American markets open slightly positive after the publication of weaker-than-expected labor market data. The ADP and Challenger Job Cuts reports confirm a significant cooling in employment. Futures on the S&P 500 and Nasdaq remain slightly positive, but investors are clearly waiting for a bigger move until tomorrow's payroll data.

Macroeconomic Data:

ADP data showed a slower increase in jobs than the consensus expected: 54,000 compared to the expected 71,000.

Challenger Job Cuts indicated a significant rise in planned layoffs, increasing from 62,000 to 85,900.

Unit labor costs in the second quarter of 2025 decreased to 1% (expected 1.1%, previously 6.9%).

Overall, these data allow us to observe not only a tightening labor market but, more importantly, a deterioration in the situation of workers at a faster pace than the market anticipated. Pressure on the FED increases with each reading. In light of such poor data, one must ask whether FED rate cuts are overdue. However, the market awaits the verdict until the publication of tomorrow's NFP data.

Donald Trump's trade policy continues to fail. The USA has increased its trade deficit for another consecutive month, mainly with China, particularly in electronics and consumer goods. Tariff policies primarily exert pressure on demand for American goods.

The newly published ISM report for the services sector turned out to be better than expected, indicating sustained resilience in the economy despite weakness in the labor market. The index rose above forecasts, suggesting strong demand in services – a key segment of the American economy.

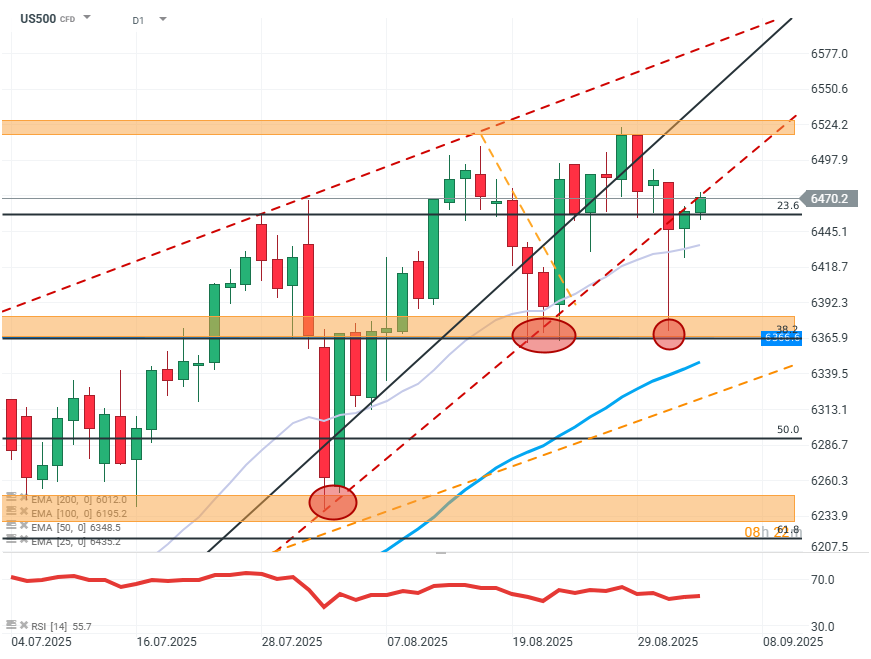

US500 (D1)

Source: Xstation

The price on the chart continues to hold at the lower boundary of the growth channel, which is likely to become a long-term resistance. The nearest trend line is at the level of 6,330 dollars, but the first resistance is very close, at the FIBO 23.6 line. Buyers show their strength by repeatedly defending important levels and quickly recovering losses. In the case of further increases, the nearest strong resistance is the level of the last ATH around 6,500.

Company News:

Broadcom (AVGO.US) — The company publishes its results today after the session. Some investors fear a "sell the facts" scenario in case of even slight disappointment with the results. Expectations for the electronics manufacturer are enormous, with the market seeing an EPS growth of over 30%.

Tesla (TSLA.US) — The company has made its robotaxi application widely available in Austin, the capital of Texas. The price rises by just over 1% at the opening.

Salesforce (CRM.US) — The e-commerce software giant disappointed with its sales forecasts, increasing investor concerns about the pace of AI implementation and monetization. In light of this information, the fact that the company is reducing its workforce by 4,000 people may also be concerning. The stock price starts the session with significant declines, down by as much as 7%.

Apple (AAPL.US) — The technology giant announces the release of its own AI model to compete with ChatGPT and Perplexity. The stock price slightly decreases.

Hewlett Packard (HPE.US) — The producer and distributor of servers and PCs published its results. The company managed to exceed expectations for both EPS and revenues. Additionally, positive sentiment was provided by comments from the CEO, assuring a new era for the company and its participation in the AI market. The stock price notes an increase.

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

🔼 Gold gains 1.7%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.