What to Expect from Key US Economic Data❓

At 2:30 PM, investors will receive the latest inflation data from the US, which, along with the NFP and PCE reports, are the most critical components influencing Federal Reserve decisions regarding interest rates. The importance of this data makes markets eagerly await the report details, which could shape sentiment on Wall Street and the Forex market in the coming days. So, what can we expect from today’s CPI data?

Key Information Before CPI:

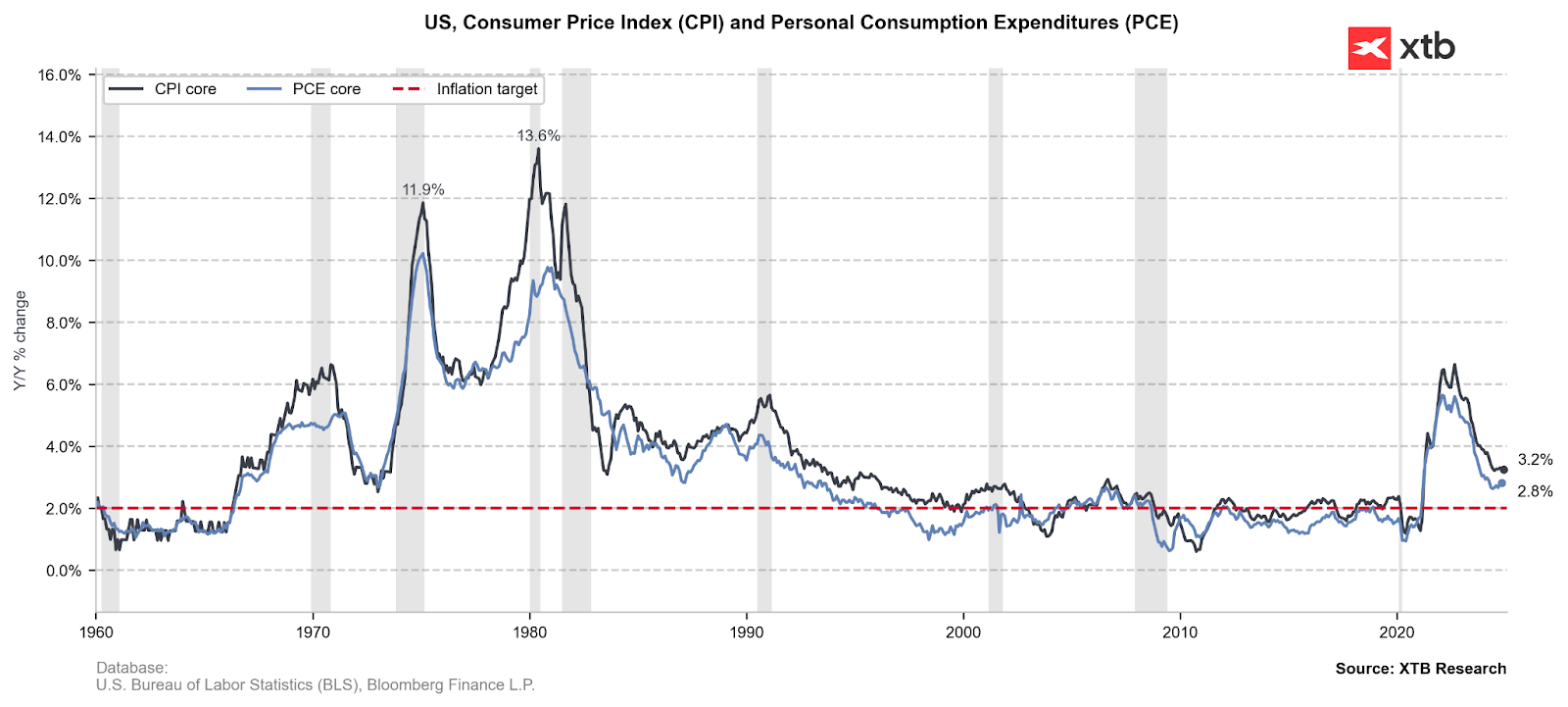

- Headline CPI likely rose to 0.3% m/m in January (vs. 0.4% previously), and core CPI likely increased to 0.3% m/m (vs. 0.2% previously).

