The cryptocurrency sector is seeing a gradual improvement in sentiment, with Bitcoin slowly overcoming significant resistance on its way to turning the main trend upward. Below we will look at important on-chain indicators that will shed more light on the strength of Bitcoin's current resurgence, which the entire cryptocurrency market is following. Historically, overcoming the 200-session average and the levels of the Realized Price below a year or so before halving proved to be a strong catalyst for increases. At the same time, macroeconomic conditions and a mixed earnings season on Wall Street can still hold back cryptocurrency bulls. What does the on-chain data show?

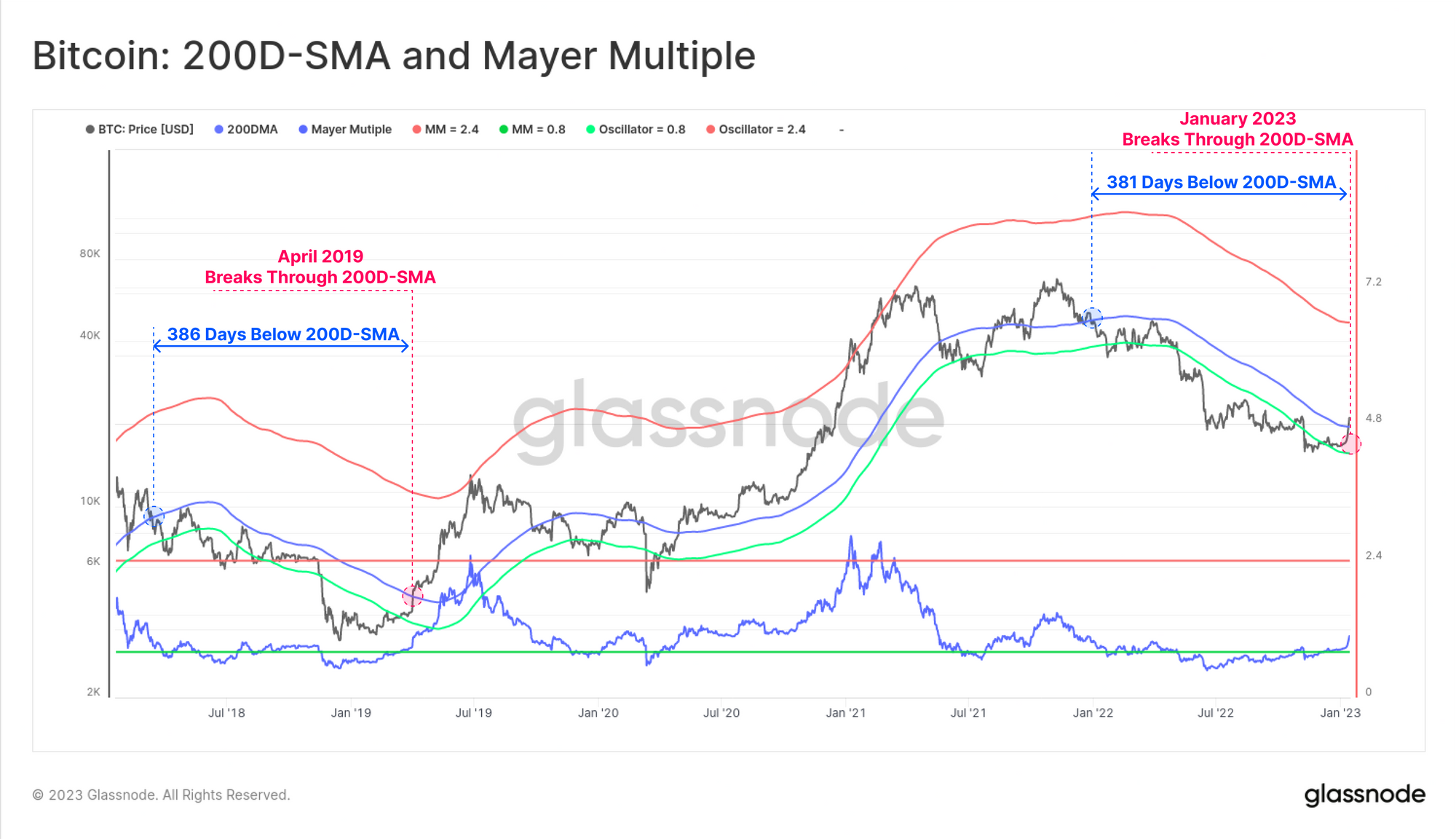

200 SMA on the D1 interval defeated

In the current bull market, the 'king of cryptocurrencies' has been below the 200-day moving average for 386 days. Previously in 2018-2019 it was 381 days. The Mayer Multiple indicator dividing Bitcoin's price by the 200-session average rose above levels near 1.0, suggesting a stronger improvement in sentiment and at least a short-term exit from the downtrend. Both of these have historically been indicators suggesting a longer-term rebound and have very rarely proved unreliable, which, however, absolutely does not prejudge their future effectiveness. The price managed to break through significant resistance as financial markets began a rally fueled by falling inflation, and the cryptocurrency industry heaved a sigh of relief as the FTX bankruptcy has so far failed to catalyze another avalanche of bankruptcies. Source: Glassnode

