The yen is losing almost 1.3% today against the US dollar today, due to several factors.

- Japan's upcoming elections on October 27

- The Bank of Japan's decision on October 31

- Elections in the United States

- The Fed decision

- Weak economic forecasts from the IMF

Bad times for yen?

- Elections in Japan will be held this Sunday, and recent polls show that the current ruling coalition may not hold a majority. Markets don't like change, and there is a good chance that another government will have a different idea for the faltering economy.

- Immediately after the election, the Bank of Japan will make a decision. Communication from the BoJ has not hinted at an imminent interest rate hike recently. The next hike is not possible until March, when the market gives the move an 80% probability.

- The yen is also weakening due to the increasing likelihood of Trump winning the election. Popular betting portals give 60 to 64% probability for the former president to win. Trump has repeatedly spoken negatively about Japan's policy of maintaining a weak yen and has been eager to impose tariffs on Japanese products.

- The IMF is lowering the growth outlook for Japan this year to just 0.3% y/y from 0.7% y/y. In its decision, the IMF points out that the boom in tourism due to the cheap yen was only a one-time event, plus the auto sector is in a lot of trouble.

... And good times for US dollar

Part of the sell-off is also due to the strength of the U.S. dollar. Yields on 10-year Treasury bonds rose yesterday to 4.2%, a level not seen since July, providing evidence that the market does not see an aggressive cycle of Fed cuts as the base case scenario for the next few quarters.

- While the IMF lowered GDP growth forecasts for most developed economies, for the United States it raised its economic growth forecast for 2025. Currently, the market is pricing in a nearly 13% chance of no Fed rate cut, in November, but next year is in greater question,

- According to the 'dotplot' presented at the September meeting, we should see up to ca. 100 bps of rate cuts next year. With strong macro data from the US economy and the risk of rising oil prices, the market now sees such a scenario as less realistic; the labor market shows no 'alarming' signs of a slowdown, drawing any pressure from the Fed for an accelerated easing cycle.

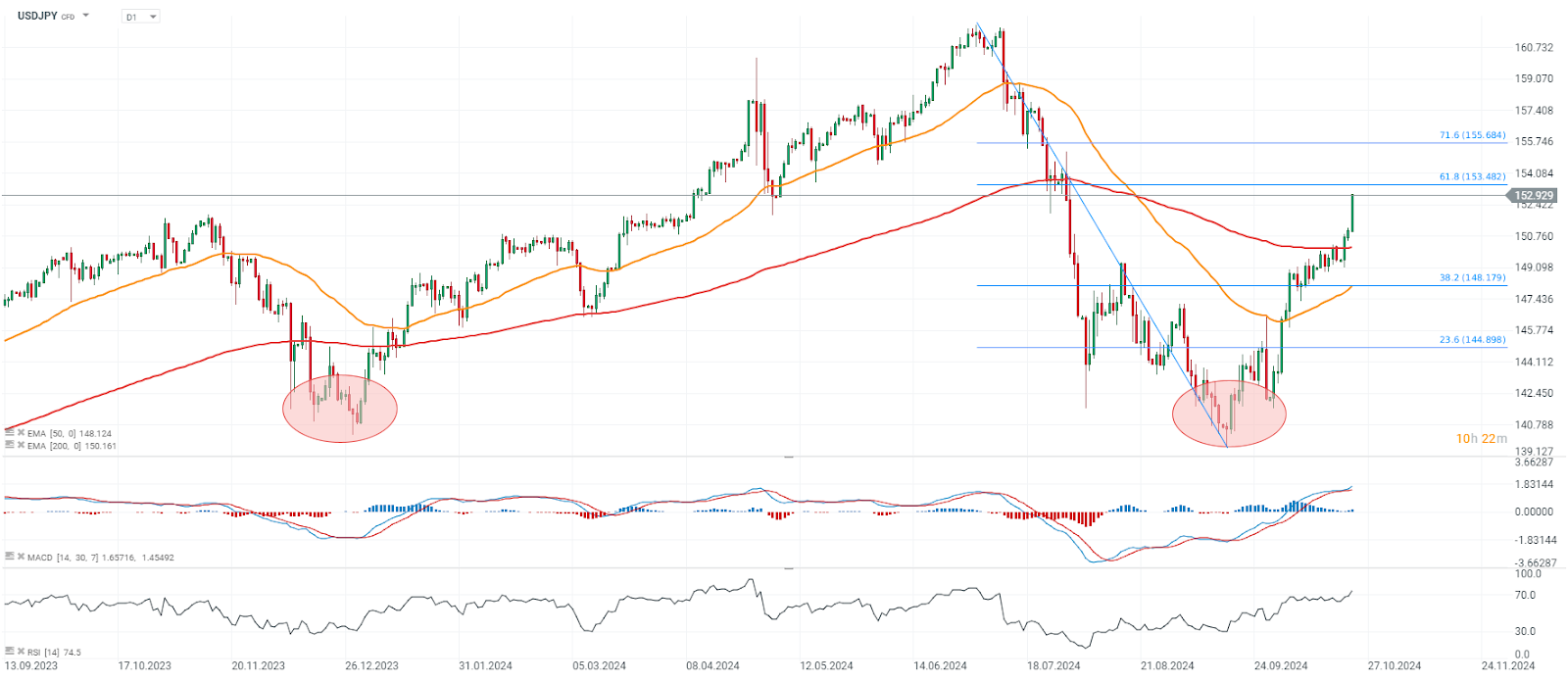

USDJPY (D1 interval)

USDJPY is breaking through the 200-session average, having earlier bounced off the 100-session average. The pair is currently at its highest since July this year. We are also seeing a decline in long positions and an increase in short positions, indicating speculative capital's doubt about the yen's ability to remain strong. The pair is currently testing the abolition of 61.8 of the last downward wave. If this level is pierced, the next important target for the pair will be the 155 level. At present, only an interest rate hike preceded by a clear victory for the LDP party in Japan could turn the tide on the currency pair.

Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Economic Calendar: Industry’s condition in the shadow of oil prices

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.