US stock market sentiment remains fragile, as investors attempt to price in a wide range of possible outcomes related to the conflict in the Middle East, while receiving mixed diplomatic signals from Washington. S&P 500 futures are down 0.8%, after earlier swinging between gains and losses, underscoring persistent uncertainty. A lack of de-escalation between the US, Israel and Iran increases recession risks, while a swift agreement could trigger a relief rally. Technology stocks are under notable pressure, with pronounced selling visible across the software sector, weighing on broader equity sentiment.

- US Treasury yields moved higher, with the 2-year yield rising to 3.88% (+3 bps), suggesting limited demand for safe-haven assets despite geopolitical tensions.

- Oil prices climbed back above $90 per barrel, recovering part of earlier losses as markets continue to price in potential supply disruptions in the region.

- The US dollar strengthened by 0.2%, while gold remained relatively stable, pointing to a selective rather than broad-based flight to safety.

- Initial optimism around potential peace talks faded quickly, after Iran denied reports of substantive negotiations with the US, despite earlier comments from Donald Trump.

- Sentiment deteriorated further following reports that Persian Gulf allies may become involved, increasing the risk of broader regional escalation.

- The wide range of possible scenarios is driving elevated volatility across global markets.

- European equities edged up 0.1%, with Puig Brands standing out, surging as much as 17% following reports of takeover talks with Estée Lauder.

- Gold erased earlier gains after Turkey signaled it may use its gold reserves to support its currency.

- Investors remain concerned about lasting economic effects, even if the conflict de-escalates quickly. According to UBS, volatility is likely to remain elevated because:

- oil inventories will need to be rebuilt,

- supply chains may remain disrupted,

- economies will continue to feel second-round effects of the supply shock.

- UBS maintains a defensive positioning in Europe, reducing exposure to cyclical sectors, including banks.

The military conflict in the Middle-East escalates

The military situation remains tense and escalatory: Iran launched overnight attacks on Israeli targets and US bases, Saudi Arabia intercepted drones, Kuwait reported damage to energy infrastructure, sirens were also triggered in Bahrain.

- QatarEnergy declared force majeure on LNG deliveries to Italy, Belgium, South Korea and China, adding to concerns over global energy supply.

- Energy infrastructure in Iran has also been hit, including facilities in Isfahan and a pipeline supplying the Khorramshahr power plant.

- Markets remain on “hyper alert”, with investors awaiting confirmation of formal US–Iran talks that could provide clearer direction.

Charts (xStation5)

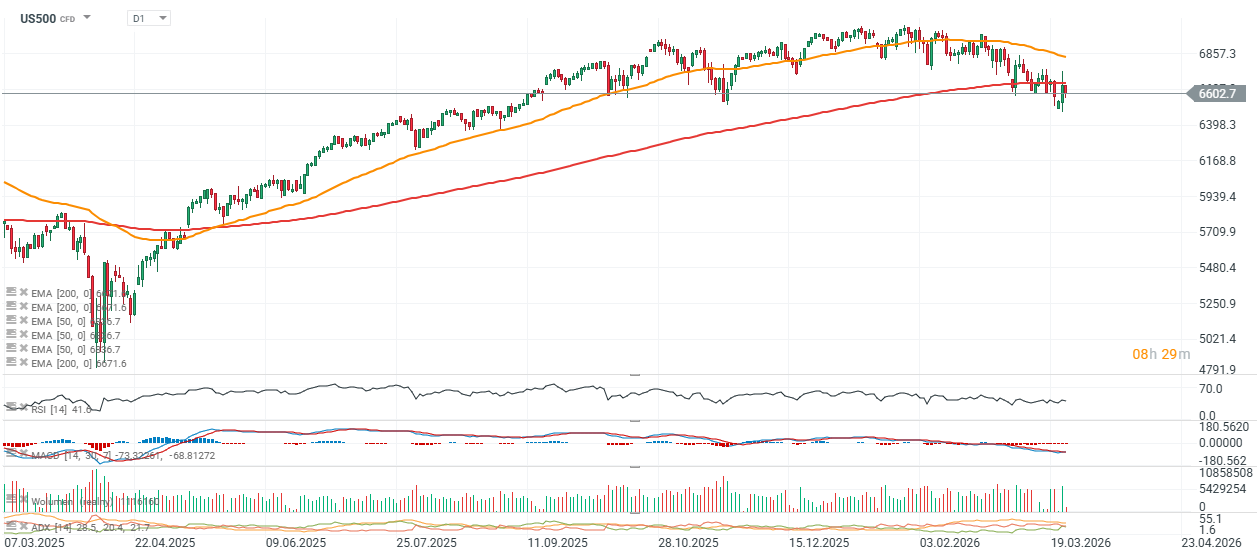

US500 (D1): elevated volatility with downside pressure dominating recent sessions.

