Wells Fargo started 2026 with a quarter that, at first glance, appears solid at the earnings level, but in reality presents a clearly negative picture in terms of earnings quality. Despite a marginal beat on earnings per share, the bank disappointed in two key areas, namely revenue and net interest income, which directly undermines the foundations of its business model.

The report highlights a clear weakness in core retail banking activity and continued pressure on net interest margins, which remain the most important source of the bank’s revenue. At the same time, positive elements such as growth in markets activity and corporate and investment banking are not sufficient to offset the deterioration in overall earnings quality.

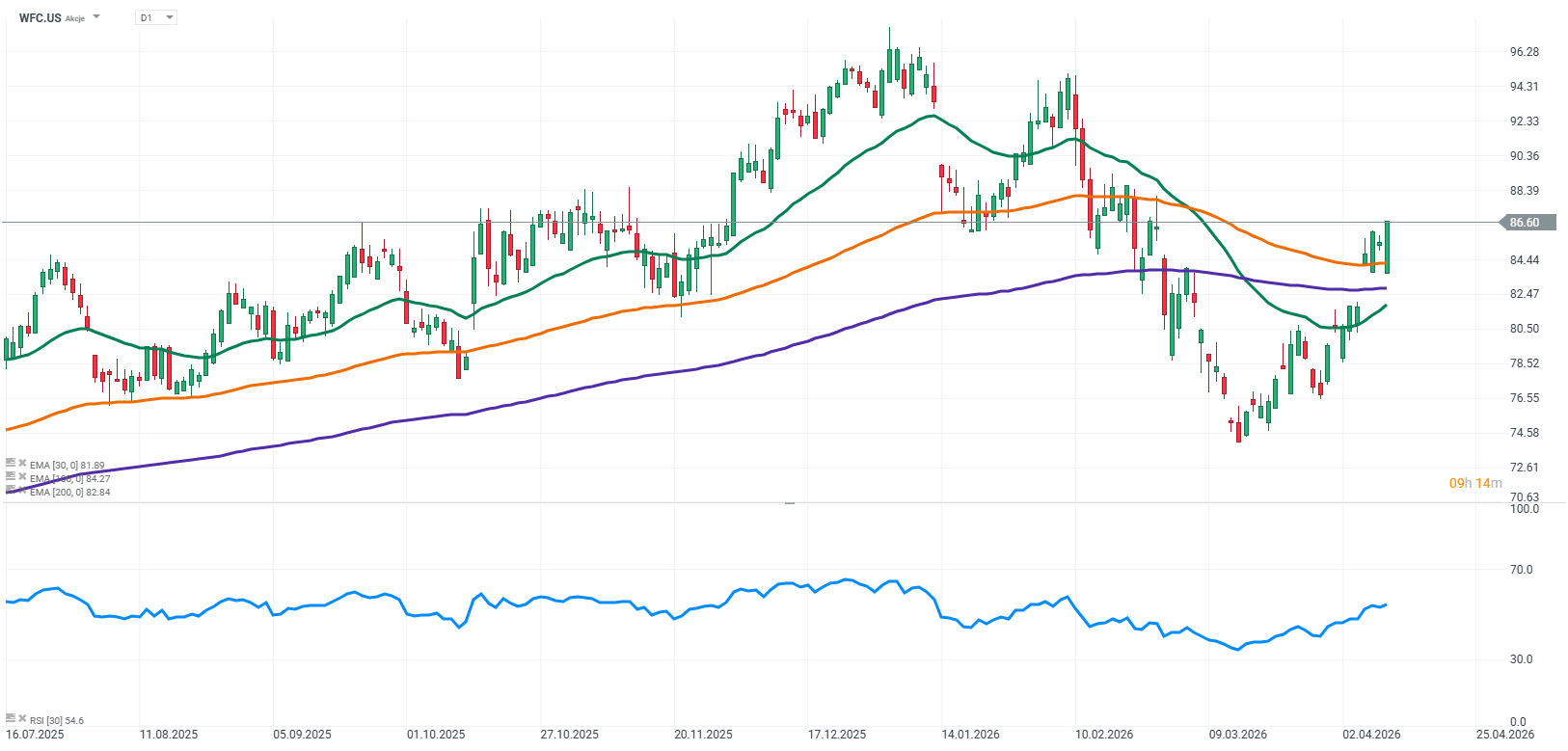

Despite year-over-year profit growth, the market reaction has been negative, confirming that investors are focusing on disappointments in key headline lines and the lack of convincing momentum in the core business.