- Year-over-year, this would mean the headline CPI remains at 2.9%, while the core CPI falls to 3.1% (from 3.2% previously).

- The January core CPI may show an increase due to seasonality, as companies typically adjust prices at the beginning of the year.

- Inflation data from the second half of 2024 may be revised downward, suggesting that disinflation was stronger than previously thought, potentially reinforcing the Fed's belief that it is approaching its 2% inflation target.

Source: XTB Research

Rising Inflation Expectations

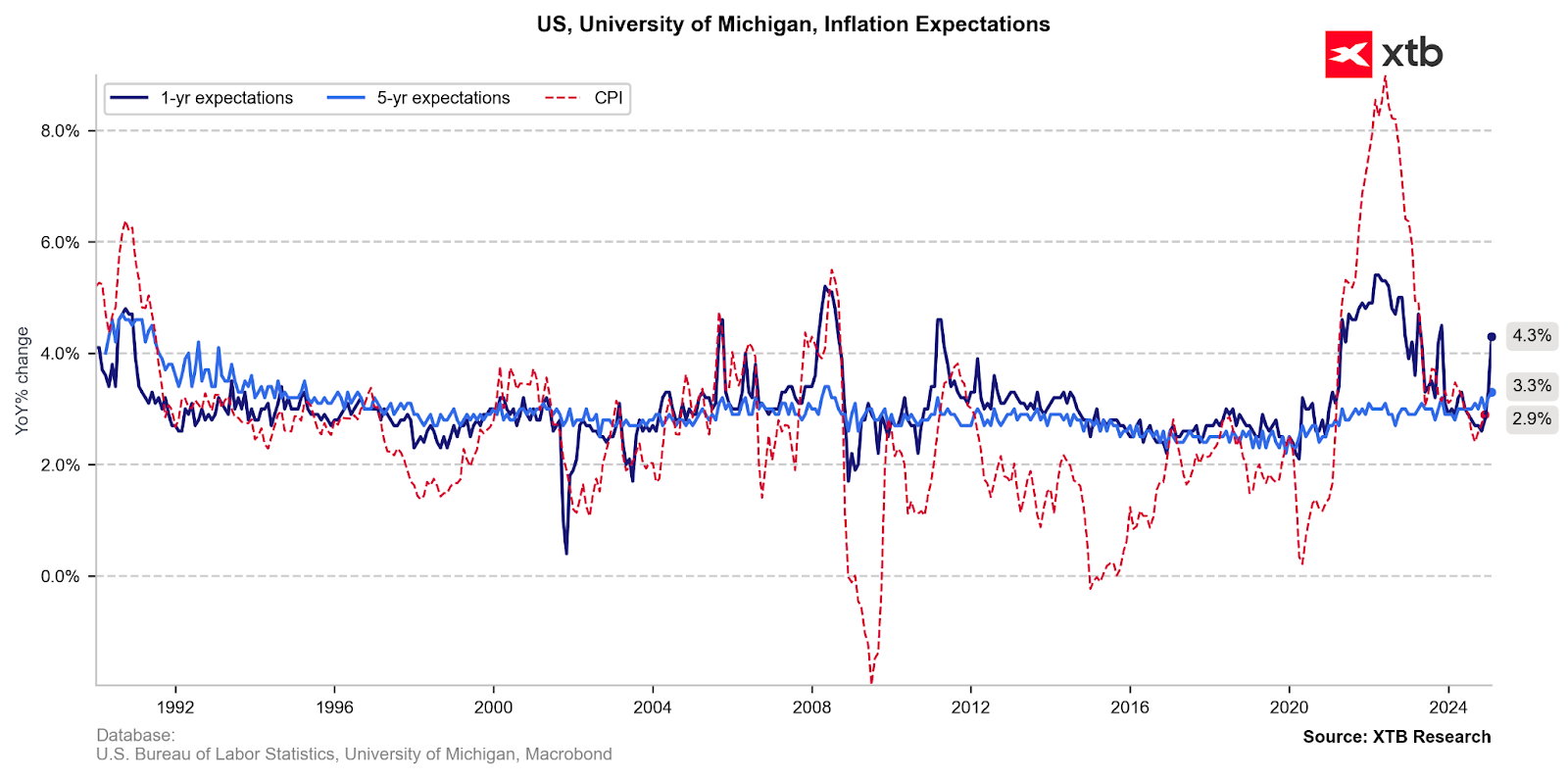

Friday’s report from the University of Michigan showed a significant jump in inflation expectations. US consumers now expect much higher price increases than last month, anticipating 4.3% inflation over the next year (previously 3.2%). A potential source of this spike in expectations is primarily Donald Trump’s tariff policy, which could tighten the goods market in the US in the short and medium term.

Source: XTB Research

No Risk from the Labor Market?

