The US CPI inflation data for February will be the key macroeconomic report this week. While the whole world is currently focused on tariffs, economic uncertainty in the US and a potential ceasefire in Ukraine, inflation issues could have a huge impact on the Fed's monetary policy, which continues to have a big impact on the dollar. What to expect from today's CPI report?

Market expectations

- The market is quite clearly indicating that it expects inflation to fall to 2.9% y/y, after several months of recent growth

- Inflation futures indicate a reading of 2.9% (it is worth remembering, however, that they also indicated this in January)

- The underlying factors indicate that inflation should not rise unless there is a larger monthly increase than 0.5% m/m

- At the same time, however, this report will show that inflation remains at an elevated level

- A slight decline in core inflation is expected to 3.2% y/y from 3.3% y/y

- Monthly inflation will be important after the recent very strong increase. The pace of price growth is expected to slow to 0.3% m/m, after the last increase of around 0.5%

- The Fed maintains the view that in the context of achieving the inflation target, inflation cannot significantly exceed 0.2% m/m. Inflation has been growing by an average of 0.25% over the past two years, while in the last 10 years it has been growing by an average of 0.26%

- Core inflation per month is also expected to grow by 0.3%

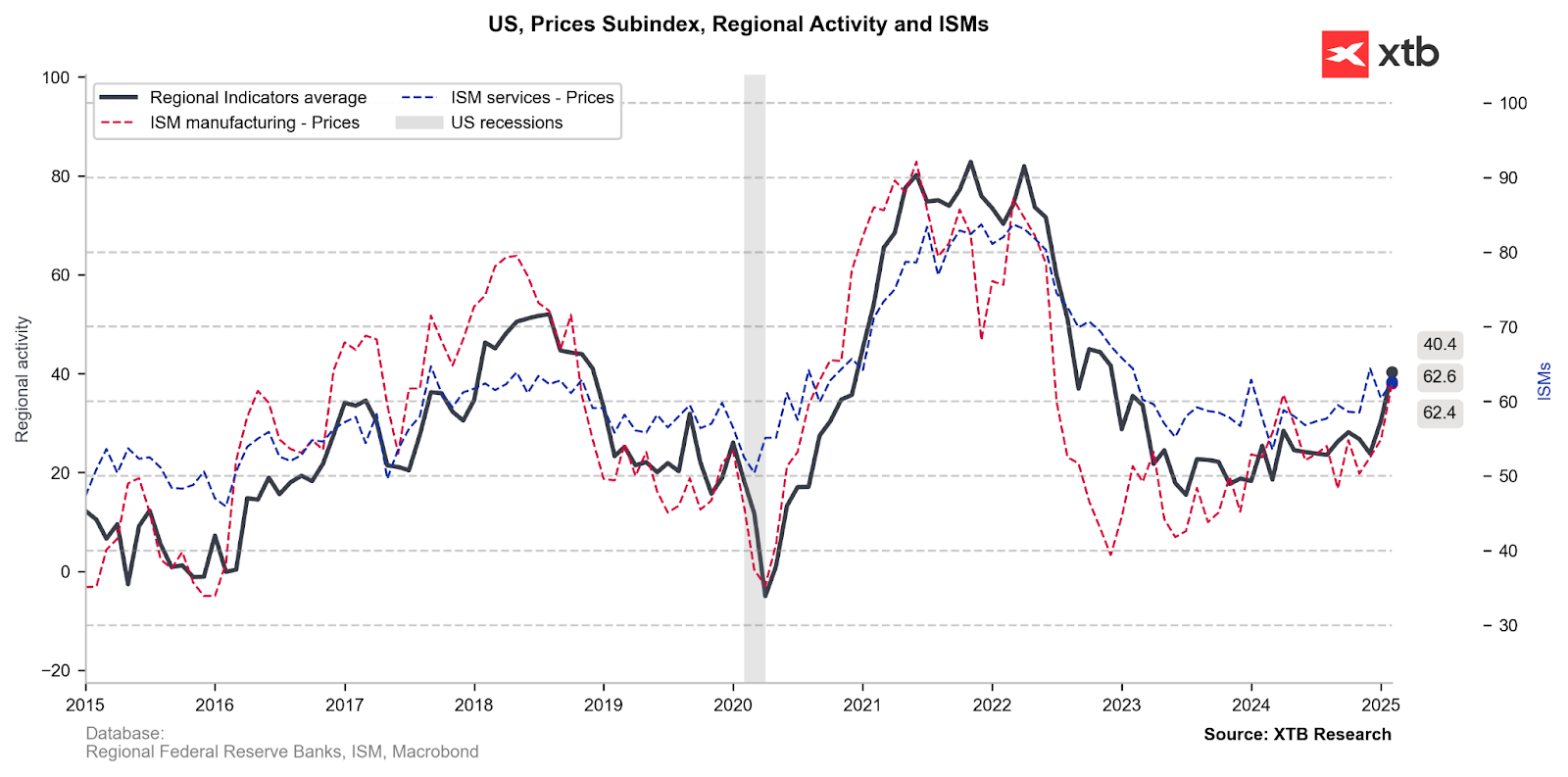

Recent reports on surveys of entrepreneurs in the US have indicated growing price pressure, which may soon have an impact on maintaining inflation at a high level for a longer period. Source: Macrobond, XTB

