- Chicago wheat futures are trading near two-year highs

- Concerns over grain exports through the Black Sea and Sea of Azov are supporting prices

- Russian consultancy IKAR now estimates July wheat exports at 2 million tonnes, down from its previous 2.5 million-tonne forecast

- Shipping companies have been restricting vessel traffic through the Azov-Don Canal since July 10

- Adverse weather is weighing on European wheat crops, while Paris wheat futures have climbed to their highest level since March 2025

- Chicago wheat futures are trading near two-year highs

- Concerns over grain exports through the Black Sea and Sea of Azov are supporting prices

- Russian consultancy IKAR now estimates July wheat exports at 2 million tonnes, down from its previous 2.5 million-tonne forecast

- Shipping companies have been restricting vessel traffic through the Azov-Don Canal since July 10

- Adverse weather is weighing on European wheat crops, while Paris wheat futures have climbed to their highest level since March 2025

CBOT wheat futures (WHEAT) have surged above 680 cents per bushel after a sharp escalation in the conflict between Russia and Ukraine once again threatened grain exports from the Black Sea region. Chicago wheat futures climbed roughly 5% in a single session, reaching their highest levels in two years, and are now up around 7% since the start of the week. Investors are now trying to determine whether this rally marks the beginning of a sustained uptrend or simply a short-term reaction driven by geopolitical risks and aggressive short covering by speculative funds.

What is driving wheat prices higher? Key factors for investors

- Russia's wheat harvest is running 7-14 days behind last year. The delay is attributed to later planting and diesel fuel shortages, slowing the pace of grain reaching export markets.

- Analysts have cut Russia's July wheat export forecasts by 13-20%. IKAR now expects exports below 2 million tonnes, down from its previous 2.5 million-tonne estimate, while SovEcon reduced its forecast to 2 million tonnes, representing a 4.8% year-over-year decline.

- Disruptions in the Sea of Azov are increasing concerns over global wheat supplies. Since July 10, shipping companies have been restricting vessel traffic through the Azov-Don Canal due to the growing risk of attacks, despite the absence of a formal shipping ban.

- Around 25% of Russia's grain and sunflower oil exports move through the shallow ports of the Sea of Azov. During the August-October export peak, deep-water Black Sea ports may not fully compensate for lost capacity, increasing the risk of shipment delays.

- Russia's Transport Ministry says it is taking measures to maintain export logistics, but market participants warn that some farmers may be forced to store harvested grain if transportation capacity proves insufficient.

- Weather has become another bullish catalyst. France's agriculture ministry expects the country's soft wheat harvest to decline 4% this year to around 32 million tonnes after repeated heatwaves reduced yields.

- Average wheat yields in France are projected at 6.93 tonnes per hectare, roughly 7% below last year, while extreme temperatures may also have damaged up to one-third of the country's corn crop.

- Paris wheat futures have climbed to their highest level since March 2025, trading above €225 per tonne, highlighting growing concerns about European grain supplies.

- Potential export disruptions in Russia could redirect import demand toward the European Union and other exporting regions. The current rally is primarily supported by geopolitical risks in the Black Sea, lower Russian export forecasts, deteriorating crop prospects in France, and large speculative short positions that increase the potential for further sharp price gains.

The Black Sea has once again become the key driver of the wheat market

Following Ukrainian drone attacks, Russia restricted shipping through the Sea of Azov, a route handling roughly 25% of Russian grain exports. At the same time, Russia launched additional strikes against port infrastructure in Odesa, while U.S. strikes on Iran reportedly damaged a wheat storage facility. Commodity markets quickly price in logistical risks because Russia remains the world's largest wheat exporter, while together with Ukraine the two countries account for a significant share of global grain trade.

The Black Sea serves as a strategic export corridor linking Eastern European producers with buyers across Africa, Asia, and the Middle East. Even partial shipping disruptions can increase freight costs, delay deliveries, and push global food prices higher. Analysts also warn that disruptions could eventually extend to fertilizer shipments and other agricultural commodities, potentially increasing inflationary pressures well beyond the wheat market.

Speculative funds amplified the rally

Geopolitical developments tell only part of the story. Before the rally began, managed money funds held one of their largest net short positions in CBOT wheat futures in many months, reflecting widespread expectations of further price declines.