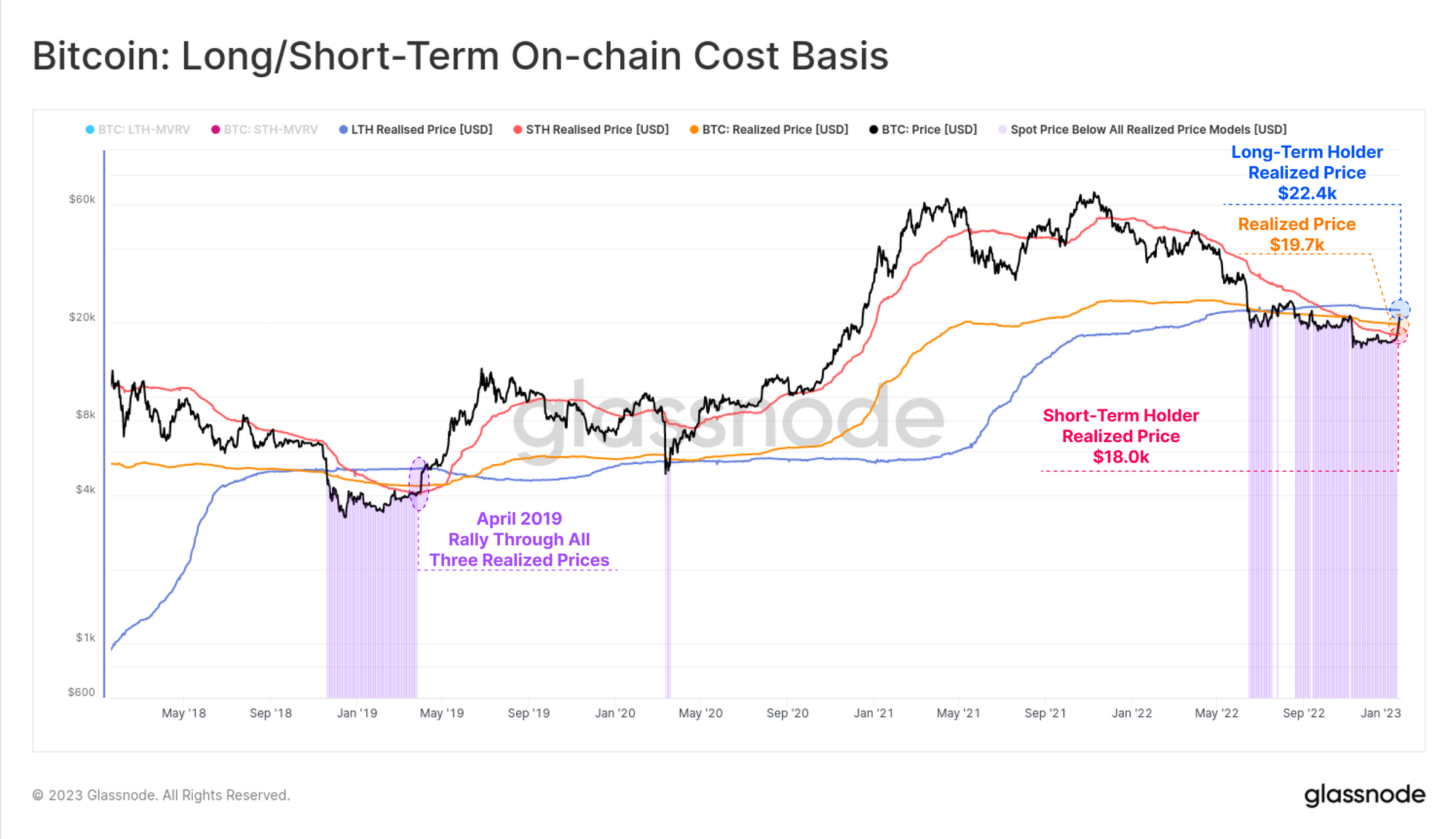

Price again above average 'Realize Price'

The chart shows average BTC purchase prices on the blockchain by address (Short Term Holders and Long Term Holders). We can see that for short-term investors, the price is more attractive, currently at around $18,000 against the average Realized Price (average historical BTC purchase price) at around $19,700. Long-term investors are still 'under the dash' with an average purchase price in the vicinity of $22,400, but in 2022 they were a loss-averse group so we can expect that they will not be willing to sell this time either, under 'impending halving' conditions. A potential sustained rise in price above $22,400 could herald a gradual improvement in conditions for further increases as the limited supply of particular investor groups along with new demand entering the market could help unleash the Bitcoin price. Source: Glassnode

The chart shows average BTC purchase prices on the blockchain by address (Short Term Holders and Long Term Holders). We can see that for short-term investors, the price is more attractive, currently at around $18,000 against the average Realized Price (average historical BTC purchase price) at around $19,700. Long-term investors are still 'under the dash' with an average purchase price in the vicinity of $22,400, but in 2022 they were a loss-averse group so we can expect that they will not be willing to sell this time either, under 'impending halving' conditions. A potential sustained rise in price above $22,400 could herald a gradual improvement in conditions for further increases as the limited supply of particular investor groups along with new demand entering the market could help unleash the Bitcoin price. Source: Glassnode