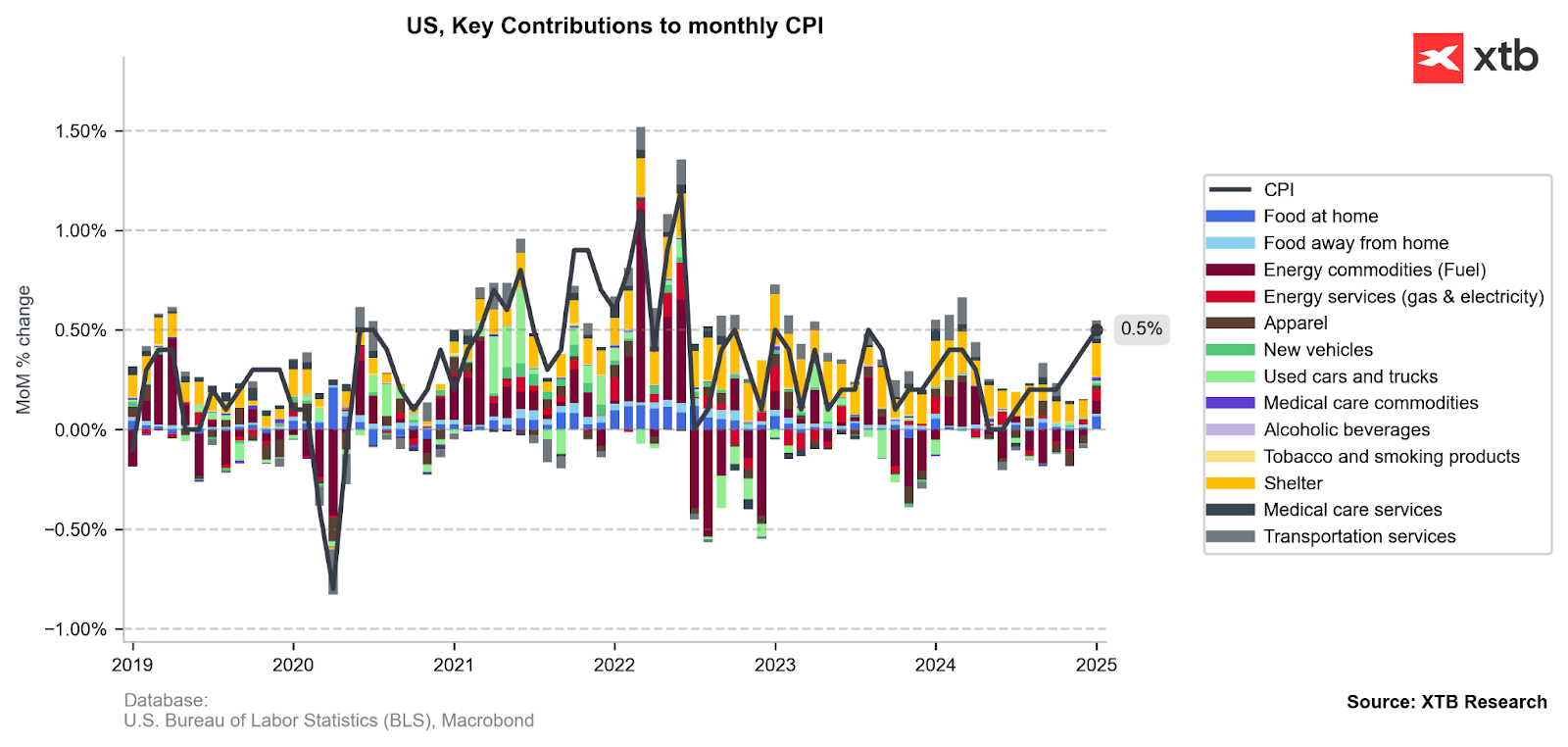

It is worth remembering that previously we observed a huge jump in monthly inflation, driven by rent inflation and gas and electricity prices. Source: Bloomberg Finance LP, XTB

