Such key events like FOMC or ECB decisions are already behind us and they failed to spur optimism on the markets. Moreover, banking sector issues continue to weigh on the risk appetite. Now the time has come for the final top-tier event of the week - release of US jobs market data for April!

Expectations

- Non-farm payrolls: 180k expected vs 236k previously (ADP: +296k)

- Private NFP: +160k expected vs 189k previously

- Unemployment rate: 3.6% expected vs 3.5% previously

- Wage growth (annual): 4.2% YoY expected vs 4.2% YoY previously

- Wage growth (monthly): 0.3% MoM expected vs 0.3% MoM previously

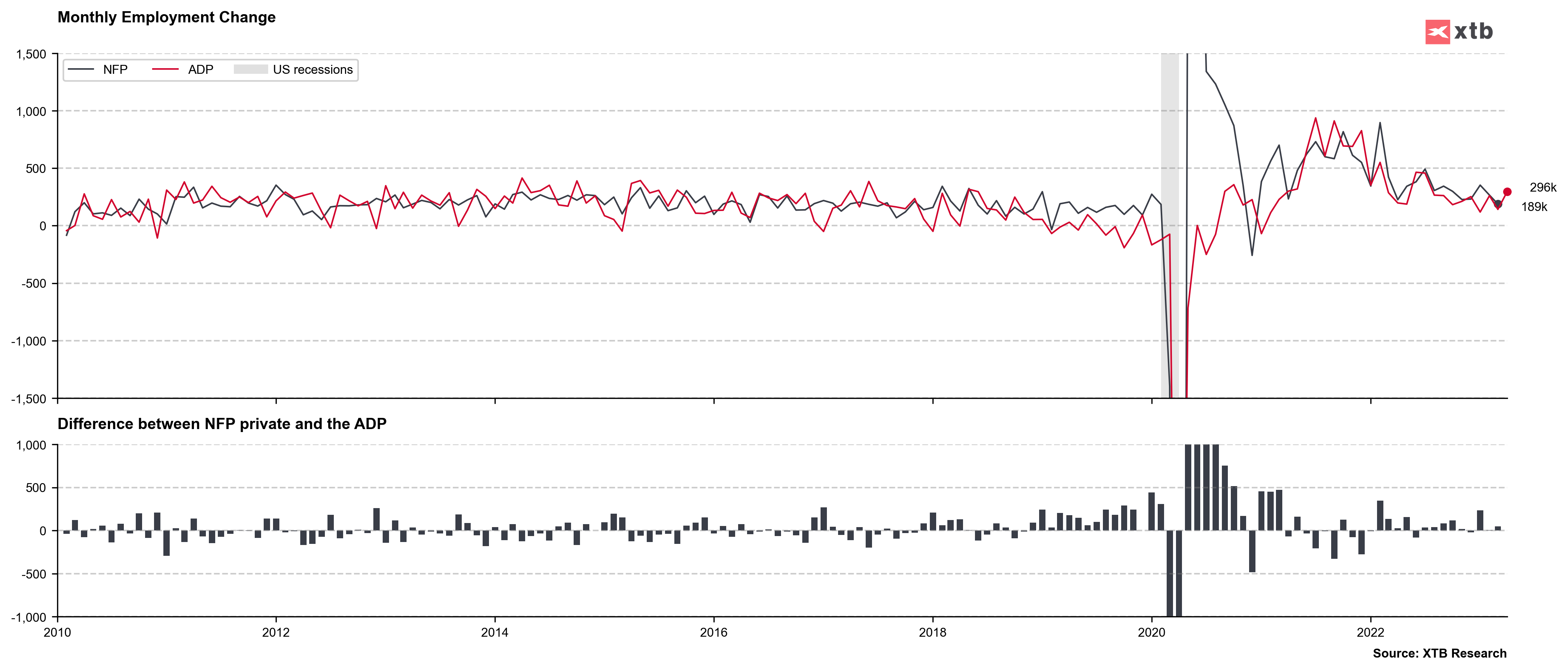

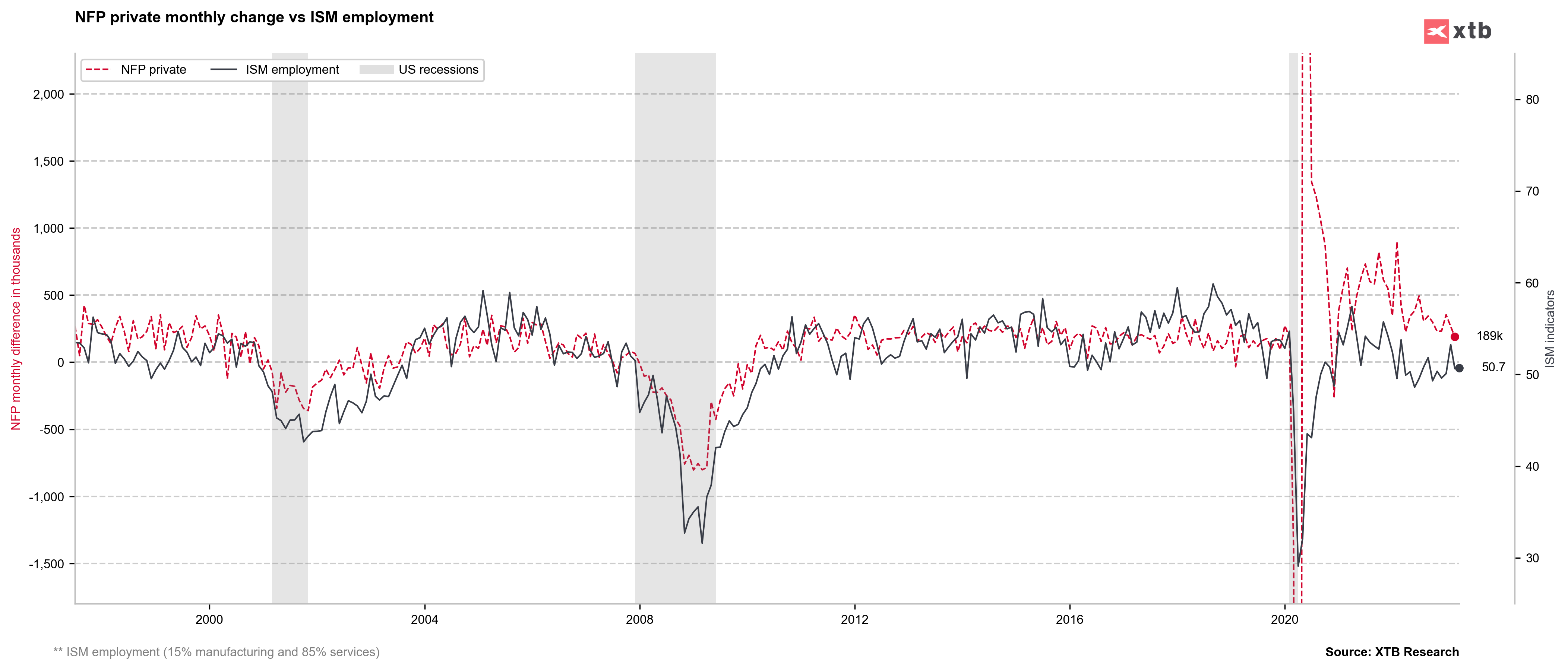

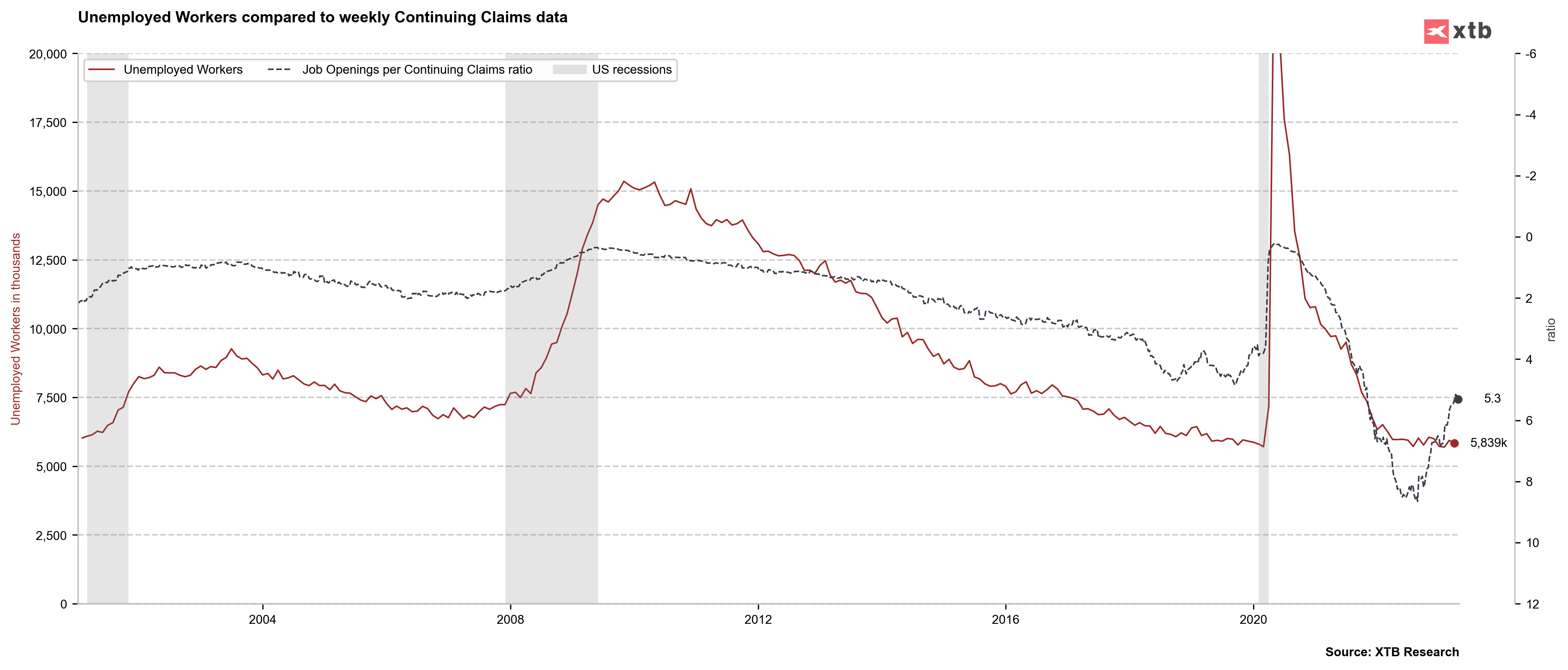

It should be noted that some worrying data from the US labor market has been released recently. Initial jobless claims climb towards 240k, JOLTS dropped significantly below 10 million while planned lay-offs are on the rise. ISM employment subindices have been struggling as of late but composite for both services and manufacturing sectors remains above 50 points threshold, signaling expansion. An expectations