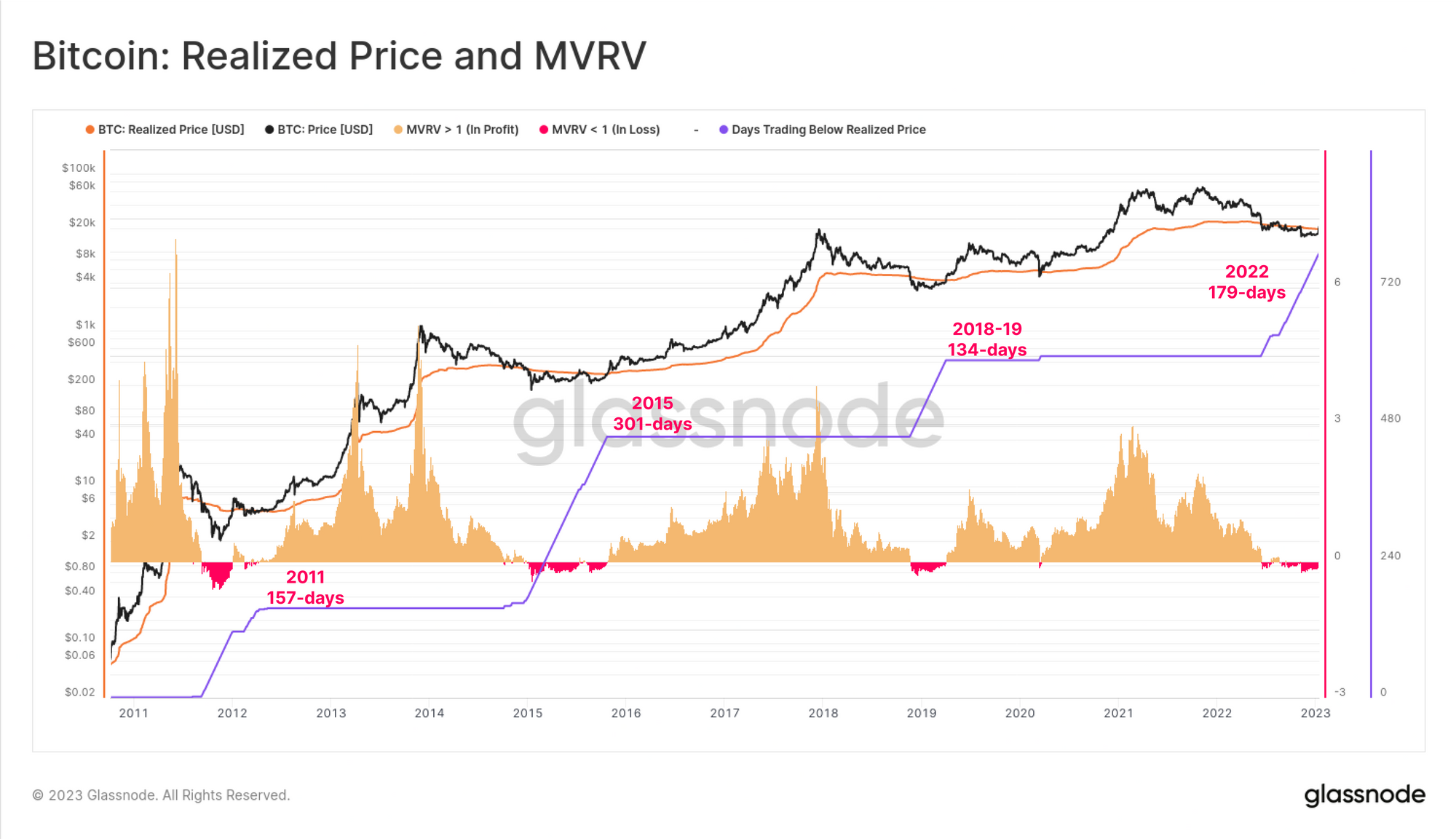

The price in the 2022 bull market was below the realized price for 179 days which is the second 'worst' result comparing it with previous bear markets. The previous time is 134 days. The record 301 days occurred during the 2014-2015 bear market. Source: Glassnode

The price in the 2022 bull market was below the realized price for 179 days which is the second 'worst' result comparing it with previous bear markets. The previous time is 134 days. The record 301 days occurred during the 2014-2015 bear market. Source: Glassnode