Key financial results

-

Revenue: USD 21.45 billion, about USD 340 million below expectations

-

Net income: approximately USD 5.3 billion, year-over-year growth

-

Earnings per share (EPS): USD 1.60, beating forecasts by USD 0.02

-

Net interest income (NII): approximately USD 12.1 billion, below expectations

-

Credit loss provisions: approximately USD 1.1 billion, year-over-year increase

-

Corporate and investment banking: year-over-year growth

-

Private credit exposure: USD 36.2 billion

-

Return on equity (ROE): approximately 12.2%

Financial performance and profitability

At the earnings level, the report may appear stable, but its structure indicates a clear deterioration in earnings quality. EPS of USD 1.60 beat expectations only marginally, which is not sufficient to convince investors given the weakness in revenues.

Revenue of USD 21.45 billion disappointed the market and confirms that Wells Fargo is struggling to generate growth in its core business model. For a bank with strong retail banking exposure, this is a particularly negative signal.

A key issue remains the fact that earnings improvement is not driven by operating strength, but largely by cost control and more volatile income sources.

Net interest income (NII) as the key structural issue

Net interest income was the biggest disappointment in the report and remains a core issue in the bank’s investment narrative.

The result of approximately USD 12.1 billion fell short of expectations, highlighting increasing pressure on margins. The main drivers include rising deposit beta, a reduced ability to further reprice loans, and a changing interest rate environment.

For a bank like Wells Fargo, where net interest income accounts for more than half of total revenue, this is a clearly negative signal. In addition, the bank reaffirmed its full-year 2026 NII guidance of around USD 50 billion, but the weak first quarter undermines the credibility of this outlook.

Corporate and investment banking as insufficient support

The corporate and investment banking segment delivered solid double-digit year-over-year growth, benefiting from improved capital markets activity.

However, this does not change the overall picture of the report. The scale of this segment remains too small to offset the weakness in the core retail business. Compared to more diversified peers such as Goldman Sachs or JPMorgan Chase, Wells Fargo remains more dependent on net interest income.

Loans, balance sheet and exposure

The loan portfolio remains stable, and the bank continues moderate asset growth. However, this is not translating into proportional growth in net interest income, which further highlights margin pressure.

A notable element of the report is the USD 36.2 billion exposure to private credit. While not an immediate concern in the short term, it increases the bank’s sensitivity to a potential deterioration in the credit cycle.

Costs and risk

Credit loss provisions increased to approximately USD 1.1 billion, reflecting a more conservative approach to risk and potential deterioration in asset quality in upcoming quarters.

The combination of rising provisions and pressure on net interest income creates an unfavorable outlook for future profitability, particularly in the consumer lending segment.

Business structure and earnings quality

The most important conclusion from the report is the deterioration in earnings quality. The bank is generating higher profits, but not through stronger fundamentals, rather through short-term supportive factors.

The simultaneous disappointment in both revenue and net interest income, combined with their recurring weakness in recent quarters, points to structural issues in the core business. This is the factor driving the negative market reaction.

Key risks

The main risk remains continued pressure on net interest income in an environment of falling interest rates and increasing competition for deposits.

In addition, rising credit provisions, private credit exposure, and limited revenue diversification may increase the bank’s sensitivity to a downturn in the economic cycle.

Opportunities and positive factors

The positive element remains growth in corporate banking and capital markets activity, which could improve revenue diversification over the longer term.

There is also potential in private credit, although its contribution will take time to materialize and does not address the current issues in net interest income.

Outlook

In the near term, the outlook remains weak. A recovery in net interest income will be critical in upcoming quarters, as without it, the full-year guidance is increasingly at risk.

If margin pressure persists, achieving return on equity above 12 percent may prove challenging, and the bank is likely to continue losing ground to sector leaders.

Key takeaways

The first quarter of 2026 for Wells Fargo should be viewed negatively. Despite a marginal earnings per share beat, simultaneous disappointment in revenue and net interest income points to deteriorating earnings quality and pressure on the core business model.

Weakness in retail banking, rising sensitivity of deposit costs to interest rate changes, and insufficient revenue diversification all indicate that the bank is entering a more challenging phase of the cycle.

Without a clear improvement in net interest income in the coming quarters, it will be difficult to rebuild market confidence and maintain competitiveness against the largest players in the sector.

Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.