk aversion

- Donald Trump announces the end of the truce with Iran; Brent crude prices rise sharply for the second day in a row, adding over 3%. Brent crude is approaching $78 per barrel

- The tech sector continues its retreat from AI-linked companies, while Alibaba gains nearly 10%

US equity markets begin today's cash session marked by a second consecutive strong sell-off and investor flight toward safe havens, including the US dollar. The main trigger for the declines were the unequivocal words of President Donald Trump spoken during the second day of the NATO summit in Ankara. Trump declared that the fragile ceasefire with Iran is "over" and described the negotiations as a "waste of time." In his latest words, Trump spoke of a possible further bombing during the coming night, pointing to a possible takeover of Kharg Island and an attack on desalination infrastructure. Furthermore, earlier the United States reinstated sanctions on Iranian oil exports after conducting an attack on 80 targets in Iran. This entire escalation by the US is a response to Iran's attack on three merchant ships, which was a blatant violation of the terms of the ceasefire memorandum.

It is worth remembering that the minutes from the last FOMC meeting will be published today at 8:00 PM. Although the importance of the minutes has decreased in recent years, now with a new chief and limited communication, the minutes may once again be an important event for the entire financial market.

Middle East Escalation and the Return of Inflation Fears

Donald Trump's comments immediately translated into commodities and debt markets. Brent crude contracts rose to $79 per barrel (highest since June 22), and the US WTI variety returned above the $75 barrier. The vision of renewed disruptions in the strategic Strait of Hormuz boosted inflation expectations, triggering a sudden jump in Treasury yields (US 10-year benchmarks rise to 4.57%, and 2-year to 4.22%).

The rise in market interest rates directly hits the valuations of stock indices, where a deepening of the ongoing capital rotation is visible.

- US500: S&P 500 index futures lose about 0.5% at the open, falling toward the 7,511 level. The broader market is buckling under the weight of concerns about higher energy costs.

- US100: The technological Nasdaq 100 loses slightly less at 0.25% in the 29,340 point region. This is an extension of the declines that yesterday were motivated by memory and chip manufacturers.

- US30: The Dow Jones index is performing worst, losing about 0.9%.

- US2000: The Russell 2000 small-cap index is under heavy pressure from rising bond yields, currently losing approximately 0.5% and reaching the 2,981 level.

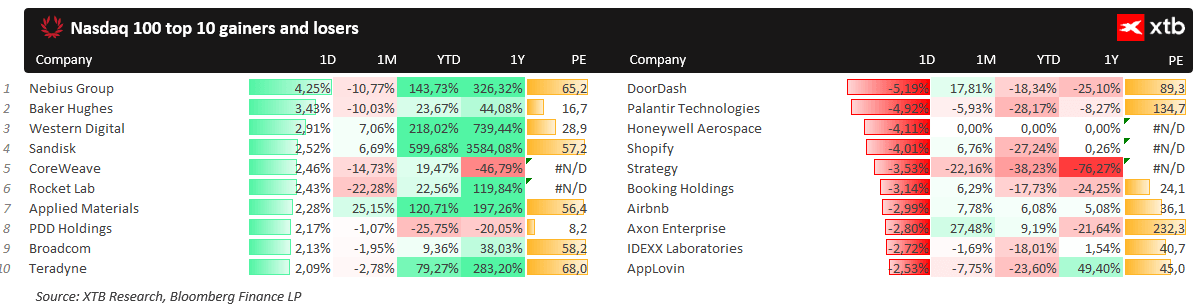

Despite the recent sell-off of the memory stocks, we can notice a little rebound in some crucial companies such as Western Digital and Sandisk. Source: Bloomberg Finance LP, XTB

Despite the recent sell-off of the memory stocks, we can notice a little rebound in some crucial companies such as Western Digital and Sandisk. Source: Bloomberg Finance LP, XTB