for the slowdown in US jobs market were distorted by ADP report released earlier this week as it came significantly above expectations, signaling a jobs gain of almost-300k. Moreover, it should be noted that ADP has been printing lower readings than NFP in recent months.

ADP employment gain has seldom exceeded the one signaled by NFP report since the beginning of 2022. Source: Macrobond, XTB

ADP employment gain has seldom exceeded the one signaled by NFP report since the beginning of 2022. Source: Macrobond, XTB

Composite ISM employment subindices remains above 50 points but does not point to any major expansion. Source: Macrobond, XTB

Composite ISM employment subindices remains above 50 points but does not point to any major expansion. Source: Macrobond, XTB

Ratio of job openings to initial jobless claims have been dropping recently. Interestingly, the overall number of unemployed remains relatively stable. Source: Macrobond, XTB

Ratio of job openings to initial jobless claims have been dropping recently. Interestingly, the overall number of unemployed remains relatively stable. Source: Macrobond, XTB

How will market react?

EURUSD continues to trade without a clear direction but at elevated levels. Meanwhile, US indices have been selling off hard in recent days. Strong jobs gain as well as lower wage growth would be positive for equity markets, especially US500, where the share of the financial sector is quite large. On the other hand, excessive employment gain and acceleration in wage growth could boost market odds for one more rate hike from the Fed. A miss in employment data could, however, have a negative impact on equities as it would hint at rising recession risk. Data released earlier suggests the first scenario but the other 2 cannot be ruled out.

US500 dropped to the lowest level since late-March. Should current recovery turn out to be short-lived and US500 drops below 4,000 pts, bears may attempt to realize the range of a double (triple) top pattern. Source: xStation5

US500 dropped to the lowest level since late-March. Should current recovery turn out to be short-lived and US500 drops below 4,000 pts, bears may attempt to realize the range of a double (triple) top pattern. Source: xStation5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.