Source: xStation5

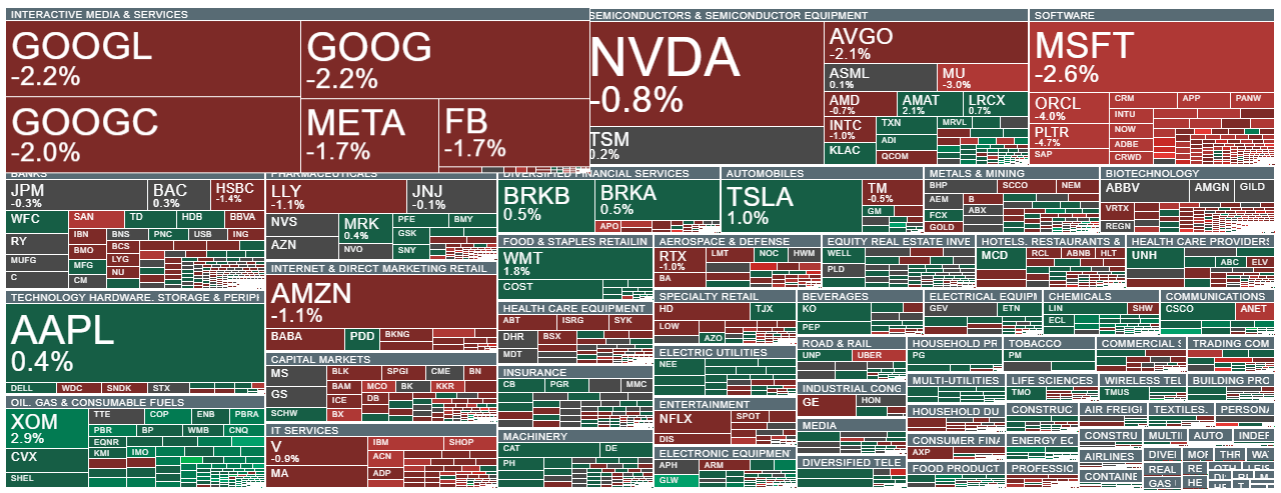

Sector view: oil continues its upward trend, while Microsoft and other IT names extend declines.

Source: xStation5

Corporate news

- US equity futures trimmed earlier losses after the cash open, though volatility remains elevated; S&P 500 contracts were broadly flat.

- Jefferies Financial Group (JEF) gained 9.5% in premarket trading, after the Financial Times reported that Sumitomo Mitsui Financial Group is considering a potential takeover, with investors pricing in a possible acquisition premium.

- JFrog (FROG) rose 2% before the open, following an upgrade from UBS (neutral → buy), with analysts highlighting resilient fundamentals despite recent share price weakness.

- Ralph Lauren (RL) added 1.7% in premarket trading, after Citi upgraded the stock to buy, citing successful brand elevation and improving operational performance.

- Trian Fund Management and General Catalyst Group amended the terms of their definitive agreement to acquire Janus Henderson.

- Ares Strategic Income Fund reported share repurchase requests totaling 11.6% of shares outstanding, significantly above its 5% framework limit.

- Apollo Global Management is limiting redemptions from one of its largest non-traded private credit funds for retail investors amid elevated withdrawal requests.

- Netgear (NTGR) surged 16% in premarket trading, after the FCC moved to ban imports of new foreign-made consumer routers, potentially improving the competitive landscape for domestic producers.

Source: xStation5

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

Mercedes earninigs: Is optimism justified?

The coffee market in the grip of weather and empty warehouses: The paradox of record Brazil harvests

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.