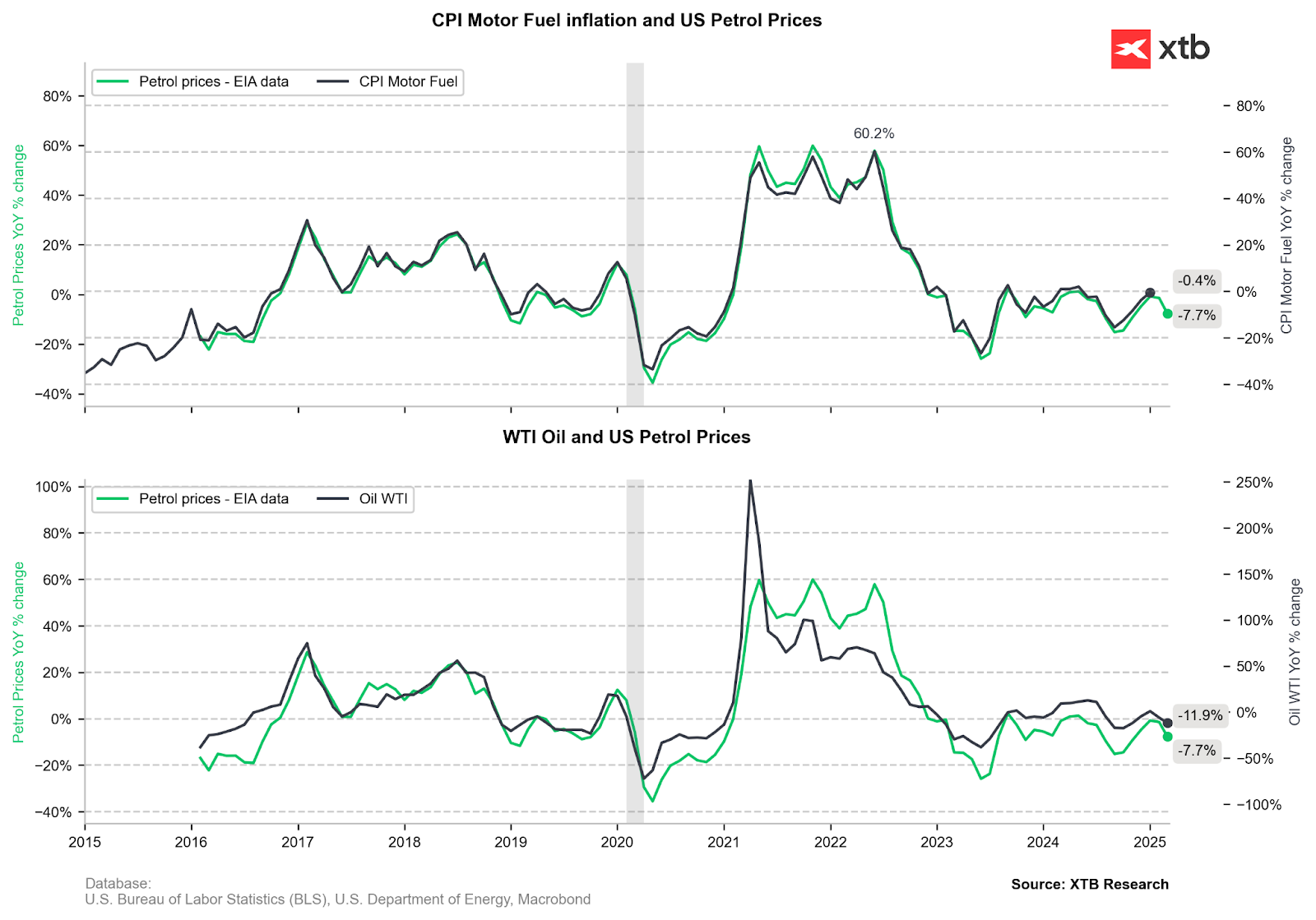

Theoretically, we should see a negative impact of fuel inflation in February, given the decline in oil and fuel prices. Source: Bloomberg Finance LP, XTB

