Market expectations for today's FOMC meeting are clear - US central bank will deliver a 75 basis point rate hike. Moreover, market prices in another such big move in July! It is a result of inflation still exceeding expectations and failing to drop even after tightening that was already delivered. Nevertheless, there were not too many comments from Fed members pointing to a possibility of a hike bigger than 50 basis points. It does not mean that Fed rules out the biggest rate hike since 1994 as the Reserve said numerous times that it will act if needed. One thing that Fed certainly wants to avoid is the wage-price spiral that was persistent throughout the 70s. Where is US500 and EURUSD now? How can those markets react to today's decision?

What to expect from today's Fed meeting? What we need to know before the decision?

-

Fed should deliver a 75 basis point rate hike even in spite of an increased risk of recession

-

Bigger rate hike is possible due to higher inflation forecasts. Possibility of a similarly big hike at next meeting should be well communicated

-

Major banks like Nomura or Goldman Sachs expect the Fed to deliver a 75 rate hike. Median estimate among economists remains at 50 bp

-

Fed may signal increased reduction in QE programme, what would magnift pressure on equities. It is not the base case scenario however

-

Dot-plot will likely continue to underestimate the final rate. It pointed to an end-cycle rate of 2.8% and now it is expected closer to 3.5%. However, markets sees possibility of Fed funds rate jumping to as high as 4% in this cycle

-

Fed wants to avoid 70s scenario when inflation expectations de-anchored due to slow process of rate hikes

-

The faster Fed gets inflation under control, the better for markets, even if it leads to a slowdown or short-term recession

-

Correction on Wall Street during the 70s resulted in a 40% drop during the first phase of monetary policy tightening. A quick rate cuts that followed triggered a 20-year period of gains that exceeded 20%

What conclusions should we draw? A 50 basis point rate hike may lead to a brief improvement in moods but will not improve the fundamental outlook. Bigger and faster rates hikes may lead to a recession but will also allow the Fed to provide support quicker. Higher taxes will cool the economy what should lower oil prices - a key driver of inflation.

Inflation still remain far off the levels seen in the 70s but if current interest rates do not rise quickly, we may once again experience de-anchoring of inflation expectations. The sooner Fed decides to match market expectations, the quicker markets will be ready to rebound. Source: Bloomberg

Inflation still remain far off the levels seen in the 70s but if current interest rates do not rise quickly, we may once again experience de-anchoring of inflation expectations. The sooner Fed decides to match market expectations, the quicker markets will be ready to rebound. Source: Bloomberg

Currently, Fed sees end-of-cycle rate at 2.8% but dot-plot release today will likely show median more closely to 3.5%. Bloomberg consensus and interest rate markets see end-of-cycle rate as high as 4% next year. If Fed accelerates tightening, it will be able to more quickly resume support for the economy. Source: xStation5

Currently, Fed sees end-of-cycle rate at 2.8% but dot-plot release today will likely show median more closely to 3.5%. Bloomberg consensus and interest rate markets see end-of-cycle rate as high as 4% next year. If Fed accelerates tightening, it will be able to more quickly resume support for the economy. Source: xStation5

A look at the markets

EURUSD

US dollar is strong and will likely continue to remain in the near future, unless the Fed shows that it has managed to tame inflation expectations. EURUSD has always recovered following a break of 25 area at RSI indicator and further rebound from 17 area. The pair usually gained 100-300 pips in such situations. The lower-end of the range was already reached and the higher would point to a potential move to as high as 1.07. US dollar index remained relatively stable during the first phase of tightening in the 70s suggesting the USD may remain stable now as well. Source: xStation5

US dollar is strong and will likely continue to remain in the near future, unless the Fed shows that it has managed to tame inflation expectations. EURUSD has always recovered following a break of 25 area at RSI indicator and further rebound from 17 area. The pair usually gained 100-300 pips in such situations. The lower-end of the range was already reached and the higher would point to a potential move to as high as 1.07. US dollar index remained relatively stable during the first phase of tightening in the 70s suggesting the USD may remain stable now as well. Source: xStation5