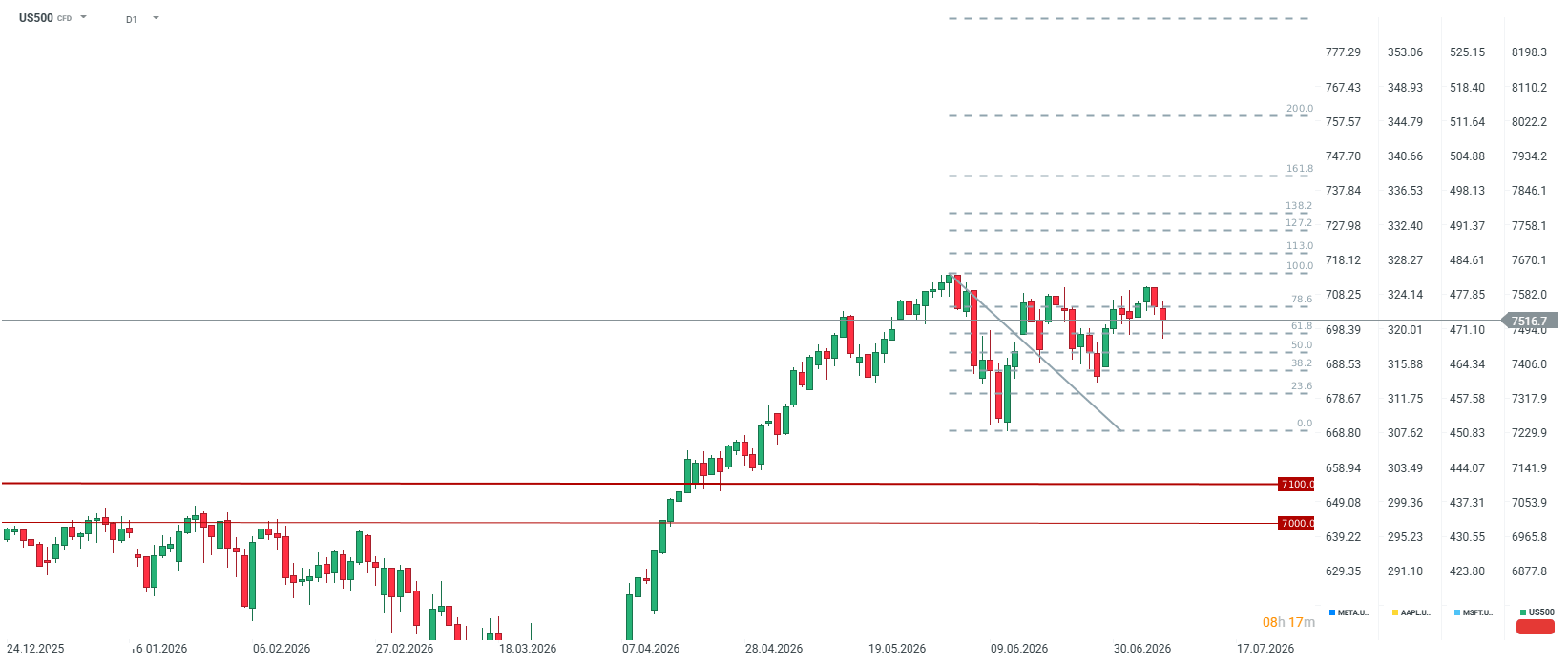

US500 Technical Analysis

After testing 7,600 points earlier this week, we are currently seeing a pullback to levels near 7,500 points. It is worth noting, however, that the start of the session is very volatile, as for a moment the declines reached the lowest levels since June 29. Currently, the key support level is the area of 7,400 points at the 38.2 retracement of the last downward wave. However, if a situation arises where the USA and Iran return to negotiations, current lows could serve as a buying opportunity, particularly for heavily oversold tech companies. It is worth noting that the US500 is only 1.5% from historical highs.

Most important company news from the session opening

- Energy sector attempts to grow: Rising oil prices fueled expectations for a strong session for oil producers. ExxonMobil (XOM.US) gained as much as 3% in pre-market trading, but is currently losing as much as 0.5% amid significant volatility in the oil market. It is worth noting that news emerged today that Exxon's Q2 profits were boosted by nearly $4 billion due to high oil prices during the Middle East conflict. It is up 3.0% on news that the conflict with Iran boosted second-quarter profits by nearly $4 billion. Chevron (CVX.US) is gaining 0.8%, and Occidental Petroleum (OXY.US) is up 1.7% following an upgrade by Evercore ISI to "outperform."

- Sell-off of chip and AI producers: Investors are fleeing crowded tech positions en masse. Nvidia (NVDA.US) is losing over 0.4% at the open, deepening an ongoing decline (shares are already 16% below the May peak). On the other hand, we are seeing a rebound in memory manufacturers after recent sharp declines. Sandisk (SNDK.US) is up nearly 4%, Micron (MU.US) is currently gaining 0.8% after falling as much as 6% in pre-market trading, and Western Digital (WDC.US) is also rebounding by 4%.

- Alibaba (BABA.US) leads gains: American ADRs for the Chinese e-commerce giant shot up 10% in pre-market trading, and these gains are currently continuing with shares reaching approximately $108. Optimism surrounding upcoming financial results triggered an influx of capital into large Chinese internet entities, with Baidu (BIDU.US) (+5.0%) and JD.com (JD.US) (+3.2%) also benefiting.

- Airlines and cruise companies under pressure from expensive fuel: The specter of higher operating costs is hitting entities sensitive to jet fuel prices. United Airlines (UAL.US) is losing 2.9%, and travel giant Carnival (CCL.US) is down 3.1%.

- FuelCell Energy (FCEL.US) dives to the bottom: The company's shares are falling 12% after officially pricing a new public offering of 10.7 million shares at $21.00 per share, representing a deep discount to recent market valuations.

France Challenges Palantir, Market Reacts.

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

ASML sell-out: Dreams and rumors will not break the monopoly

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.