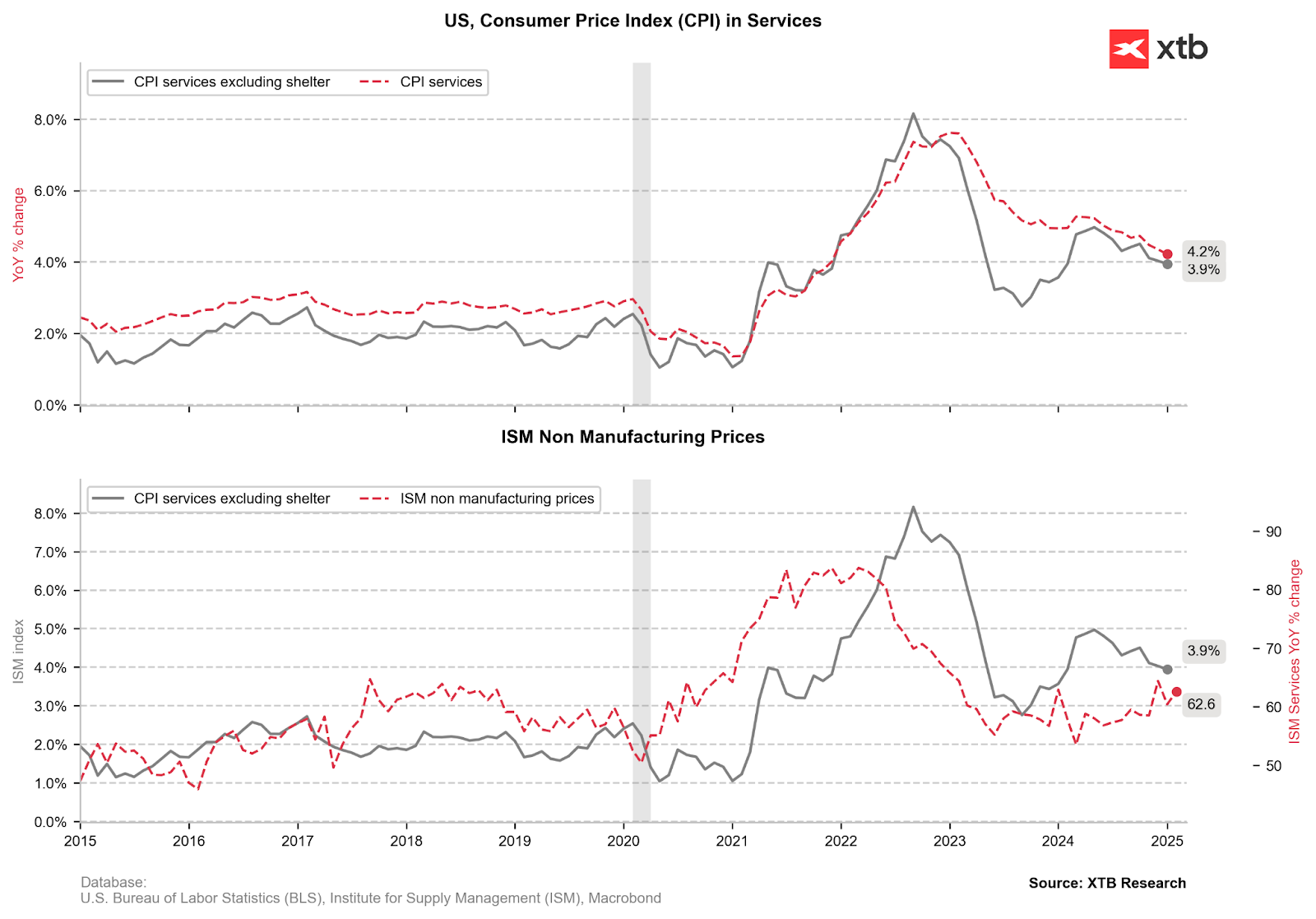

Service inflation remains a mystery, as it has slowed down quite significantly recently, but the ISM price sub-index suggests that further declines may already be limited. Source: Bloomberg Finance LP, XTB

What else to look for?

- BLS increases the weight of goods over services in inflation, which could have serious consequences if tariffs on foreign products continue to be imposed

- BLS increases the share of car inflation in CPI, which could have significant consequences if prices rebound

- BLS slightly reduces the weight of rental inflation, which could support a decline in core inflation if the current trend continues

- Food prices may have a smaller impact on inflation. The growth in egg prices, which have seen significant increases in recent months, has decreased

- Further price declines are expected in the core services sector, such as hotel prices, airline tickets and car insurance