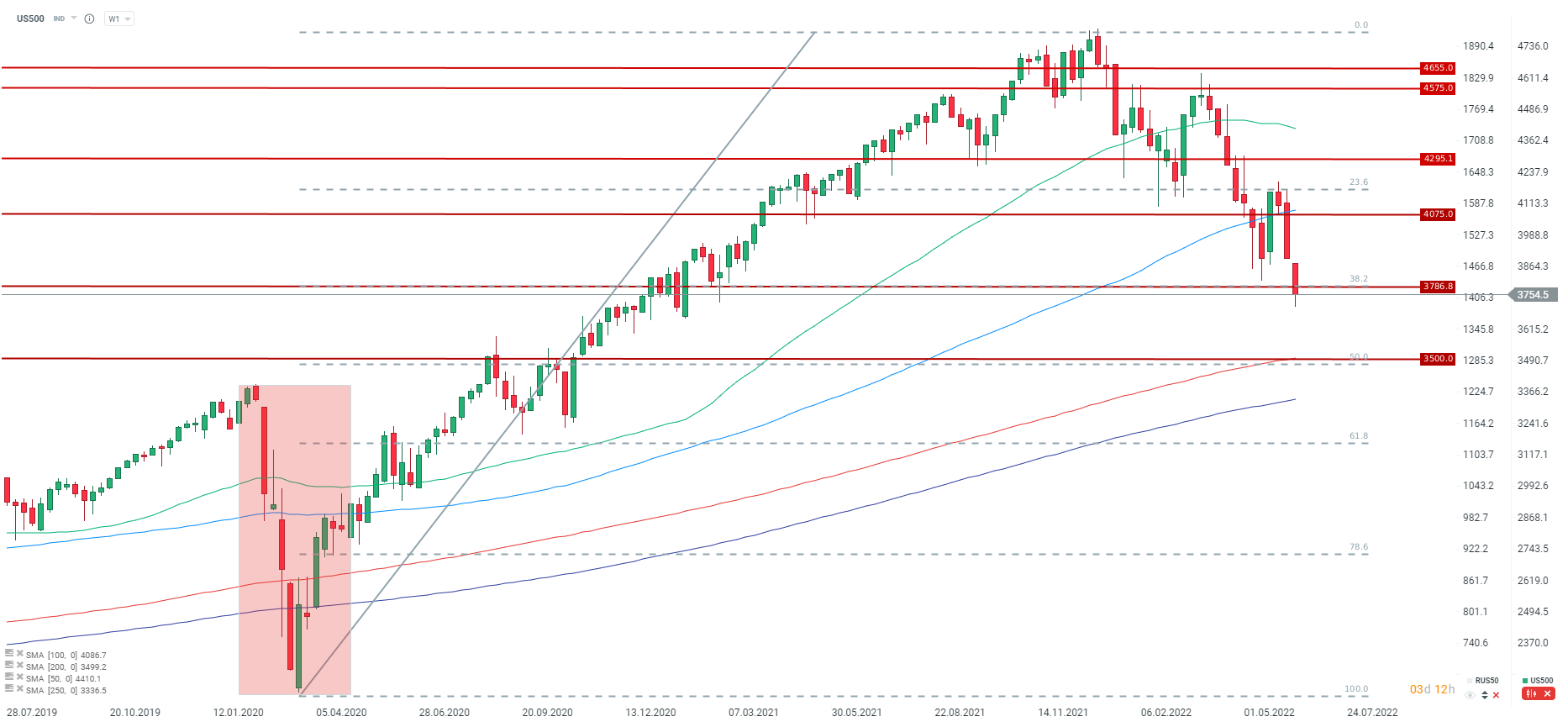

US500

US500 reacted negatively to 38.2% retracement and remains in technical bear market territory. Key resistance for the index can be found in the 3,900 pts area, where a bearish price gap can be found. A key support for the index can be found in the 3,500 pts area, where the 200-week moving average as well as 50% retracement of the whole post-pandemic recovery move can be found. If Fed fails to deliver a 75 basis point rate hike, a jump in equities may be expected. However, it should be rather a temporary jump. Source: xStation5

US500 reacted negatively to 38.2% retracement and remains in technical bear market territory. Key resistance for the index can be found in the 3,900 pts area, where a bearish price gap can be found. A key support for the index can be found in the 3,500 pts area, where the 200-week moving average as well as 50% retracement of the whole post-pandemic recovery move can be found. If Fed fails to deliver a 75 basis point rate hike, a jump in equities may be expected. However, it should be rather a temporary jump. Source: xStation5

US500 reaction to previous rate hikes

At the end of 6-hour period after rate hike decisions during the current and previous cycle, US500 traded either flat or slightly lower. However, it should be noted that neither of those rate hikes was a surprise for markets. Source: Bloomberg

At the end of 6-hour period after rate hike decisions during the current and previous cycle, US500 traded either flat or slightly lower. However, it should be noted that neither of those rate hikes was a surprise for markets. Source: Bloomberg

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Economic Calendar: Markets Awaken After a Weekend of Geopolitical Deadlock🚢

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.