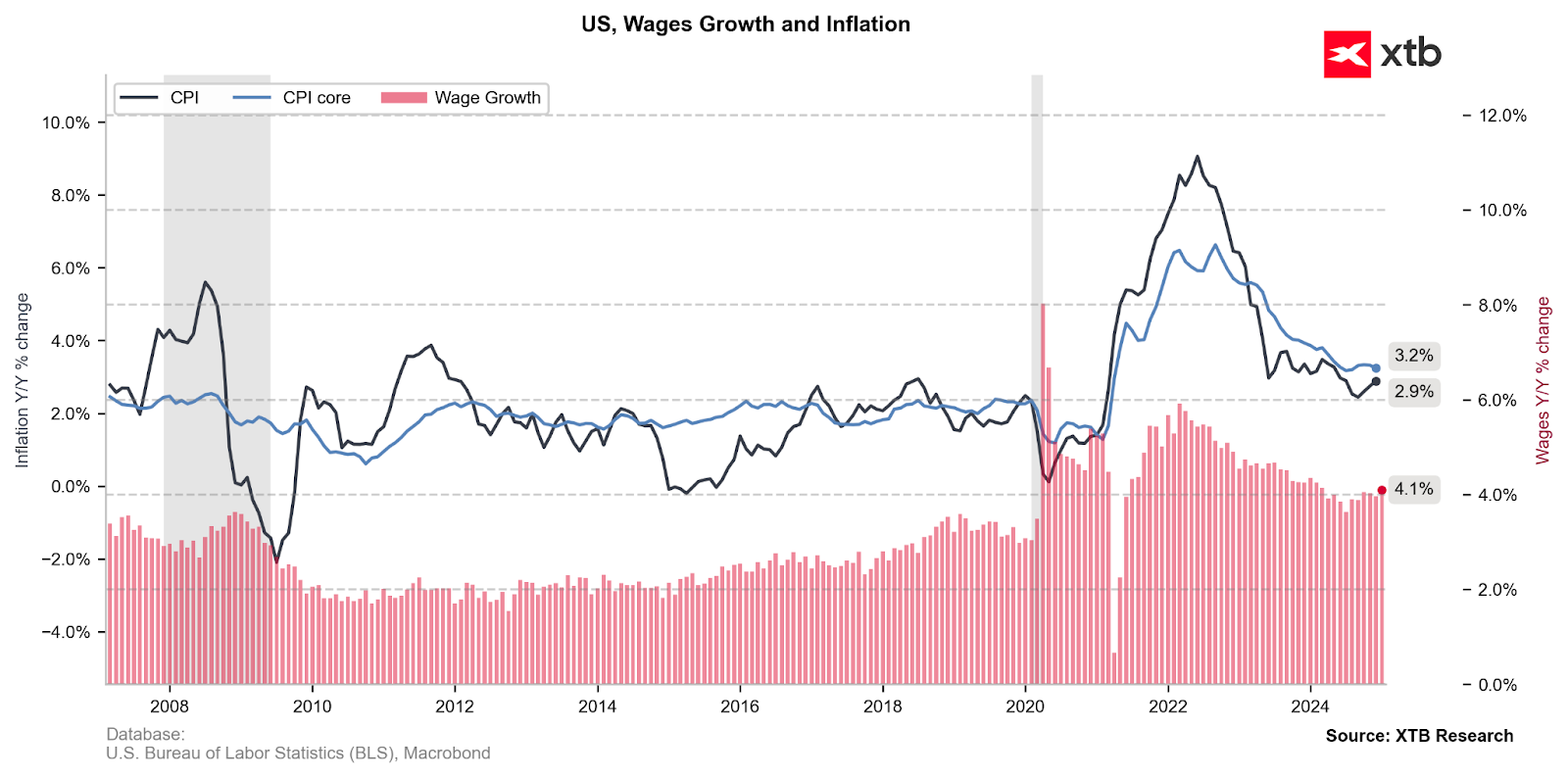

While Jerome Powell clearly emphasized in his speech yesterday that the labor market is not a source of current inflation concerns, US wages (one of the main components of inflation) have shown a gradual increase over the past few months. Wages in January rose more than expected (from 3/9% to 4.1%), but the impact of this data is partly softened by the overall upward revision of the last 2024 NFP report.

Source: XTB Research

Fed's Perspective

A seasonally higher reading should not affect the Federal Reserve’s “not in hurry” stance. The inflation uptick between late 2024 and early 2025 was already forecasted at the start of Q4 2024, both in the US and EU. Therefore, the Fed will focus primarily on the overall trend in core inflation, with additional adjustment, should the year-end data be revised down, signaling strogner transmision of monetary policy.

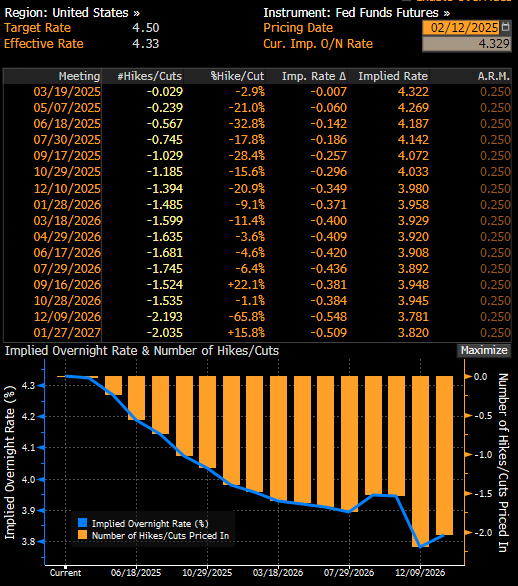

Money markets are currently pricing in the first rate cut in September 2025. A stronger-than-expected drop in core inflation could shift expectations closer to mid-year. However, the anticipated effects of tariff policies can delay such scenario. Source: Bloomberg Finance L.P.

Summary:

- Cars and rents will likely continue to exert downward pressure on CPI in the first half of 2025, supporting the broader disinflation trend.

- The Fed is expected to ignore temporary shocks, such as rising food prices, focusing instead on core inflation trends.

- Revised data indicating stronger disinflation could reinforce the Fed's resolve to keep interest rates unchanged in the short term before cutting them further later.

- Conversely, if inflation readings are higher, the Fed might find a reason to delay easing even more.

- This scenario might be unfavorable for Wall Street, which performs better in an environment of easy capital access.

The US100 is experiencing slight changes today before the CPI data release. However, in the long term, the index maintains a strong upward trend, technically supported by exponential moving averages (50-day, 100-day, and 200-day EMA). These zones remain key support points for this instrument.

Source: xStation5

Daily Summary: A sell-off with a spin-off

Three Markets Worth Watching Next Week (17.07.2026)

US OPEN: The market extends losses as investor concerns grow

Market Wrap: European indices decline amid US - Iran tensions📉 Semiconductors under pressure

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.