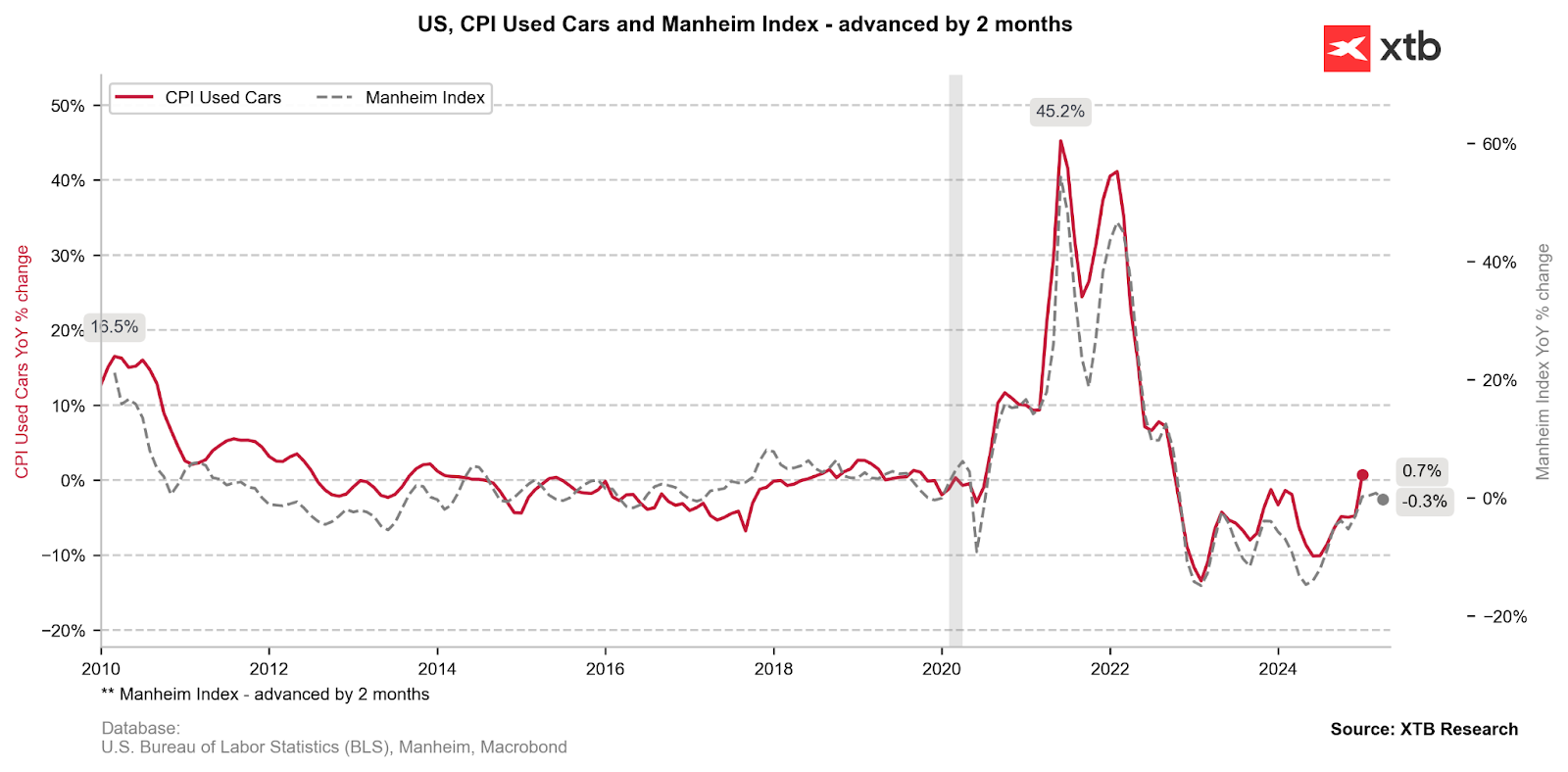

Used car prices have fallen, which should also be reflected in February inflation. Source: Bloomberg Finance LP, XTB

