- Fed will announce the first rate decision of 2024 today at 7:00 pm GMT

- Economists do not expect rates to be changed

- This meeting will not be accompanied by release of new economic projections

- US central bank may attempt to set expectations for the timing of the first rate cut

- Markets are speculating about possibility of slowdown or even pause in QT

- USD remain strong, while US indices trade near record highs

The Federal Reserve will announce the first rate decision of 2024 this evening (7:00 pm GMT). USD has been very strong as of late as market odds for a March rate cut diminished. Moreover, downward move on EURUSD was additionally fuelled by lack of hawkish comments from ECB. On top of that, rebound in oil prices and tensions in the Middle East are creating risk of the second wave of inflation and, at the same time, boost demand for safe haven assets, including US dollar. What should we expect from the FOMC meeting today? What will markets focus on?

Timing of the first rate cut

Investors were offered a number of macro reports from the United States recently, which hinted that the US economy is still in good shape and that the Fed may be able to wait with delivering the cut.

- NFP data for December came in at 216k, above 170k expected. Unemployment rate dropped to 3.7%

- US annualized Q4 GDP growth reached 3.3%, while market expected just 2.0%

- US CPI inflation accelerated to 3.4% YoY in December, while core measure slowed less than expected

- University of Michigan consumer sentiment rebounded from 69.7 to 78.8 in January

- Manufacturing PMI climbed back above 50 points threshold in January, while services index jumped to almost 53 points

- JOLTS report showed job openings back above 9 million in December

On the other hand, there are also some negative factors in play that may justify the need for quicker end to tight monetary policy

- Regional indices showed a collapse in economic activity, but it is not evidence by PMIs

- Core PCE inflation dropped to 2.9% YoY in December, while headline PCE inflation stayed unchanged at 2.6% YoY

- Falling PPI inflation suggests further negative impact on consumer prices

- ADP report for January showed 107k employment increase, below 145k expected

CPI inflation rebounded in December, while PCE inflation came in below market expectations. Source: Bloomberg Finance LP, XTB

CPI inflation rebounded in December, while PCE inflation came in below market expectations. Source: Bloomberg Finance LP, XTB

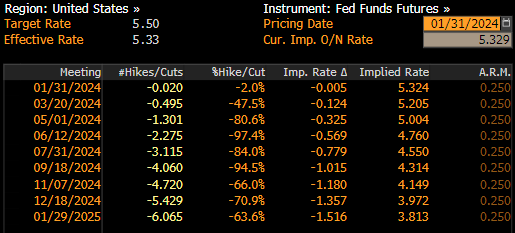

As one can see, positive factors are much more abundant than negative ones, therefore the chance of Fed delivering the first rate cut as soon as at March meeting is rather slim. Money markets are pricing in less-than-50% chance of such a development. However, timing of the first rate cut will not be the only thing investors will focus on. The decision on quantitative tightening (QT) will also be watched closely. It is rather unlikely that the Fed will announce any major changes today, but any hints may be an important mover for the US dollar.

Money markets are pricing in less than 50% chance of Fed rate cut in March, while those odds stood at almost 90% as recently as in December. Source: Bloomberg Finance LP

Is balance sheet more important?

While discussions have mainly focused on the timing of interest rate cuts in recent months, Federal Reserve members addressed an important issue during the December meeting – the reduction of the Fed's balance sheet. Due to previous QE programs, particularly the pandemic-related one, the Fed's balance sheet has expanded to a massive level of 9 trillion dollars. Fed has been limiting its balance sheet by not reinvesting in bonds since mid-2022, resulting in a reduction of the balance by approximately 1.5 trillion dollars so far. Previously, the Fed indicated a desire to reduce the balance sheet by about 2.5 trillion dollars. However, concerns have arisen that further reduction could lead to a liquidity problem, as experienced in 2019. Demand for dollar liquidity has increased significantly, leading to a substantial rise in dollar lending rates. The Fed quickly intervened with an open market operations program, but at one point, there were noticeable movements in the debt market, a strengthening of the dollar, and a decline in the stock market.

The Fed suggested in its research that a balance reduction of $2.5 trillion would be equivalent to a 50 basis points increase in interest rates. Given the current level of inflation and interest rates, there is no need to reduce the balance at such a pace or even continue the entire QT.

Therefore, it is not ruled out that during today's meeting, there will be signals about the future of QT. If more specifics are presented, such as the possibility of slowing down in March or June or ending QT by the end of this year, it could lead to a weakening of the U.S. dollar and provide support for the stock market. However, if no concrete details are provided, signals about the first possible interest rate cut will be more crucial.

At present, liquidity in the market remains high, as evidenced by ongoing reverse repo operations that withdraw liquidity from the market. Simultaneously, there is a significant decrease in these operations, which may indicate that the moment to abandon QT is approaching.

What to focus on in the statement and during Powell's press conference?