The sudden deterioration in the geopolitical outlook forced many investors to buy back previously sold contracts in order to limit losses. This short covering often produces much larger price moves than supply-and-demand fundamentals alone would justify. The combination of escalating Black Sea tensions and heavily bearish positioning allowed wheat futures to reach their highest levels in two years.

Fundamentals remain stable, but geopolitics is driving the market

Despite the sharp rally, U.S. supply fundamentals remain relatively healthy. According to the latest USDA Crop Progress report, 67% of the U.S. winter wheat crop has already been harvested, ahead of the historical average, 72% of the spring wheat crop has headed, and 58% of the crop is rated good to excellent. This suggests the current rally is being driven primarily by geopolitical risks and investor positioning rather than a deterioration in global production.

Export demand also remains supportive. Taiwan recently purchased approximately 98,000 tonnes of U.S. wheat, confirming continued international demand, although European Union wheat exports during the first half of July were slightly below last year's pace. For investors, this means that in the near term, price direction is likely to depend far more on developments in the Black Sea region than on harvest data or the broader global supply balance.

The coming days will determine whether export disruptions in the Black Sea prove temporary or evolve into more prolonged supply constraints. If Russia maintains shipping restrictions or military activity expands to additional ports and export terminals, wheat prices could remain elevated. On the other hand, a rapid easing of geopolitical tensions could quickly shift market attention back toward favorable harvest prospects and comfortable global grain inventories.

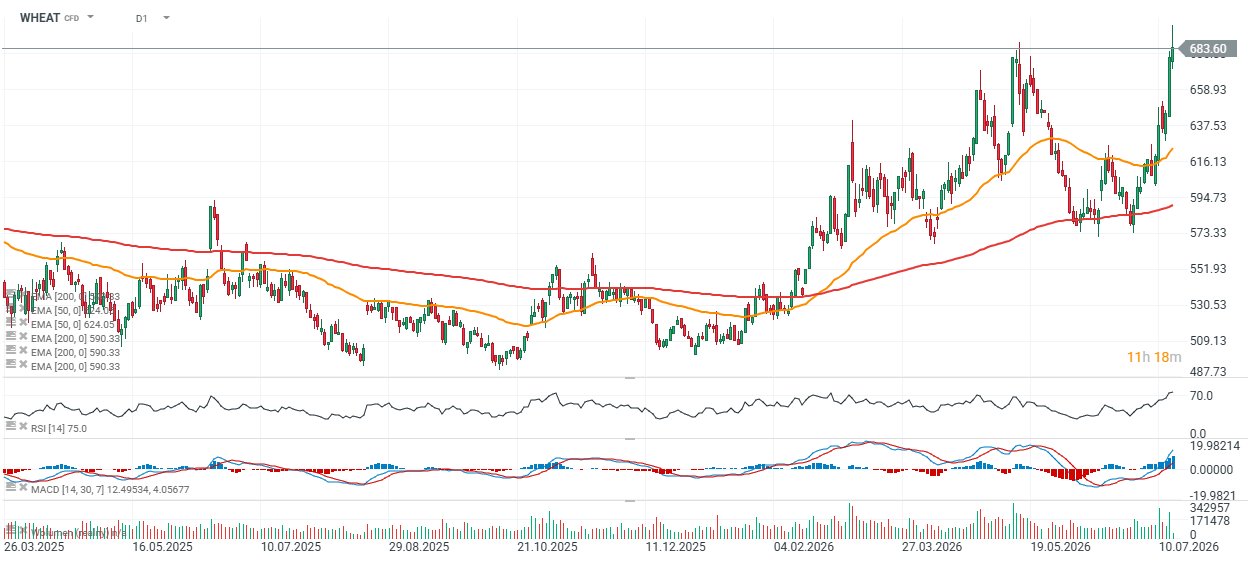

WHEAT chart (D1 timeframe)

The CBOT wheat contract has now advanced for a third consecutive session, with the three-day rally comparable in magnitude to the upward impulse seen between May 8 and May 14. Prices have reached a key resistance zone. A sustained move above 700 cents per bushel could potentially open the door to another leg higher, although at this stage a corrective pullback toward the 640-650 cent area appears equally plausible.

Source: xStation5

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.