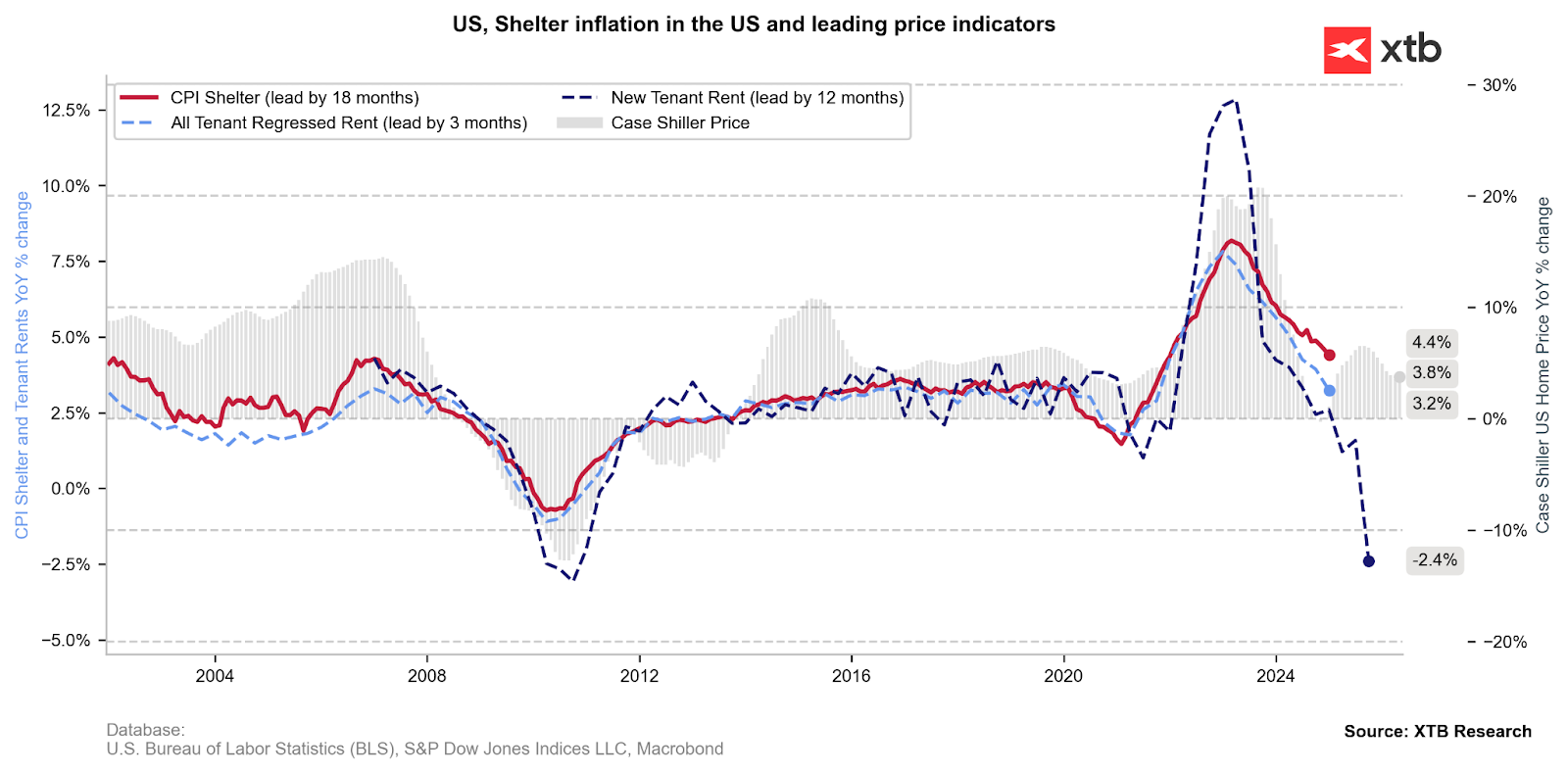

Rental inflation is still the largest category in terms of contribution. Case Shiller may suggest the end of the decline in this category, but at the same time, new rental prices are falling very sharply, which may outweigh the further decline in overall rental inflation. Source: Bloomberg Finance LP, XTB

How will the market react?

Today's data is unlikely to change the Fed's perception of the inflation situation. Of course, this report should be much better than January's, although at the same time it is necessary to take into account the beginning of the impact of tariffs on the inflation situation, although currently to a much limited extent. The greatest impact on inflation is expected to be