- Changing wording of the statement to highlight that policy is in appropriate stance could be seen as a dovish development and may weaken the US dollar. Earlier, Fed's statement hinted at a need to strengthen policy stance

- Adding a phrase on increase in uncertainty related to jobs market and inflation - such a phrase was added in 2019 prior to the rate cut

- Investors should also look for similar statements that were present in January 2019, which heralded the end of QT. Back then it was hinted at a possibility of adjusting balance sheet normalization details to potential economic and financial changes

Inclusion of such statements would confirm the dovish turn from Fed and may lead to a potential weakening of the US dollar and more gains on Wall Street. Keeping the current status quo and lack of any changes in the statement would be positive for USD and may put pressure on equities. However, it should be said that performance of the stock market is driven mostly by earnings reports now.

How will markets react?

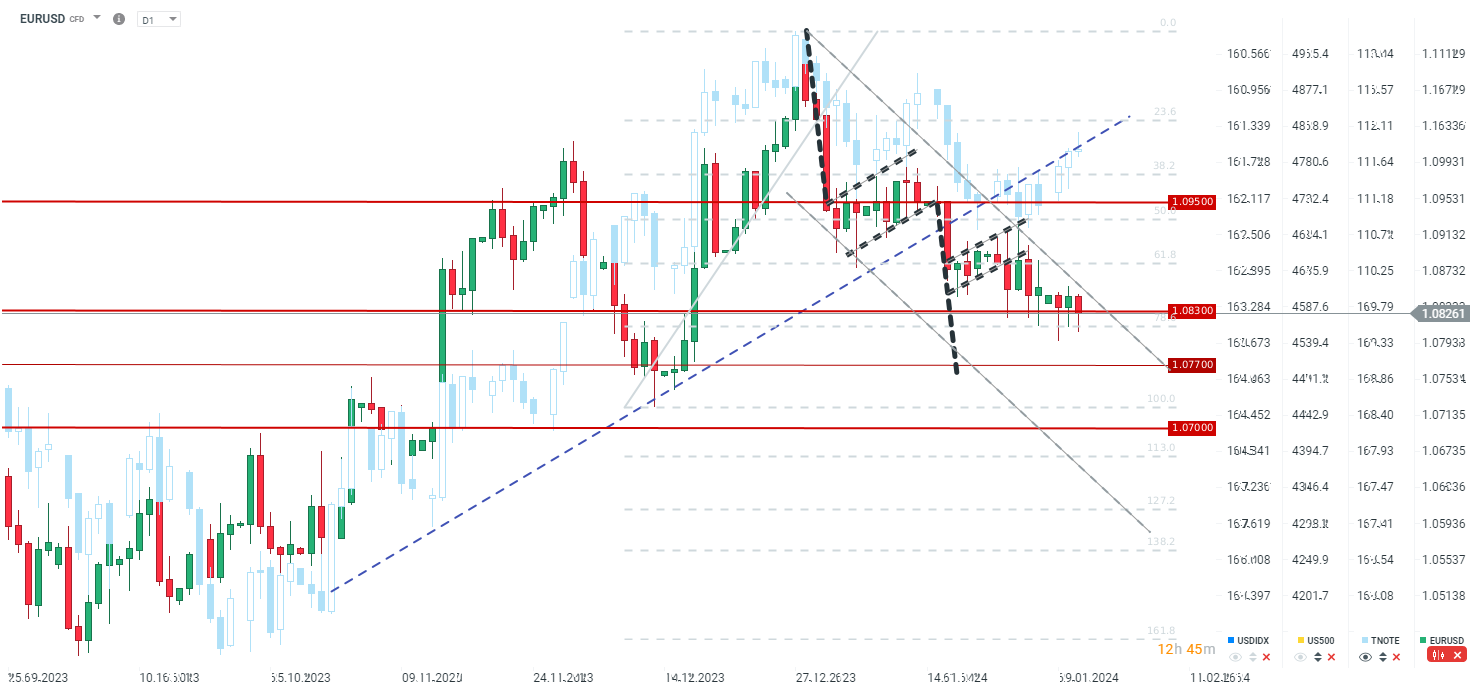

EURUSD

The main currency is trying to recover following a test of the 1.0800 mark, supported by falling bond yields. There is a significant divergence between EURUSD and bond markets, suggesting a potential for the pair to rebound. However, should Fed fail to deliver onto dovish expectations, USD may gain with the pair breaking below support market with 78.6% retracement in the 1.08 area.

Source: xStation5

Source: xStation5

US500

US500 reached the range of the breakout from an inverse head and shoulders pattern, and is now pulling back from the 4,950 pts area. A drop in bond yields (pick-up on TNOTE market) can also be spotted. One cannot rule out divergence between stock and bond markets narrowing, but US500 may wait for the next set of top-tier tech earnings on Thursday (Apple, Amazon and Meta) before delivering the next big move. Should Fed fail to signal a change in their policy stance, one cannot rule out US500 pulling back to as low as 4,830 pts area. On the other hand, a dovish turn from Fed may allow the index to climb above the psychological 5,000 pts mark.

Source: xStation5

Source: xStation5

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

Nasdaq Gains 0.6% and Reclaims 29,000 🔼 Strong Results from ON Semiconductor and Palantir

🗽 US500 sets a new record high

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.