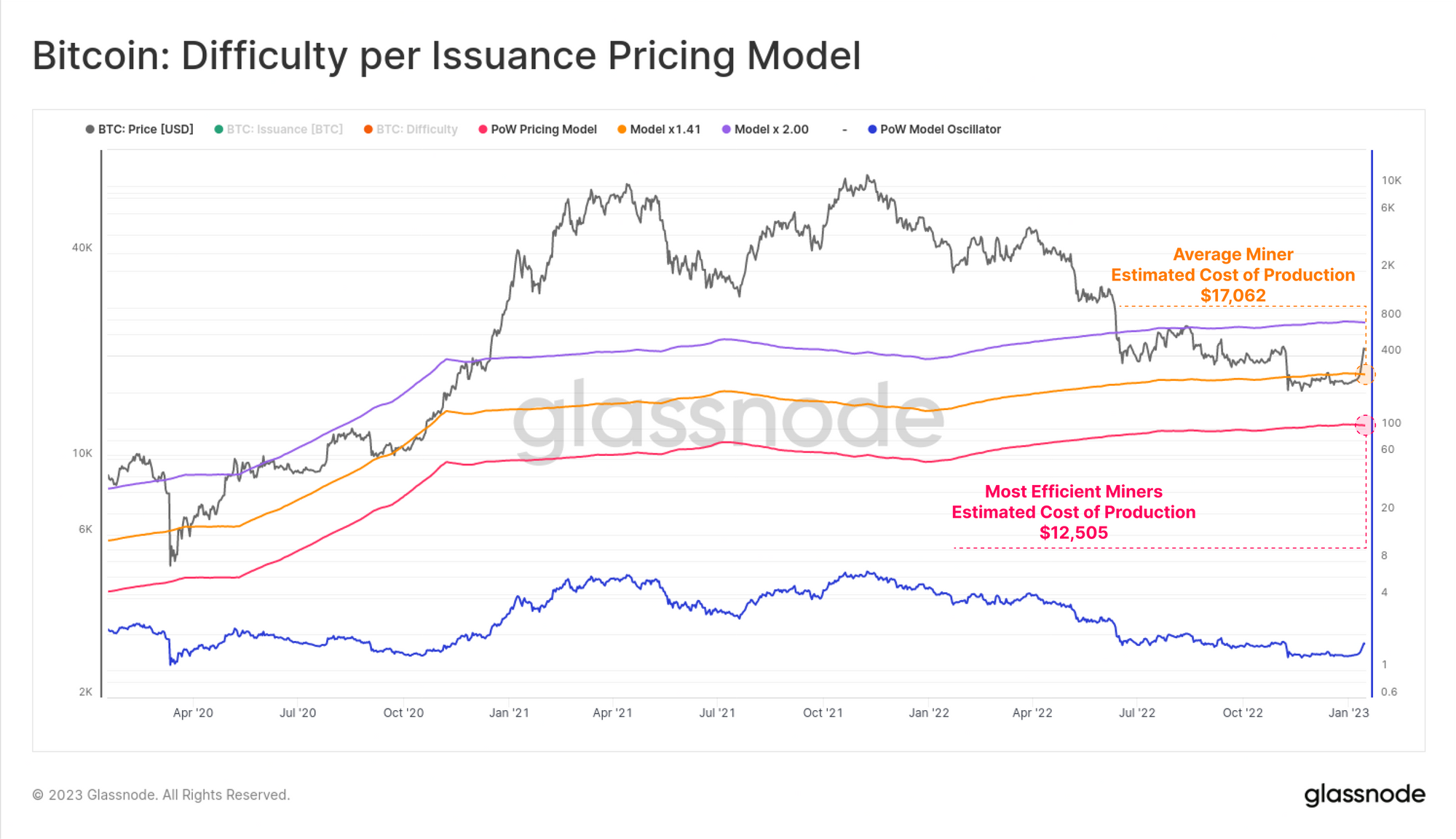

Lower stress on the BTC mining market

The price of BTC is well above the cost of mining, which could affect the limited supply from miners as global energy prices stabilize and players operating at break-even have suspended operations and dropped out of the market in 2022. The average price of mining BTC for the average miner is currently around $17,000 (although another Glassnode model indicates an average mining cost closer to $18,500) with the most efficient 'miners' able to 'mine' BTC at a much lower cost, hovering around $12,000. In the previous year, miners made up one of the largest 'dormant supply' groups. Source: Glassnode

Bitcoin chart, D1 interval. The RSI indicator signals an extreme overbought level near 88 points. The price of BTC has reached key short-term resistance near $21,200, these levels were lost in the face of the sudden bankruptcy of the FTX exchange. A breakout above them could open up gains to the summer 2022 maximums, while a drop back below $20,000 and a potential retest of support at the SMA 200 (red line) could be worrisome. Source: xStation5

Bitcoin chart, D1 interval. The RSI indicator signals an extreme overbought level near 88 points. The price of BTC has reached key short-term resistance near $21,200, these levels were lost in the face of the sudden bankruptcy of the FTX exchange. A breakout above them could open up gains to the summer 2022 maximums, while a drop back below $20,000 and a potential retest of support at the SMA 200 (red line) could be worrisome. Source: xStation5

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Bitcoin Climbs Above $66,000 as ETF Flows Recover but Glassnode Warns of Higher Volatility

Morning Wrap: Oil Climbs Back Above $90 as Chinese AI Weighs on Tech Stocks.

Morninga Wrap: Wall Street Under Pressure. AI Loses Momentum, Netflix Disappoints, and the Persian Gulf Erupts

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.