visible in the second quarter of this year. If today's reading shows a decline in inflation or a greater decline in inflation than expected, there is a chance of further stimulation of Wall Street to make up for losses. Lower inflation would be a harbinger of possible future cuts, which are still uncertain. Powell indicated during his last speech that inflation remains high and the labor market is strong, which theoretically rules out the possibility of cuts at the moment. However, if inflation starts to fall faster, there is also a chance for a faster reaction from the Fed.

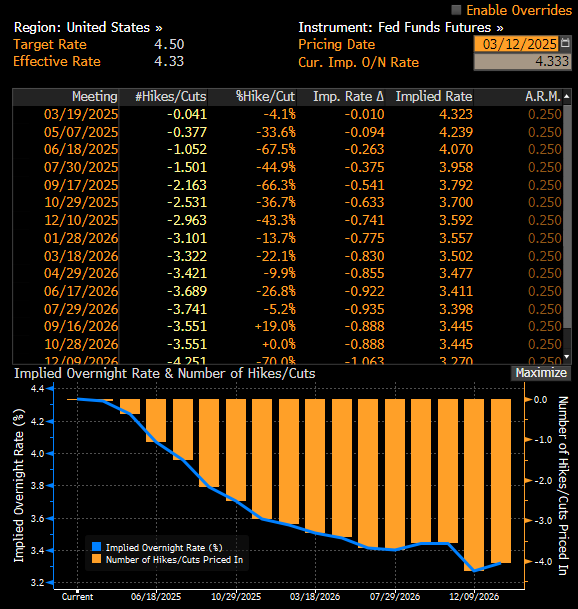

At the moment, 3 cuts from the Fed are priced in, with the first cut this year in June. Source: Bloomberg Finance LP, XTB

