The Consumer Price Index data report is scheduled for release at 1:30 pm GMT. Annualized inflation is expected to ease further, therefore monthly CPI data will draw more attention, as it is likely to rebound and emerge as a cause for concern for the Federal Reserve.

Although inflation has shown signs of peaking at 9.1% in June last year, it remains more than three times above the Fed's 2% target and continues to point to a broad-based advance on the general price level, particularly services and housing.

It is expected that today's data will show a deceleration in headline price growth from 6.5 to 6.2% YoY while core gauge is seen dropping from 5.7 to 5.5% YoY. On a monthly basis, the CPI is forecast to increase to 0.5% mainly due to higher energy prices and rebound of used car prices, while the Core CPI is expected to remain at 0.4% as rent prices are still elevated.

Markets are somewhat positioning for a slightly hotter-than-expected CPI reading, given strong labor market data for January. Median forecasts point to a significant slowdown in both headline and core annual gauges. On the other hand, expectations for month-over-month readings do not look so rosy. Source: xStation5

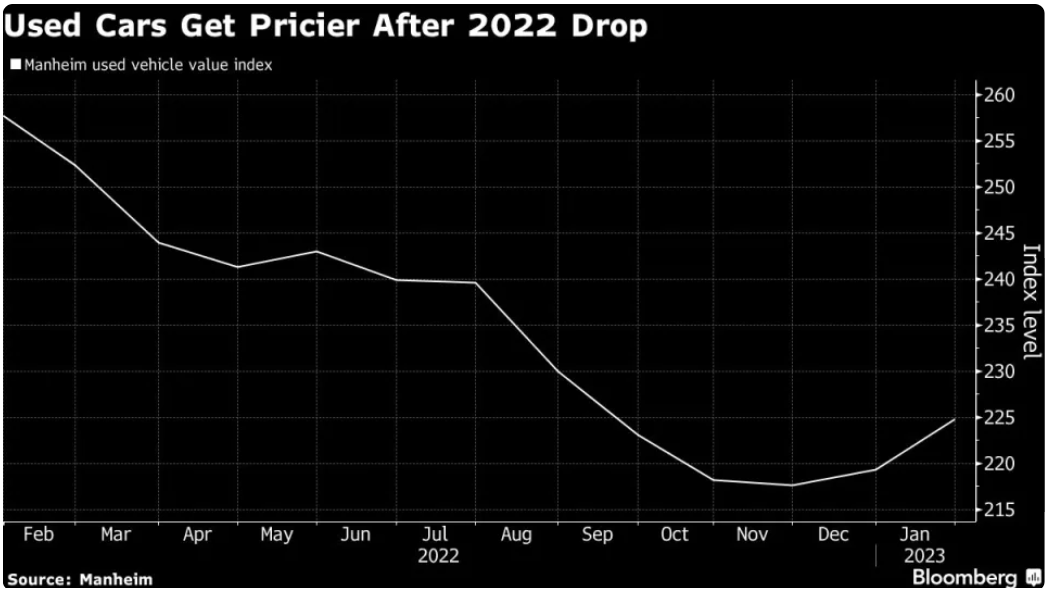

Markets are somewhat positioning for a slightly hotter-than-expected CPI reading, given strong labor market data for January. Median forecasts point to a significant slowdown in both headline and core annual gauges. On the other hand, expectations for month-over-month readings do not look so rosy. Source: xStation5 The used car prices in the US resumed an upward move in January. Source: Bloomberg via Manheim

The used car prices in the US resumed an upward move in January. Source: Bloomberg via Manheim

Taking a look at energy prices we can see that those dropped significantly at the end of 2022, however rebounded slightly in January, therefore impact of recent declines may be limited on today's report.

Fuel prices continue to point to a possible decline in inflation, but the short-term impact of cheaper gasoline may be limited. Source: Bloomberg, XTB Research

Fuel prices continue to point to a possible decline in inflation, but the short-term impact of cheaper gasoline may be limited. Source: Bloomberg, XTB Research

The Fed is currently focusing on services inflation, excluding the real estate market, which still remains elevated and leaves some room for surprise. Source: Bloomberg, XTB Research

A softer-than-expected reading would reinforce bets that the Federal Reserve could bring a pause to its policy tightening beginning from Q2 2023, which would prompt fresh selling around the US Dollar. On the other hand, even a slight setback could be a major blow and leave at least two more hikes, maybe more, on the cards. Any meaningful divergence from the expected readings should infuse some volatility in the markets and allow traders to grab short-term opportunities around the USD pairs and futures linked to US indices.

According to JPMorgan these are potential scenarios on how the S&P 500 may react after CPI release:

- CPI below 6% - S&P 500 moves up by 2.5%-3%

- CPI 6.0%-6.3% - S&P 500 moves up by 1.5%-2%

- CPI 6.4%-6.5% - S&P 500 moves down by 0.75%-1.5%

- CPI above 6.5% - S&P 500 moves down by 2.5%-3%

US500 once again approaches key resistance at 4175 pts, which coincides with 23.6% Fibonacci retracement of the upward wave launched in March 2020 and upper limit of the 1:1 structure. Also medium-term 100-day EMA (purple line) recently crossed above the long-term 200-day SMA (red line). This formed a bullish ‘golden cross’ formation, which can at times precede a move higher. Nevertheless as long as price sits below the aforementioned resistance, another downward wave may be launched towards crucial support at 4000 pts. However if bulls manage to uphold recent momentum, then upward move may accelerate towards highs from August 2022 around 4335 pts. Source: xStation5

Morning Wrap: Oil Rises Again (07.08.2026)

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.