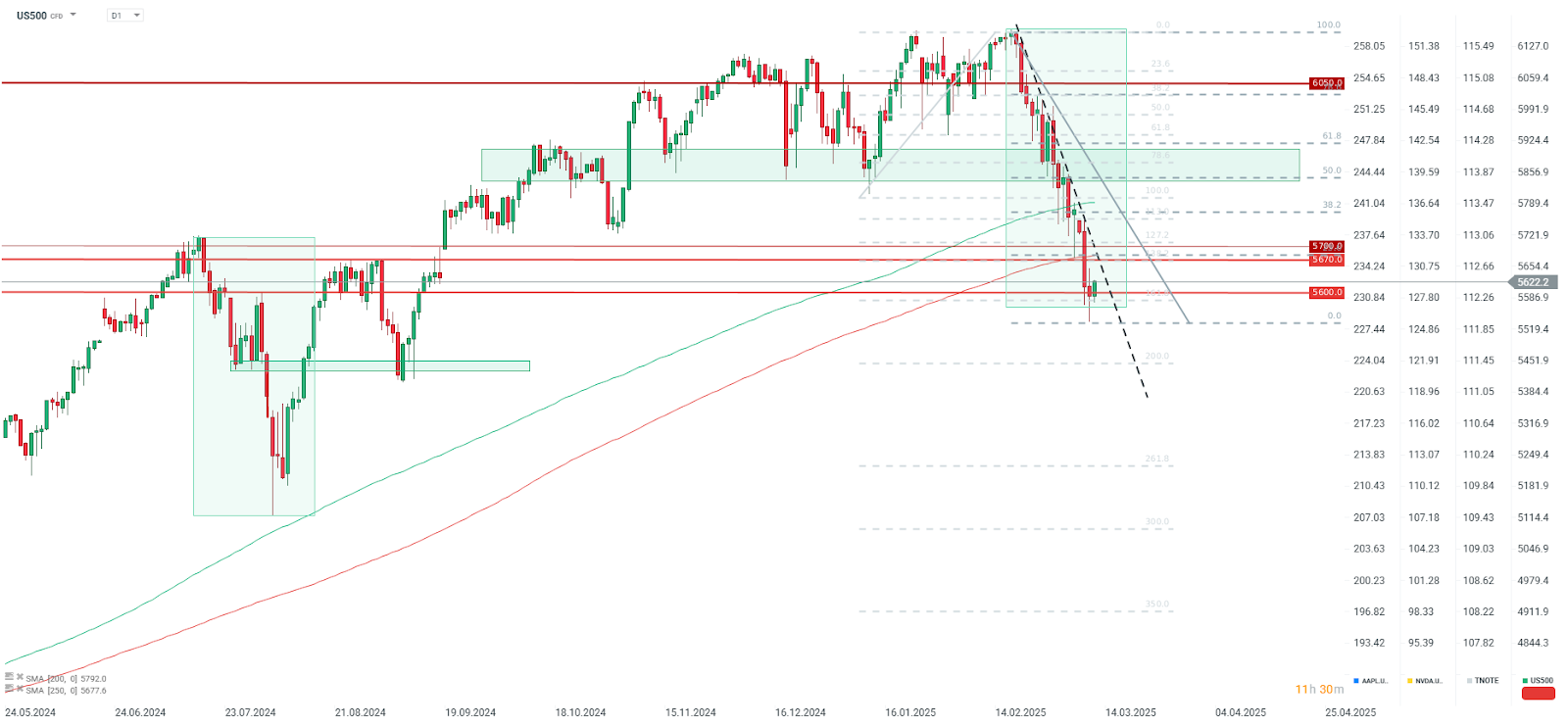

The US500 is currently losing about 5% since the beginning of this year and over 8% from its historic peak. The declines are definitely due to the Mag7 group, which has lost 15% of its value since the beginning of this year. Currently, the very important support on the US500, designated by the 161.8 retracement of the last upward impulse and the 5600 level, is being tested. At the same time, the range of the previous largest correction in the upward trend is being tested. The nearest important resistance is around 5670-5700, where there is also a 23.6 retracement of the entire last downward impulse and the 250 session average. This level is key - if it returns above it, the upward scenario will start playing out again. However, if not, a repeat of 2022 will be possible, when the 250 session average was broken for over a year. Source: xStation5

Daily Summary: Markets limit the pullback while awaiting the Fed

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.